Nj Controlling Interest Transfer Tax Exemptions

Https Www Alston Com Media Files Insights Publications 2017 01 Controlling Interest Transfer Taxes A Mostly Criti Files Controlling Interest Transfer Taxes Jmt Jan 2017 Fileattachment Controlling Interest Transfer Taxes Jmt Jan 2017 Pdf

Https Www Alston Com Media Controlling Interest Transfer Taxes Part Two Jmt N Pdf

Form Citt 1 Fillable Controlling Interest Transfer Tax

Controlling Interest Transfer Tax Buyer Beware New Jersey Law Firm New Jersey Attorneys Lawyers

Https Www Bracheichler Com Wp Content Uploads 2019 12 Gladstone Ecepc Presentation Pdf

Form Citt 1 Fillable Controlling Interest Transfer Tax

452011 Essentially the new law imposes a tax on the purchaser in a non-deed transfer of a controlling interest in an entity that owns classified real property if the total consideration for the transfer is in excess of 1million.

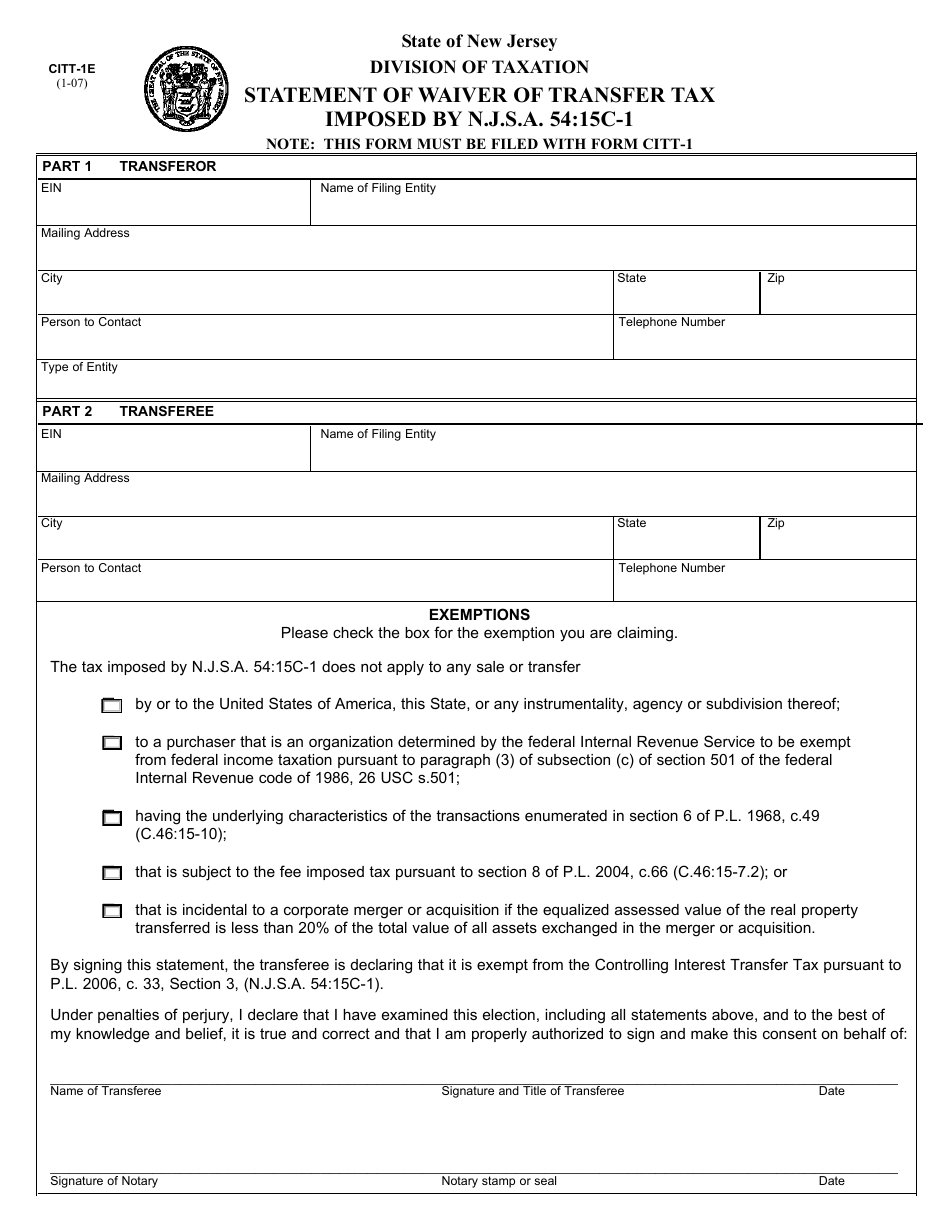

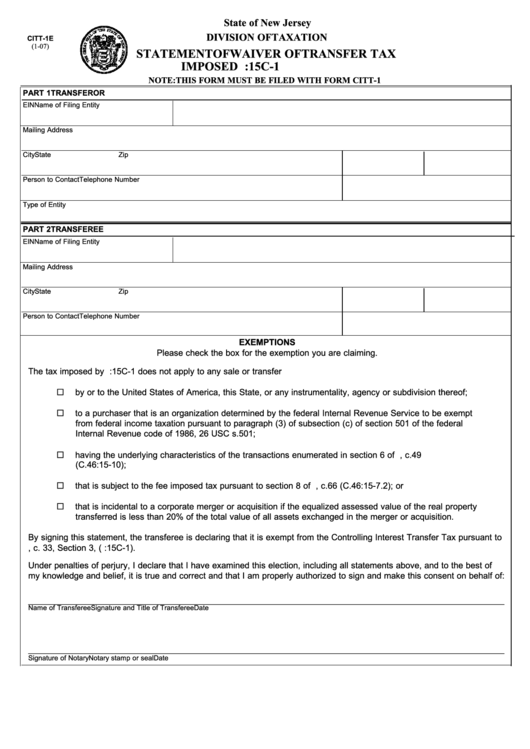

Nj controlling interest transfer tax exemptions. Tax does not apply to transfers of publicly traded stock. By including that direct or indirect. A separate statement of waiver Form CITT-1E must be filed if an exemption is claimed.

The Controlling Interest Transfer Tax is due on or before the last day of the month following the month in which the sale or transfer of the controlling interest is completed. This fee is separate from a Controlling Interest Transfer Tax CITT which applies only to certain transfers of controlling interest in entities possessing commercial properties. Recordation and transfer tax rates vary from 116 to 3.

2162021 Even if a merger qualifies as a tax-deferred reorganization under the federal tax code a controlling interest transfer tax may be imposed if the transfer represents ownership change in an entity holding real estate and there is no applicable exemption. Controlling Interest Transfer Tax The Controlling Interest Transfer Tax CITT applies in situations where there is a transfer in the controlling interest of an entity which owns 4A property with a value of over 1 million dollars. 5415C-1 imposes the controlling interest transfer tax CITT on the buyer.

