Nyc Transfer Tax Mixed Use

Nyc Nys Transfer Tax Calculator For Sellers Hauseit

Nyc Mansion Tax Calculator For Buyers Interactive Hauseit

Nyc Nys Transfer Tax Calculator For Sellers Hauseit

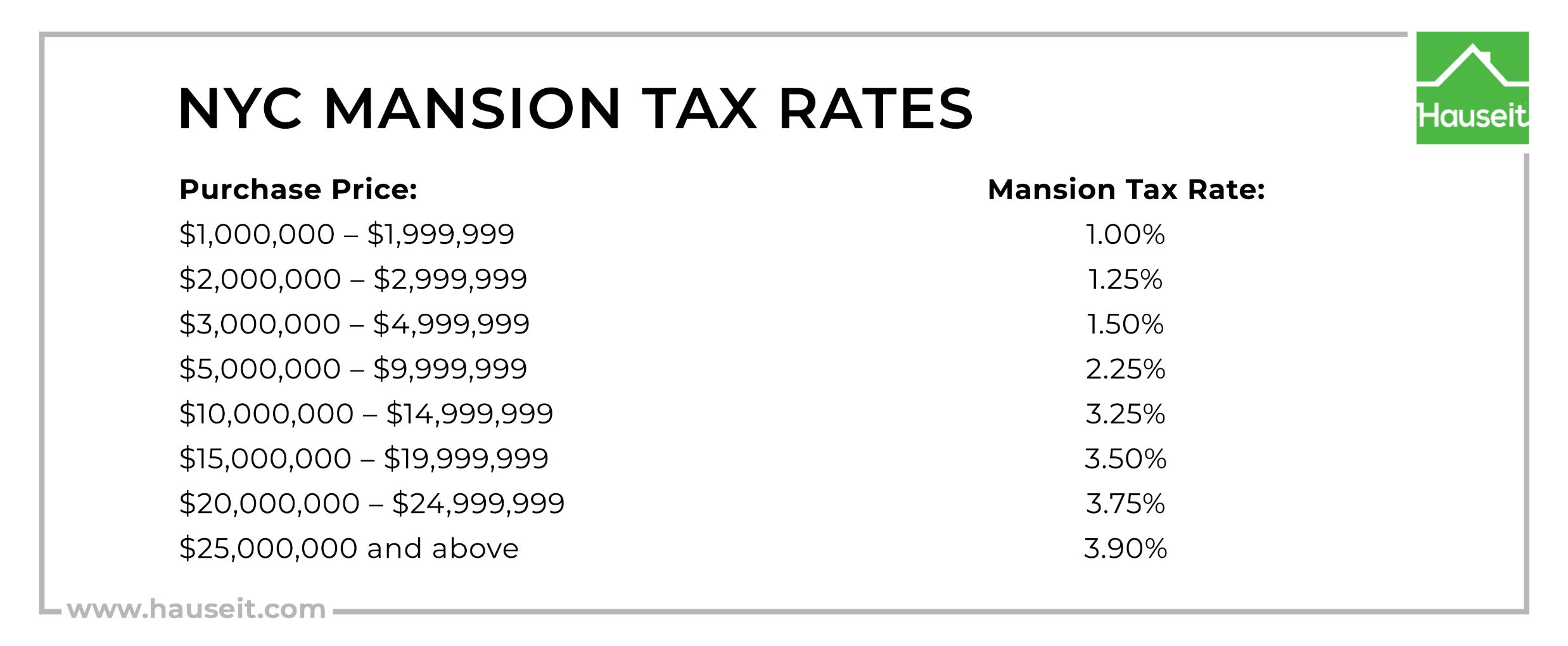

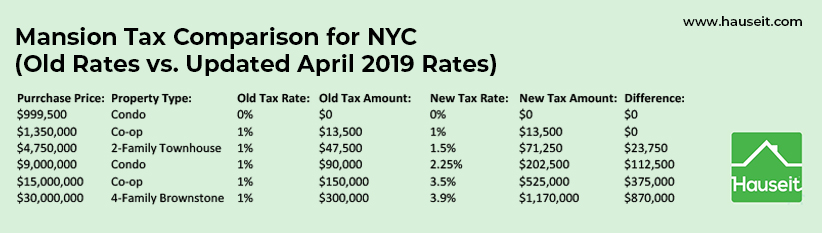

Nyc Mansion Tax Of 1 To 3 9 2021 Overview And Faq Hauseit

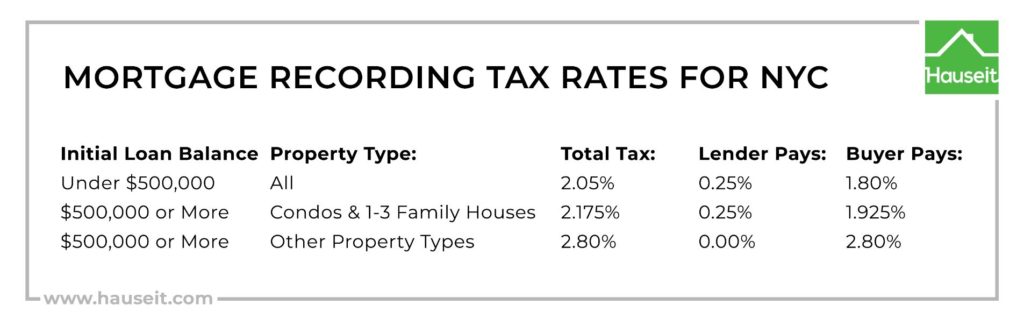

Nyc Mortgage Recording Tax Of 1 8 To 1 925 2021 Hauseit

Nyc Nys Transfer Tax Calculator For Sellers Hauseit

If the property cost more than 500000 the total transfer tax is 1825 to 2075 depending on the price.

