Nyc Transfer Tax Divorce

Nys And Nyc Real Estate Transfer Tax Overview For Nyc Nyc Real Estate Real Estate Infographic Nyc Infographic

Divorce Infographic Infographic Divorce Real Estate Infographic

Nyc Nys Transfer Tax Calculator For Sellers Hauseit

Nyc Nys Transfer Tax Calculator For Sellers Hauseit

Architecture In Sydney Infographic Portal Real Estate Infographic Architecture Victoria Building

Copy Of Birth Certificate Nyc Amazing Vitalchek Orders Birth Birth Certificate Template Birth Certificate Certificate Templates

The Importance of Tax-Affecting Earnings in Divorce.

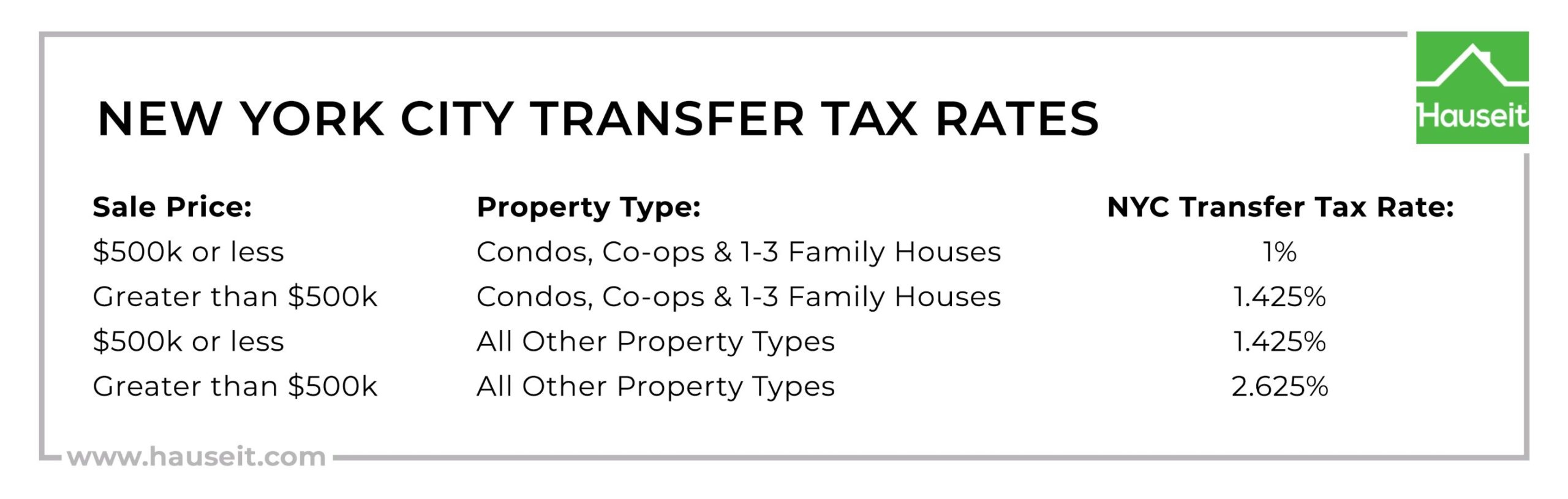

Nyc transfer tax divorce. CITE Pursuant to 19 RCNYSection 23-03 d 3 formally Article 24 c of the Real Property Transfer Tax regulations a transfer of real property from one spouse to the other pursuant to the terms of a sep-aration agreement or divorce decree is subject to transfer tax. 452019 The NYC transfer tax formally known as the Real Property Transfer Tax RPTT must be paid whenever real estate is transferred between two parties. 2182020 The NYC Real Property Transfer Tax RPTT generally applies to the delivery of a deed xv by a grantor to a grantee when the consideration for the real property exceeds 25000.

But what of conveyances made pursuant to divorce decree or separation agreement. Further the transfer of capital assets. Should the transferee be exempt from the tax the transferor would become liable.

Ad Book a New York Airport Transfer. In the absence of evidence estab-. The NYC-RPT instructions state that an existing mortgage will be excluded in all transfers pursuant to gifts or divorce As with any conveyance a failure to pay transfer taxes will be penalized.

Full Refund Available up to 24 Hours Before Your Tour Date. The state of New York or any of its agencies instrumentalities political subdivisions or public corporations including a public corporation created pursuant to agreement or compact with another state or the Dominion of Canada. What About a Flip Tax.

182016 A conveyance from one spouse to the other pursuant to the terms of a divorce or separation agreement is subject to tax While the NYS transfer tax form TP-584 does not directly deal with this type of transfer like the NYC-RPT does the State still requires the parties to calculate and pay transfer taxes. The transfer of an asset as part of a divorce is not considered a sale in the eyes of the IRS. Outside of NYC a statewide transfer tax applies.

