Real Property Transfer Tax Nj

Https Www Bracheichler Com Wp Content Uploads 2019 12 Gladstone Ecepc Presentation Pdf

Real Estate Transfer Taxes Deeds Com

Registry Division

Tax Collector S Office City Of Englewood Nj

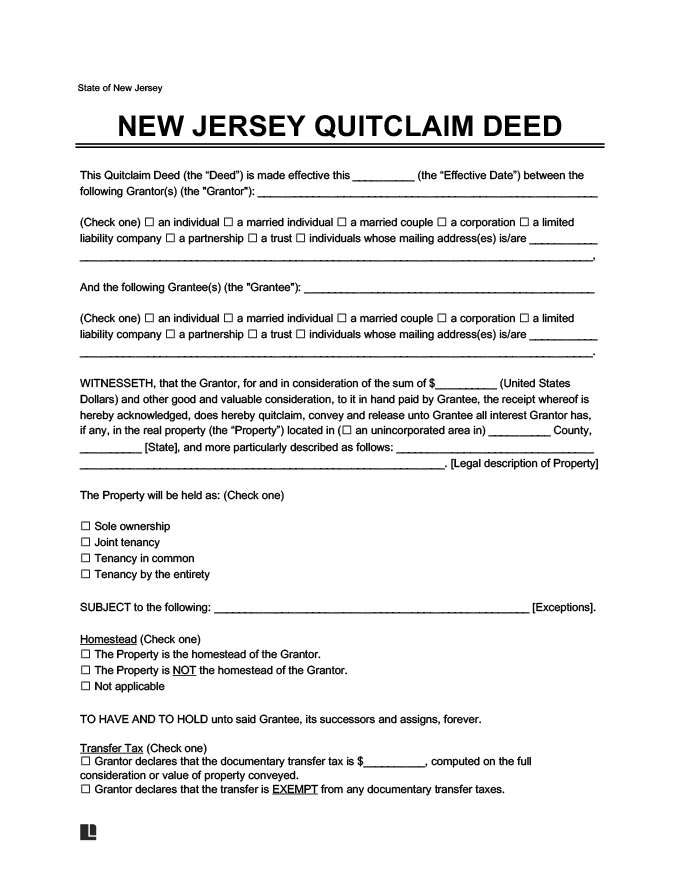

Free New Jersey Quitclaim Deed Form How To Write Guide

Department Finance

9252020 While many real estate taxes can be deducted at the end of the year transfer taxes in New Jersey are not able to be deducted.

Real property transfer tax nj. In both cases the real property has a full equalized assessed value of 1000000. On the transfer of title of real property said Jonathan Donenfeld a certified public accountant with. It should be noted that if a deed is recorded and it is determined later that additional RTF fees are due the deed is still valid and the buyers status as Bona Fide Purchaser is not affected.

11282011 The fee schedule can be found on the states Division of Taxation web site statenjustreasurytaxation and a Google search will yield many online calculators to help you calculate the tax. What is the realty transfer fee. 11252012 The reason the Tax Court found that the regulation was applied inconsistently is easily demonstrated with an example.

The CIT is only imposed if the real property is classified as 4A Commercial and if the consideration or other valuation of the real property is. It is due at the time of the deed transfer. Residents and domiciles for real property located in New Jersey.

In addition to the city tax New York state imposes a tax on all deeds and transfers of real property but at a different rate. In that case it is also exempt from the mansion tax. At the recording of a deed for the transfer of real property in New Jersey the Realty Transfer Fee is imposed on the seller and the Mansion Tax may be imposed on the buyer.

The RTF is calculated based on the amount of consideration recited in the deed or in certain instances the assessed valuation of the property conveyed divided by the Directors Ratio. 4615-5 et seq The Realty Transfer Fee is imposed upon the recording of deeds evidencing transfers of title to real property in the State of New Jersey. 10202014 The CIT Law imposes a one percent fee CIT on the transfer of a controlling interest in an entity that owns certain real property.

The only exception occurs if the property is used as an investment or rental property in which case the seller could deduct them as a work expense. Imposes a realty transfer fee RTF on the seller of real property for recording a deed for the sale. Neither the seller or buyer can deduct transfer taxes on their taxes.