The CIT is only imposed if the real property is classified as 4A Commercial and if the consideration or other valuation of the real property is greater than 1 million. If the property is the only asset of the acquired entity the purchase price is used to determine the tax amount. Shall be attached as an exhibit to the sellertransferors business tax return for the entity filed with New Jersey.

If the entity owns. Exemptions include the following sales or transfers. 1 A controlling interest transfer that is accomplished by a transferring document other than a deed or trust document does not qualify for any of the exemptions under 35 ILCS 20031 -45.

The 1 percent is applied to. The Controlling Interest Transfer CIT tax is imposed by the state when Connecticut real estate interests are transferred through the sale or trade of controlling interests of a corporation partnership or similar type entity. Furthermore the New Jersey law is clear about the computation of the tax base.

Form Citt 1 Fillable Controlling Interest Transfer Tax

Form Citt 1e Download Fillable Pdf Or Fill Online Statement Of Waiver Of Transfer Tax New Jersey Templateroller

State Local Tax Controlling Interest Transfer Tax Freeman Law Jdsupra

Http Rc Com Documents Transfertaxconsiderationsinchangeinentity 20 Appendixa Pdf

Tp 584 Combined Real Estate Transfer Tax Return Credit Line Mortgage And Exemption Certificate Free Download

Https Www Greenbaumlaw Com Media Publication 483 Practical 20law 20ownership 20 20jan 20 20tjd 20ktb 20msk Pdf

Https Www Jstor Org Stable 20781726

Combined Real Estate Transfer Tax Return Form Free Download

Tp 584 Combined Real Estate Transfer Tax Return Credit Line Mortgage And Exemption Certificate Free Download

Http Full Coleschotz Com 2b7963 Assets Files News 251 Pdf

Combined Real Estate Transfer Tax Return Form Free Download

Http Www Millvillenj Gov Agendacenter Viewfile Item 6794 Fileid 11822

Fillable Form Citt 1e Statement Of Waiver Of Transfer Tax Imposed By N J S A 54 15c 1 Printable Pdf Download