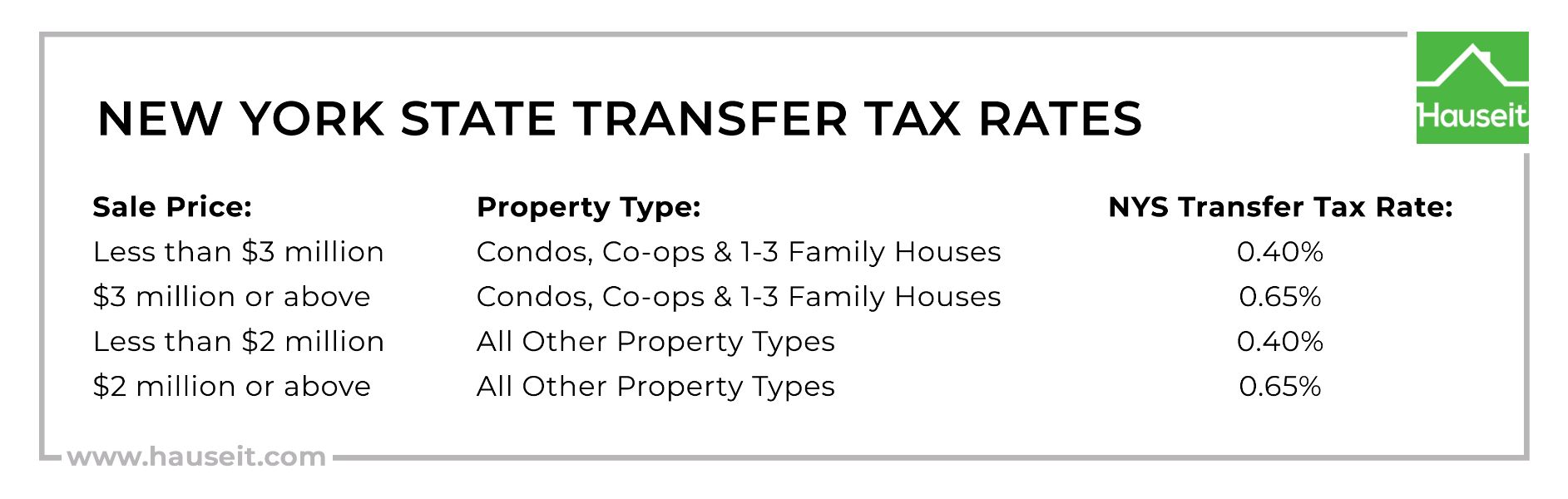

Nyc transfer tax mixed use. Sellers pay a combined NYC. Calculate Seller Transfer Taxes in NYC. The TSB also formalizes the Departments position that the Tax applies to mixed-use property to the extent that the real property is improved by a building containing not more than four family dwelling units.

11132017 By Dmitrii Gabrielov and Tim Gustafson. 452019 NYC transfer tax sales price is greater than 500000. An issue can arise if a taxpayer conveys a property that contains both residential and com-mercial use portions.

5312019 Mixed use properties will be treated as residential for purposes of the additional transfer tax. The distribution of a condominium unit by a limited liability company to one of its members will be exempt from New York City Real Property Transfer Tax as a transfer from a mere agent dummy straw man or conduit to. This is the way it is currently done.

Properties with sales prices of 1 million or more are subject to an additional real estate transfer tax of 1. The residential defined as a conveyance of a 1- 2- or 3-family house or an individual residential condominium unit. You must pay the Real Property Transfer Tax RPTT on sales grants assignments transfers or surrenders of real property in New York City.

The combined NYC and NYS Transfer Tax rates are 14 for sales of 500k or less 1825 for sales above 500k and below 3 million and 2075 for sales of 3 million or more. You must also pay RPTT for the sale or transfer of at least 50 of ownership in a corporation partnership trust or other entity that ownsleases property and transfers of cooperative housing stock shares. The TSB contains an example of a fact pattern which would trigger the requirement for the NYS Disclosure.