New Jersey Exit Tax Moving Out Of State Tax Considerations

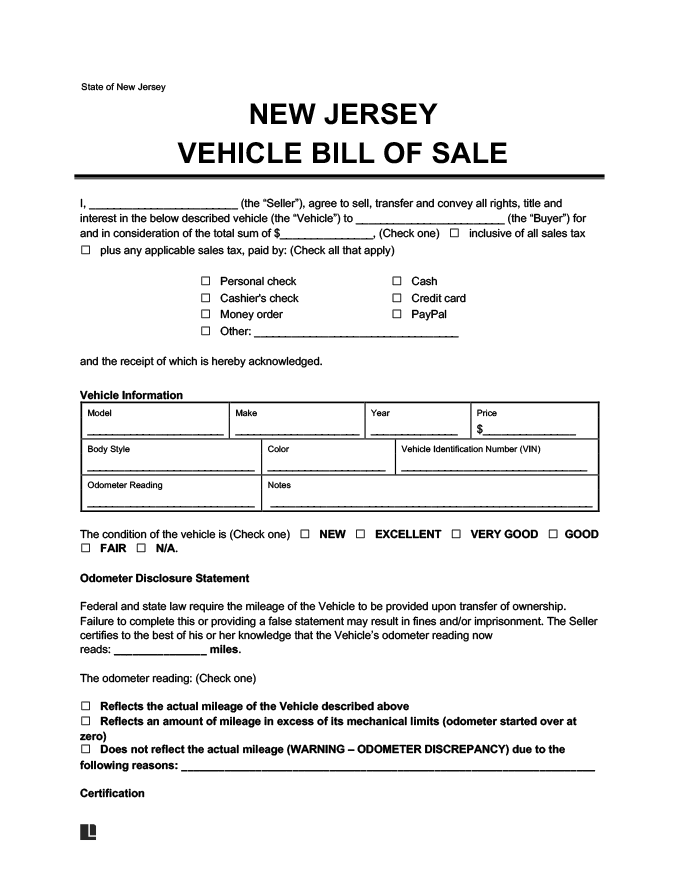

Free New Jersey Bill Of Sale Form Pdf Template Legaltemplates

Department Finance

Guide To Valid And Enforceable Deeds In New Jersey

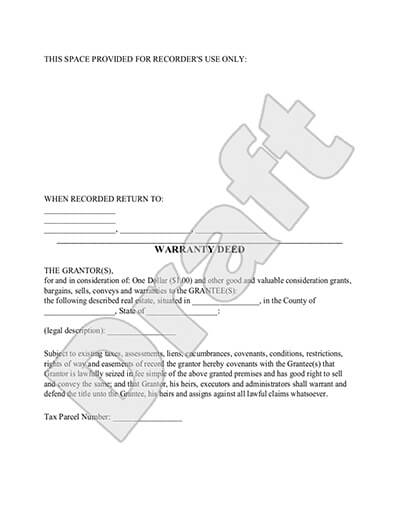

Free Warranty Deed Free To Print Save Download

Need A Inheritance Tax Waiver Form Templates Here S A Free Template Create Ready To Use Forms At Formsbank Com Inheritance Tax Tax Forms Estate Tax

