Nyc Transfer Tax Assignment Of Contract

Assignment Contract Real Estate Contract Contract Template Signs Youre In Love

General Assignment Agreement Free Fillable Pdf Forms Business Analysis Assignments Agreement

Assignment Of Option To Purchase Real Estate Assignment Contract Basics For The Real Estate Investor

Assignment Of Option To Purchase Real Estate Assignment Contract Basics For The Real Estate Investor

Llc Transfer Of Ownership Agreement Sample Intellectual Inside Intellectual Property Assignment A Rental Agreement Templates Contract Agreement Lease Agreement

Transfer Of Ownership Contract Template Beautiful Intellectual Property Assignment Agreement Template Contract Template Wedding Place Card Templates Contract

You should however read the contract carefully because the contract may say it cannot be assigned and it may also impose a fee due to one of the parties if it is assigned.

Nyc transfer tax assignment of contract. Calculate Seller Transfer Taxes in NYC. Yes No Indicate to whom Real Estate Tax bills should be mailed Check one BankLender Owner Tenant Agent Name of Real Estate Tax Bill Recipient Address. This is designed to prevent the quick and savvy investor from simply buying at a low price and selling it to someone higher behind the sellers back.

Whether real estate transfer tax is payable on the sale of the Premises as a transfer by Original Seller to Purchaser for a consideration equal to the Original Purchase Price payable to Original Seller under the Contract. The newly added transfer tax. NEW YORK CITY DEPARTMENT OF FINANCE CENTRAL REGISTRATION 59 MAIDEN LANE 20TH FLOOR NEW YORK NY 10038 8.

4282019 The pertinent information for Wholesellers is Assignment of Agreements of Sale are subject to double taxation. Each subject to realty transfer tax. If this initial transfer is more than 2 years from the above date enter the date.

This is known as the mansion tax. 4142016 The New York State RPT is computed at the rate of 2 for each 500 of consideration for the transfer. For conveyances of real property located outside New York City file Form TP-584 Combined Real Estate Transfer Tax Return Credit Line Mortgage Certificate and Certification of Exemption from the Payment of Estimated Personal Income Tax with the county clerk where the property transferred is located.

5282008 The revised bulletin provides that the realty transfer tax will not apply to the assignment of an agreement of sale to a real estate companys SPE so long as the following requirements are met. The NYC Real Property Transfer Tax RPTT is 1 to 1425 for residential deals. Other real property transfers in cities of 1 million or more for 2000000 or more.

You must also pay RPTT for the sale or transfer of at least 50 of ownership in a corporation partnership trust or other entity that ownsleases property and transfers of cooperative housing stock shares. The initial agreement of sale expressly states that the buyer is acting on behalf of a yet-to-be-formed SPE. If the assignment itself is going to be considered a transfer and taxed accordingly it should remain in effect in both of the aforementioned situations.

Simple Home Purchase Agreement Elegant Agreement Template Category Page 13 Efoza Real Estate Contract Purchase Agreement Purchase Contract

Assignment Of Option To Purchase Real Estate Assignment Contract Basics For The Real Estate Investor

Real Estate Contract The Most Interesting New Real Estate Construction Technology Trends

Land Purchase Agreement Form Pdf New Sample Land Contract Agreement 9 Examples In Word Pdf Contract Template Purchase Agreement Real Estate Contract

Irrevocable Power Of Attorney Forms Inspirational Nationwide Legal Forms Securities Assignments P Power Of Attorney Form Power Of Attorney College Lesson Plans

Assignment Of Mortgage Smart Business Box Purchase Agreement Retail Store Smart Business

7 Step Fast Cash Formula Blueprint Wholesale Real Estate Real Estate Training Real Estate Coaching

Https Therealdeal Com Wp Content Uploads 2016 12 Cd15 0281 438 East 12th Street Condominium Offering Plan Screened Part11 Pdf

