Nyc Real Property Transfer Tax Law

Nyc Nys Transfer Tax Calculator For Sellers Hauseit

Nyc Nys Transfer Tax Calculator For Sellers Hauseit

Nyc Nys Transfer Tax Calculator For Sellers Hauseit

Https Www Friedfrank Com Sitefiles Publications 070061927 20fried Pdf

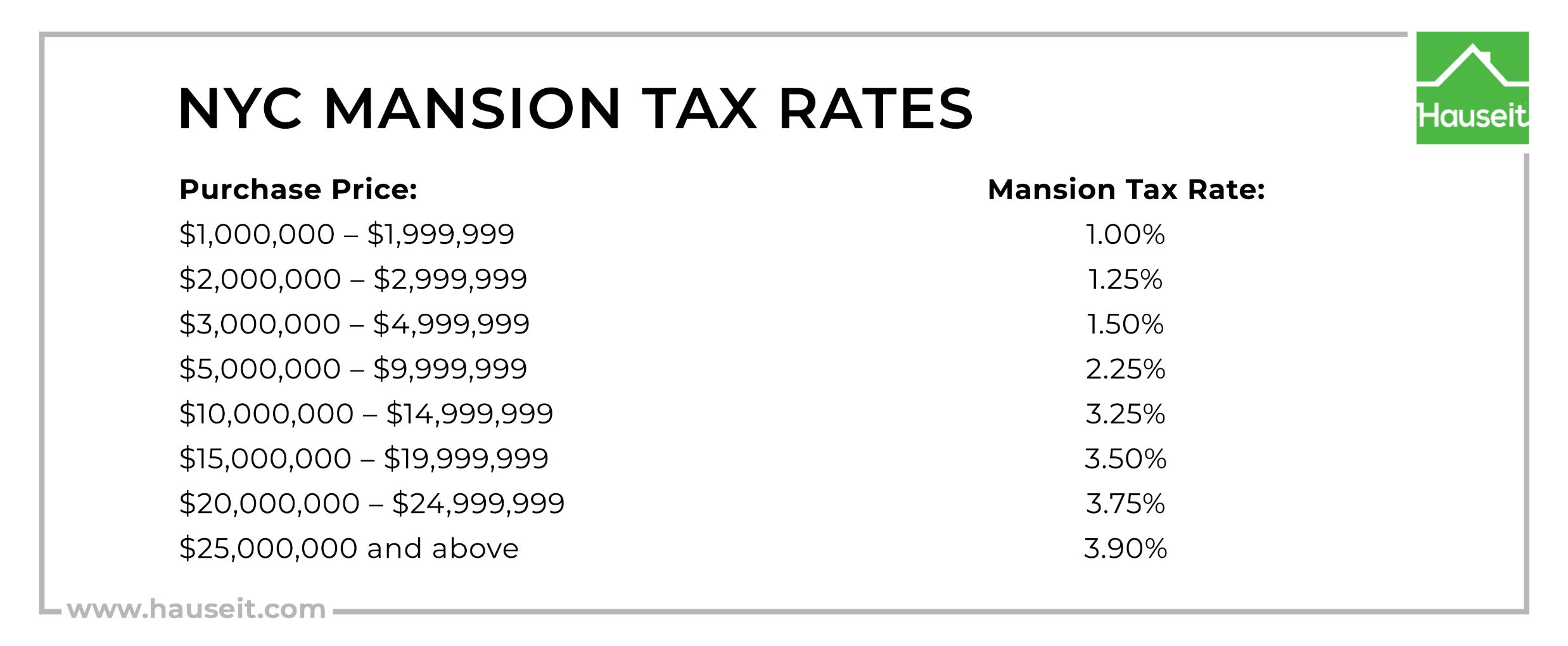

Nyc Mansion Tax Of 1 To 3 9 2021 Overview And Faq Hauseit

Nyc Nys Transfer Tax Calculator For Sellers Hauseit

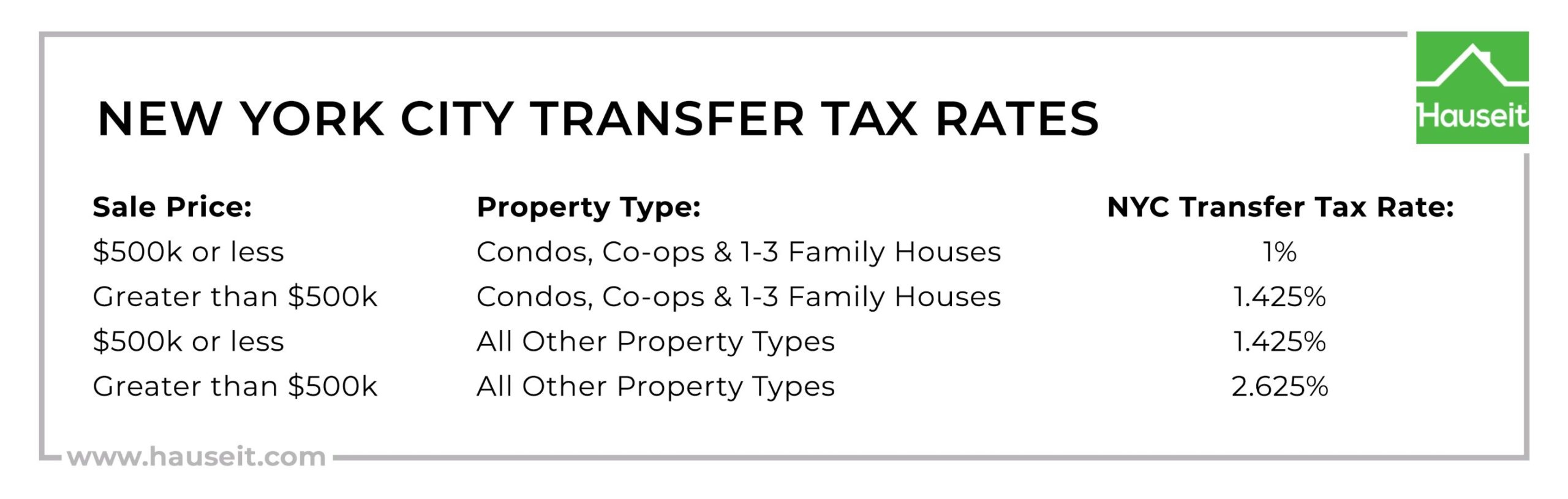

The tax is assessed at a graduated rate ranging from 1 to 2625 depending on the classification of the property conveyed and the total consideration paid.

Nyc real property transfer tax law. The tax is 2 for each 500. 1404 - Liability for tax. 1401f provides in part that an interest in real property includes a contract to purchase real property a beneficial interest and the right to receive rents profits or other income.

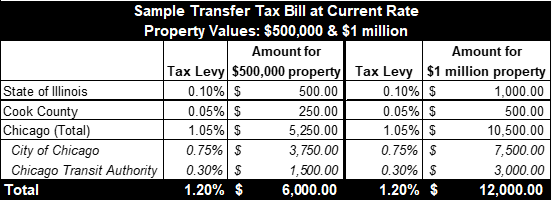

9122017 Two main statutes provide the foundation for the real property transfer sales. 6292017 NYCs RPTT Real Property Transfer Tax is authorized by the New York Tax Law Section 1201 b and enacted by Title 11 Chapter 21 of the New York City Administrative Code. 2132021 The following shall be exempt from the payment of the real estate transfer tax.

Section 663 Estimated Tax on Sale or Transfer of Real Property by Nonresident. 1272016 Tax Law. Real Property Transfer Tax FLR-994750-021 Dear.

1 Anything to the contrary notwithstanding in the case of any conveyance or transfer of real property or any economic interest therein in complete or partial liquidation of a corporation partnership association trust or other entity the taxes imposed by this section shall be measured by i the consideration for such conveyance or transfer or ii the value of the real property or. Xvi This includes any document whereby any real property or. It applies to all residential properties in NYC including townhouses condos and co-ops.

As the transfer or transfers of any interest in real property by any method. Both the NYS real estate transfer tax return TP-584 and the NYC RPT real property tax return NYC-RPT list no consideration transfers among the types of conveyances that are exempt from transfer tax. Real Property Law.

