Nyc Transfer Tax Statute

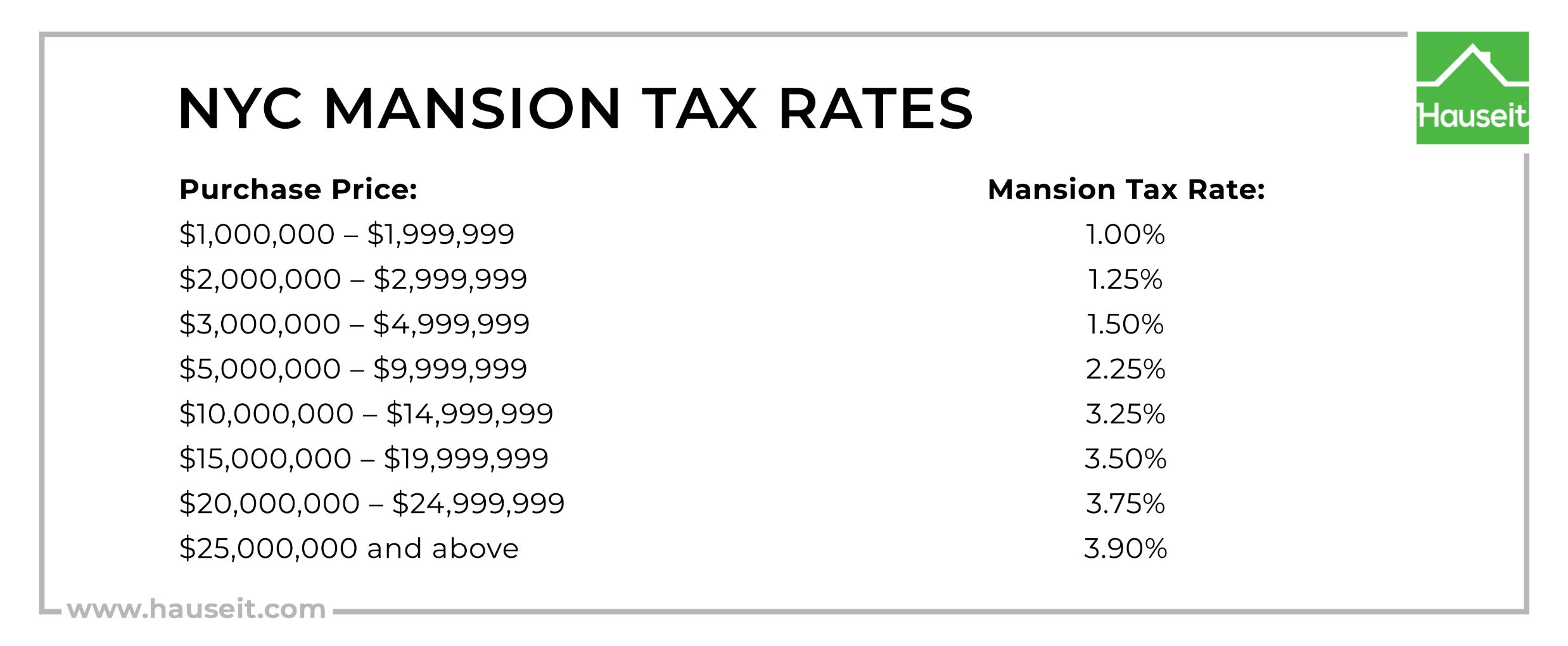

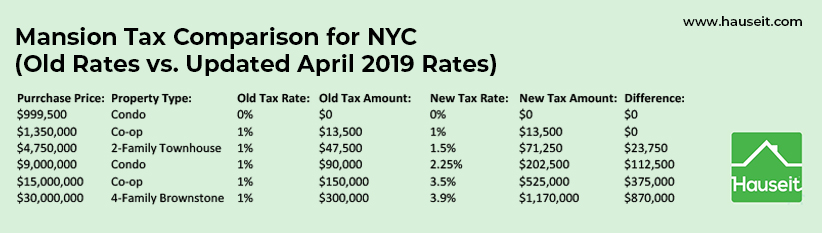

Nyc Mansion Tax Of 1 To 3 9 2021 Overview And Faq Hauseit

New York Transfer Tax Simplified

Transfer Tax Law Changes In New York City Elika Insider

Nyc Mansion Tax Of 1 To 3 9 2021 Overview And Faq Hauseit

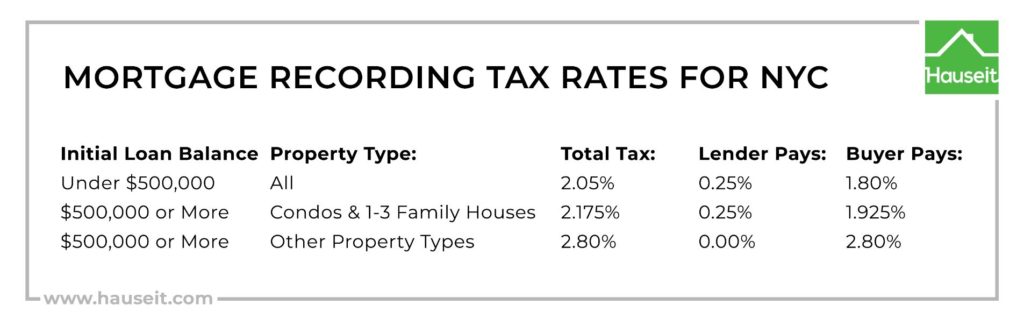

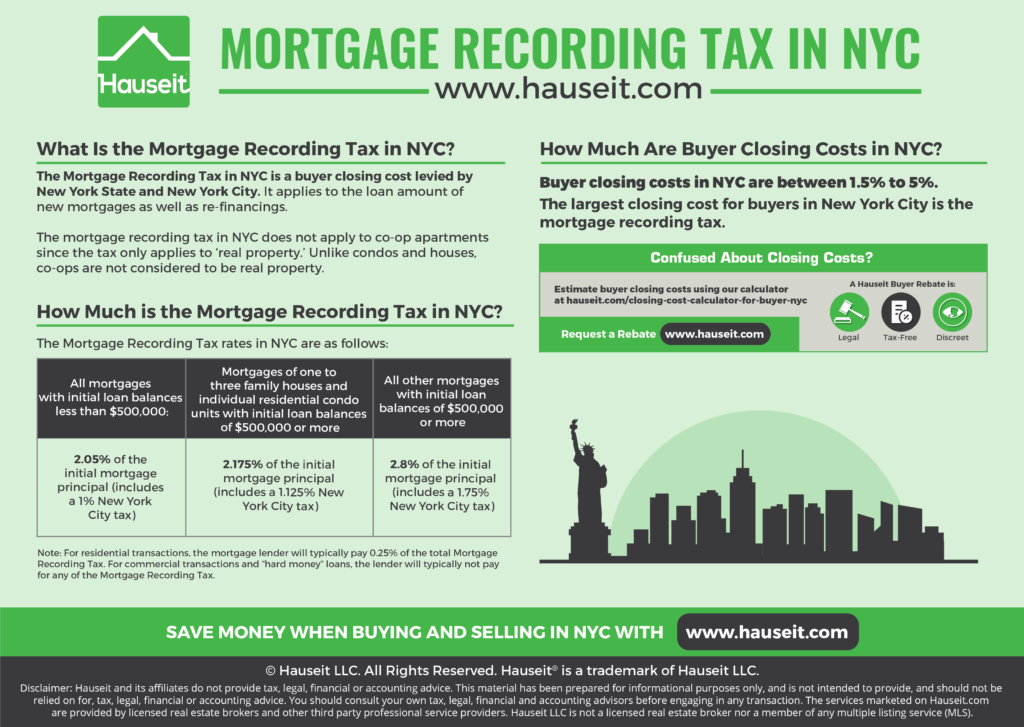

Nyc Mortgage Recording Tax Of 1 8 To 1 925 2021 Hauseit

Bluehost Com

452019 The NYC transfer tax formally known as the Real Property Transfer Tax RPTT must be paid whenever real estate is transferred between two parties.

Nyc transfer tax statute. 11-2102 - Imposition of tax. Buyers of residential properties priced at. New York City Administrative CodeNEW.