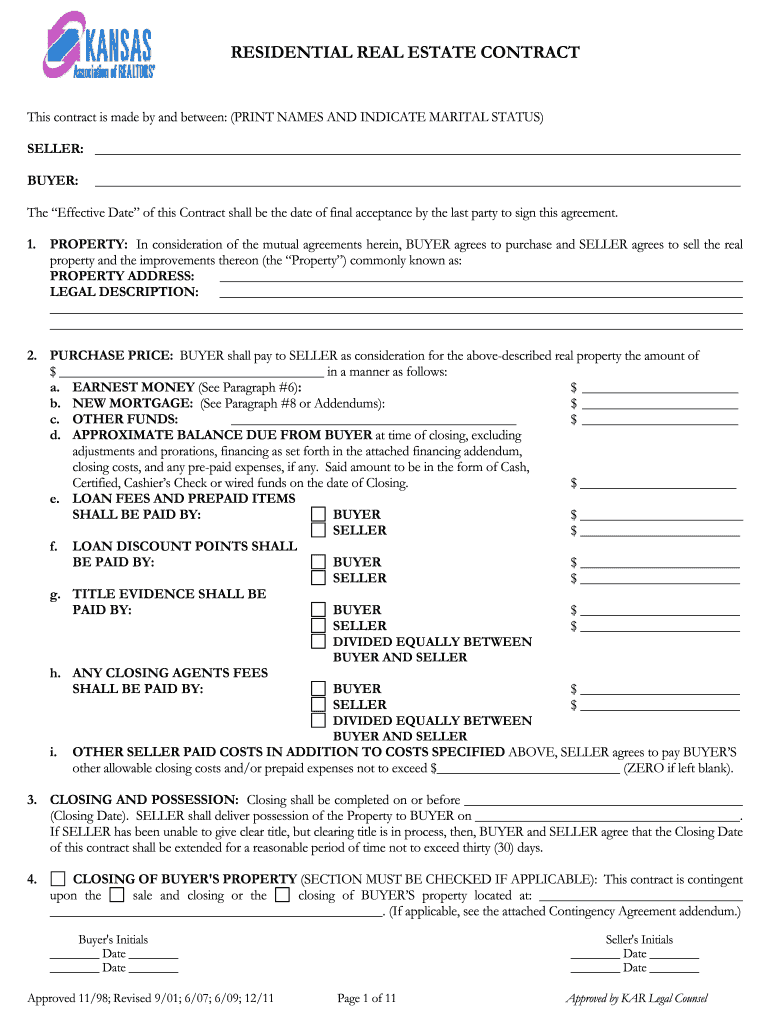

Kansas Real Estate Contract Fill Online Printable Fillable Blank Pdffiller

Wholesaling Made Simple A Comprehensive Guide To Assigning Contracts Retipster

Assignment And Assumption Agreement Template Lovely Contract Assignment Template Newgameplus Templates Medical Brochure Contract Template

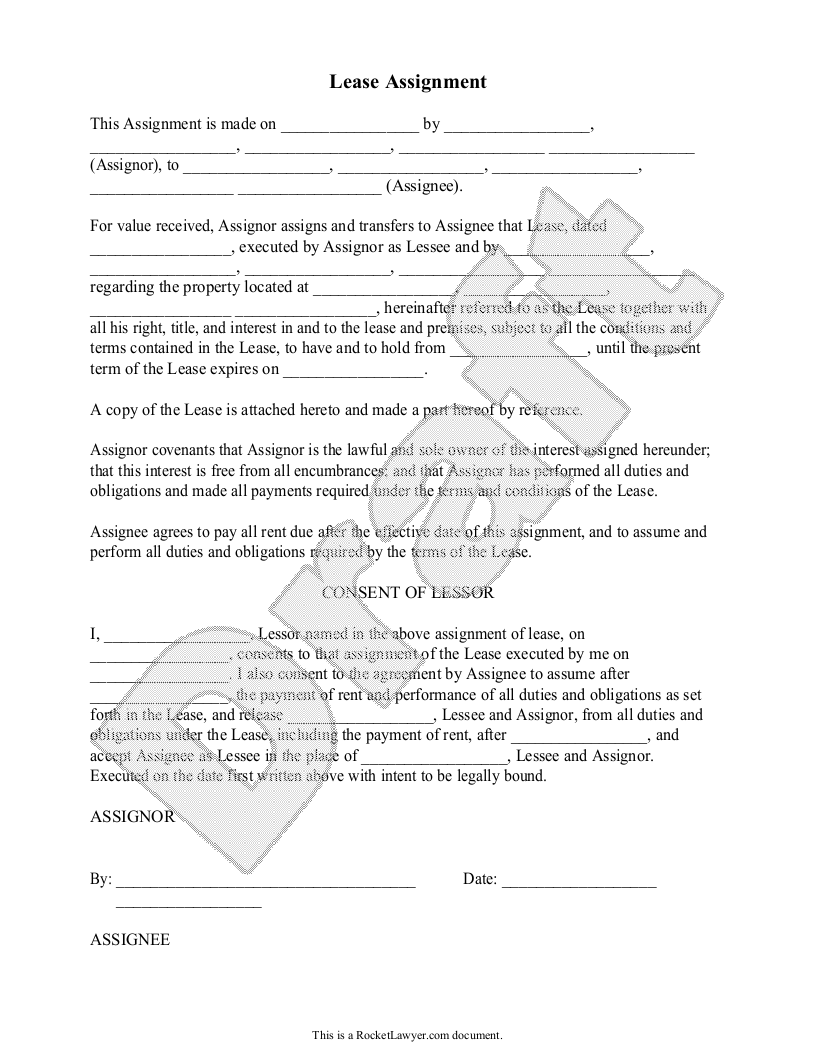

Free Lease Assignment Free To Print Save Download

Templates Trademark Assignment Agreement Templates Hunter Agreement Trademark Assignments