The Nj Realty Transfer Fee What It Is And How Much It Will Cost You Propertyclub

Should I Sign A Quitclaim Deed During Or After Divorce

New Jersey Quit Claim Deed Form In 2020 Quites New Jersey Jersey

Quitclaim Deed Information Guide Examples And Forms Deeds Com

Tax Collection Middletown Nj

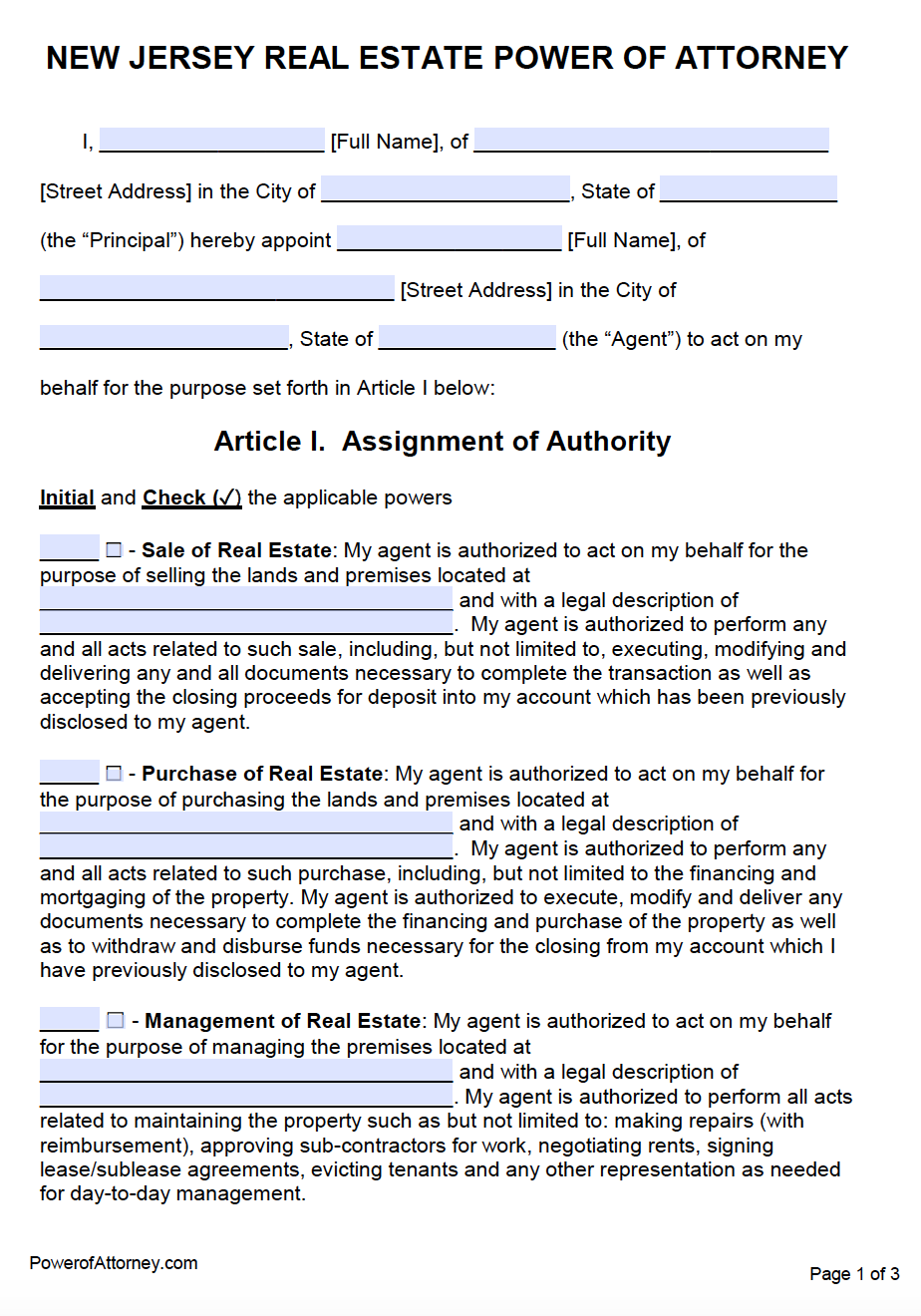

Free New Jersey Power Of Attorney Forms Pdf Templates

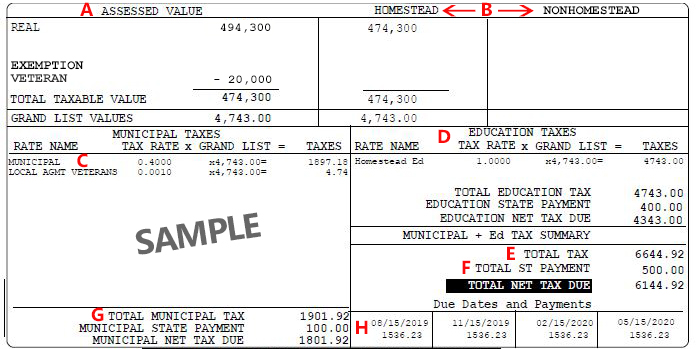

Understanding Your Property Tax Bill Department Of Taxes