29 2014 the New York State Department of Taxation and Finance DTF issued an advisory opinion concluding that a substitution of property between a grantor and a grantor trust constituted a transfer for consideration and therefore the New York sales and use taxes were applicable to the transfer3 The commissioner held that if there is consideration given in any form in connection with the transfer a retail sale of tangible property occurs and sales tax. The NYC Real Property Transfer Tax RPTT is 1 to 1425 for residential deals. 8202018 In New York State the transfer tax is calculated at a rate of two dollars for every 500.

Mapping The Long Journey Of Nyc Solid Waste Video Video The Longest Journey Solid Waste Journey

Nyc Nys Transfer Tax Calculator For Sellers Hauseit

Nyc Nys Transfer Tax Calculator For Sellers Hauseit

Nyc Nys Transfer Tax Calculator For Sellers Hauseit

Nyc Nys Transfer Tax Calculator For Sellers Hauseit

Nyc Nys Transfer Tax Calculator For Sellers Hauseit

Whitehall Ferry Terminal Now Battery Maritime Building Aka Municipal Ferry Pier 1909 11 South St New York Ny Style Beau Building Whitehall Architect

Nyc Mansion Tax Of 1 To 3 9 2021 Overview And Faq Hauseit

با محبوبم در یک شهر زندگی می کنم بین ما چند خیابان چندین خانه یک پل هوایی دریاچه ای کوچک و صد ها هزار آدم New York Taxi Architecture Drawing Paint By Number

Pandemic Support Access Nyc

Gifts 5 8 Inch 5 0 Inch Mobile Phone Face Fingerprint Unlock Android9 1 Octa Core Dual Sim Cards Support T Card Du Phone Gift Sim Cards Smartphones For Sale

Pin Na Doske Goal

Nyc Neighborhood Economic Profiles Office Of The New York City Comptroller Scott M Stringer