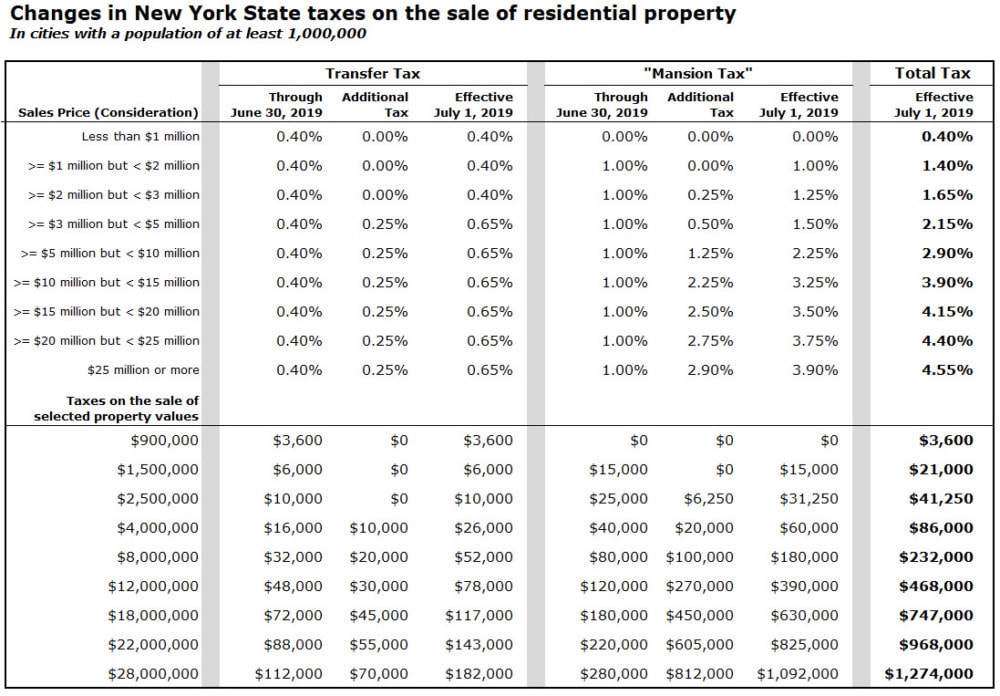

You must also pay RPTT for the sale or transfer of at least 50 of ownership in a corporation partnership trust or other entity that ownsleases property and transfers of cooperative housing stock shares. The tax is 2 for each 500. NY State Transfer Tax The New York State Transfer Tax is 04 for sales below 3 million and 065 for sales of 3 million or more.

11-2101 - 11-2118 Real Property Transfer Tax Chapter 21 - REAL PROPERTY TRANSFER TAX 11-2101 - Definitions. Currently these changes would only apply to real property located within the five boroughs of New York City. 8202018 In New York the seller of the property is typically the individual responsible for paying the real estate transfer tax.

Outside of NYC a statewide transfer tax applies. For certain qualified transfers to Real Estate Investment Trusts REITs the tax is reduced to 1 per 500 of consideration. Thus a total combined NYS and NYC rate applicable to such transfers is up to 5975 455 NYS 1425 NYC.

Real Property Law. 2006 New York Laws. 4152019 Further NYC continues to impose its own transfer tax rate of 1425 on residential real property for transfers for consideration of more than 500000.

NEW YORK STATE TRANSFER TAX The current rate of the New York State transfer tax RETT provided for in Section 1402 of the Tax Law is 04 200 per 50000 of consideration or 400 per 100000 of consideration. The state of New York or any of its agencies instrumentalities political subdivisions or public corporations including a public corporation created pursuant to agreement or compact with another state or the Dominion of Canada. 11-2103 - Presumptions and burden of proof.

Nyc Mansion Tax Of 1 To 3 9 2021 Overview And Faq Hauseit

Anita Perera Law Professional Corporation Brampton Lawyers Mississauga Lawyers Toronto Lawyers Estate Law Brampton Legal Advice

Free Printable Child Guardianship Forms Elegant Is Free Printable Custody Agreement Joint Custody Parenting Plan

Leave And Licence Agreement Http Propertyregistration Info The Landlords Need To Take All Necessary Precautions To Shield Their Agreement Lease Licensing

Panaflex Print Islamabad Mug Printing Thesis Binding Print

Reducing Refinancing Expenses The New York Times

New York City Taxes A Quick Primer For Businesses

Reviews Rates Fees And Rewards Details For The Keybank Business Rewards Credit Card Compare To Other Cards And A Rewards Credit Cards Compare Cards Business

How Much Annual Income Can Your Retirement Portfolio Provide Balance Transfer Credit Cards Loans For Poor Credit Retirement Portfolio

What Is The Average Co Op Flip Tax In Nyc And Who Pays It By Hauseit Medium

Nyc Mortgage Recording Tax Of 1 8 To 1 925 2021 Hauseit

New York City Taxes A Quick Primer For Businesses

Pin On Solutions Manual