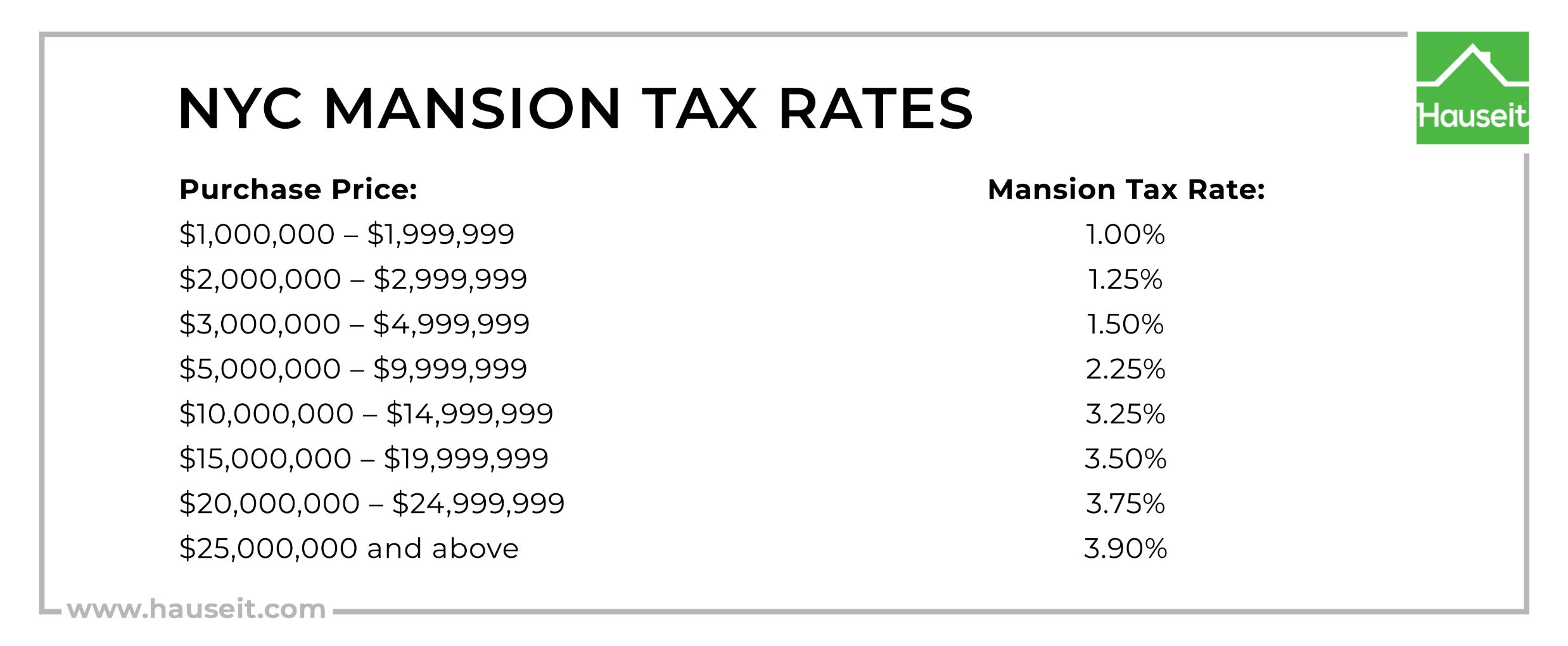

Therefore the recipient of the asset takes on the transferors adjusted tax basis in the asset. A The following shall be exempt from payment of the real estate transfer tax. There is a 250000 lifetime exclusion on the transfer of marital residence.

Nyc Nys Transfer Tax Calculator For Sellers Hauseit

Nyc Nys Transfer Tax Calculator For Sellers Hauseit

Nyc Nys Transfer Tax Calculator For Sellers Hauseit

Nys And Nyc Real Estate Transfer Tax Overview For Nyc Nyc Real Estate Real Estate Infographic Nyc Infographic

10 Essential Money Saving Tips For Canada 1st Time Home Buyers Infographic Portal Money Saving Tips Saving Tips Saving Money

Nyc Nys Transfer Tax Calculator For Sellers Hauseit

Pin On Additional Notices

A Sole Proprietorship Also Known As The Sole Trader Or Simply A Proprietorship Is A Type Of Business Entity That Is Sole Proprietorship Sole Trader Business

Employment Verification Form Template Awesome Work Experience Form Employee Tax Forms Business Plan Outline Legal Forms

Pin On Money Transfer Services

Nyc Nys Transfer Tax Calculator For Sellers Hauseit

Nyc Nys Transfer Tax Calculator For Sellers Hauseit

Nyc Nys Transfer Tax Calculator For Sellers Hauseit