California Transfer On Death Deed Stepped Up Basis

California Tod Deed Form Get A Transfer On Death Deed Online

Https Saclaw Org Wp Content Uploads Sbs Tod Deed Pdf

Https Saclaw Org Wp Content Uploads Sbs Tod Deed Pdf

Https Saclaw Org Wp Content Uploads Sbs Tod Deed Pdf

Transfer On Death Deeds In California Across The Bar

California Transfer On Death Affidavit Forms Deeds Com

Get Results from 6 Engines at Once.

California transfer on death deed stepped up basis. What happens is that the owner of the real property creates a deed that adds the name of at least one additional person as a beneficiary of the property should the owner die. There are 3 effective ways to revoke this deed. Transfer on death deed The simplest and easiest way to make real estate into non probate property is with a transfer on death deed.

8242016 When the transfer occurs after the donors death the recipient of the property receives a step-up in basis to propertys date-of-death value. Now California allows for the transfer of real property upon a persons death thereby avoiding probate. Probate is an expensive lengthy and tedious legal process that occurs when a proper Estate Plan is not in place.

8122017 With a transfer on death account your beneficiary receives stock valued at 75 a share. 7132020 When someone dies and leaves an asset to an heir the tax basis resets to the value on the day of death. That could be bad if the asset has fallen in value between the date it was purchased and the date of death because a taxable loss was not booked but generally it is a good thing reducing capital gains taxes for the heirs.

This effectively makes title uninsurable for 120 days after date of death. Get Results from 6 Engines at Once. This can result in significant tax savings when the recipient sells the property.

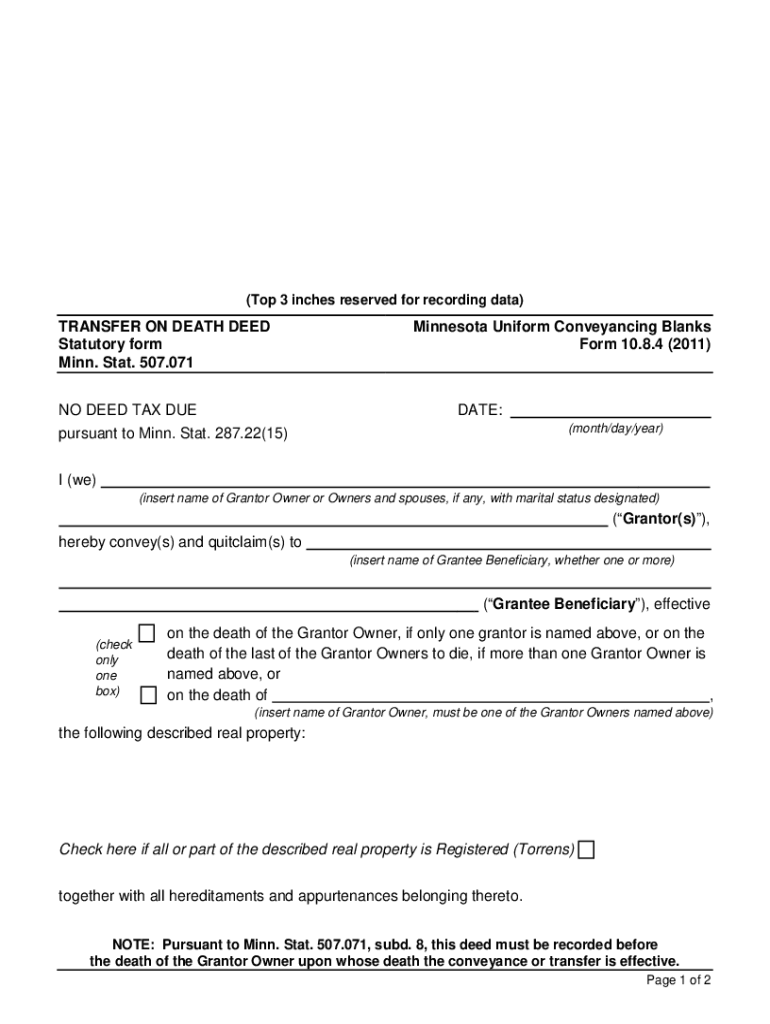

See IRC 6754. 7252016 Effective January 1 2016 California now provides for a revocable transfer on death deed TOD which if properly recorded serves as inexpensive alternative to avoid probate. It can be revoked cancelled or replaced anytime and has no effect until the death of the owner.

5122020 Using a transfer on death deed allows the owner to keep complete ownership of the property and control all financial decisions related to it. How Californias Transfer on Death Deed Works. A step-up in basis of a partnership or LLC interest upon the death of a partnerLLC member will only apply to the outside basis ie the tax basis of the interest in the hands of the successor owners.

Colorado Transfer On Death Beneficiary Deed Online Legal Form Nolo

Free Transfer On Death Deed Free To Print Save Download

Understanding The Transfer On Death Deed Legalzoom Com

Mn Transfer On Death Deed Form Fill Online Printable Fillable Blank Pdffiller

New California Law Transfer On Death Deeds Expire After Jan 1 2021 Askamity Episode 53 Youtube

Quitclaim Deed Information Guide Examples And Forms Deeds Com

Seven Reasons A Transfer On Death Deed To Avoid Probate Might Be A Bad Idea

Problems With Deeds On Death Transfer On Death Deeds Or Beneficiary Deeds Grant Morris Dodds Probate Estate Planning Attorneys

Real Estate Transfer Taxes Deeds Com

Free Hawaii Last Will And Testament Template Pdf Word Eforms Free Fillable Forms Will And Testament Last Will And Testament Obituaries Template

How To Add A Beneficiary To A Mortgage Deed Legalzoom Com

60 Important Papers And Documents For A Home Filing System Checklist Home Filing System Estate Planning Checklist Organizing Paperwork