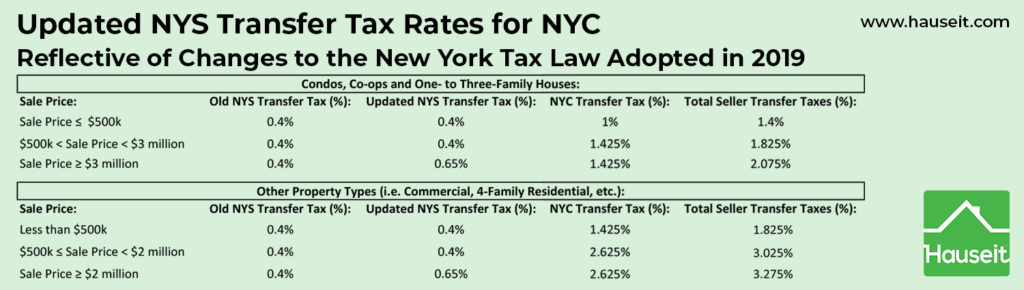

1402-A - Additional tax. 333 establishes the requirement for providing information to ORPTS for every deeded transfer of property in New York State. The New York City transfer tax goes from 1 to 1425 when over 500000.

Https Www Huntonak Com En Insights New York And Dc Changes To Real Estate Transfer Tax Rett Html

Nys And Nyc Real Estate Transfer Tax Overview For Nyc Nyc Real Estate Real Estate Infographic Nyc Infographic

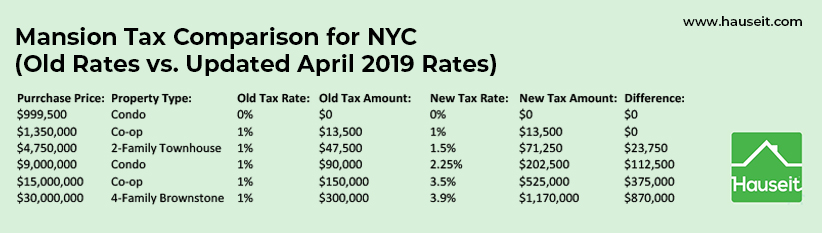

Changes To Nyc Mansion Tax And Nys Transfer Taxes For 2019 Hauseit

Nyc Nys Transfer Tax Calculator For Sellers Hauseit

Nyc Nys Transfer Tax Calculator For Sellers Hauseit

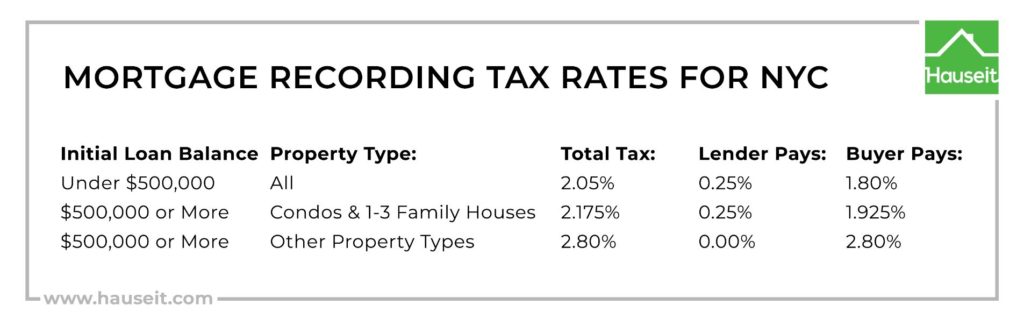

Nyc Mortgage Recording Tax Of 1 8 To 1 925 2021 Hauseit

Changes To Nyc Mansion Tax And Nys Transfer Taxes For 2019 Hauseit

Nyc Nys Transfer Tax Calculator For Sellers Hauseit

What Is The Average Co Op Flip Tax In Nyc And Who Pays It By Hauseit Medium

Real Estate Transfer Taxes Deeds Com

New York State Requirements For A Quitclaim Deed Legalzoom Com

Https Www Mosessinger Com Site Files Ljn Nlmat 2016 11 01 Pdf

Transferring To A Real Estate Transfer Tax City State Ny