Transfer Definition Income Tax

Transfer Pricing Meaning Examples Objectives Purpose

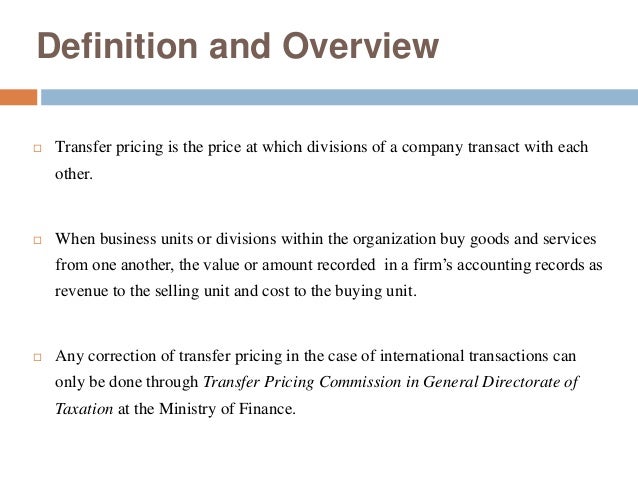

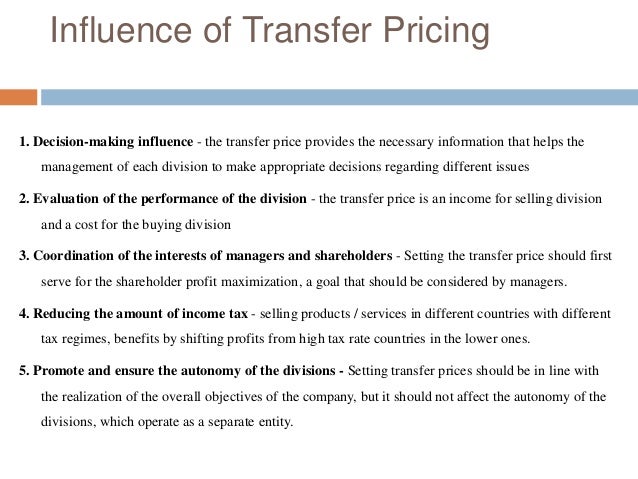

Transfer Pricing

Slump Sale And Its Taxability

Transfer Pricing

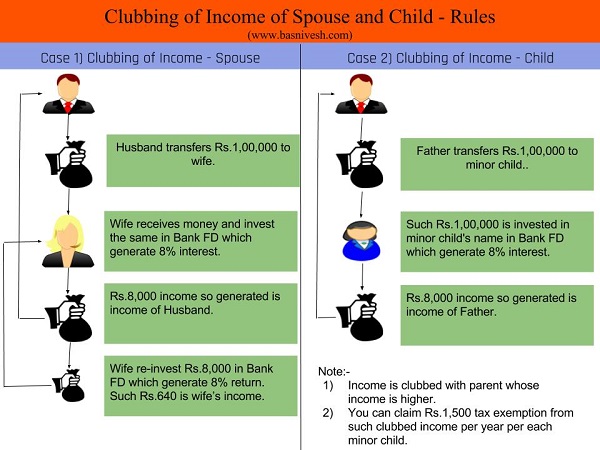

Clubbing Of Income Of Spouse And Child Tips To Save Tax Basunivesh

Clubbing Of Income Of Spouse And Child Tips To Save Tax Basunivesh

INCOME TAX ACT 58 OF 1962 the Act SECTION.

Transfer definition income tax. 8112009 A transfer tax is imposed on tax on the sale donation barter or any other mode of transferring ownership or title of real property at the maximum rate of 50 of 1 75 of 1 in the case of cities and municipalities within Metro Manila of the total consideration involved in the acquisition of the property or of the fair market value in case the monetary consideration involved in the transfer. Transfer and Revocable Transfer defined Amended and updated notes on section 63 of Income Tax Act 1961 as amended by the Finance Act 2020 and Income-tax Rules 1962. An involuntary sale of a property of a debtor by a court at the instance of a decree holder is also transfer of a capital asset.

By law taxpayers must file an income tax return annually to. What is Transfer Pricing. Transfers of tangible and intangible assets are generally subject to income tax with the determination of tax liability dependent on the nature of the holding revenue assets capital assets or trading stock.

In this video I have explained when a transaction is said to be transfer as per Income Tax Act. 1282020 Income tax is a type of tax that governments impose on income generated by businesses and individuals within their jurisdiction. The sale need not be voluntary.

ALIENATION OF INCOME -- Term generally used to describe the transfer of the right to receive income from a source while not necessarily transferring the ownership of. It is usually not deductible from federal or state income taxes although it may. Detail discussion on provisions and rules related to Transfer and revocable transfer defined.

You live outside Canada throughout the tax year. Do not have significant residential ties in Canada. 11152020 Section 63 of Income Tax Act.

Usually there is a tendency among MNCs to adjust their international transactions in such a way that maximum profit arises in that country where the rate of tax is lowest and minimum profit arises in that country where the rate of tax. In relation to a capital asset includes the sale exchange or relinquishment of the asset or the extinguishment of any rights therein or the compulsory acquisition thereof under any law. SECTIONS 11 DEFINITION OF GROSS INCOME 11a 23g AND 28.

What Is Domestic Transfer Pricing

List Of Relatives Covered Under Section 56 2 Of Income Tax Act 1961

Determination Of Period Of Holding Of Capital Asset Short Term Or Long Term

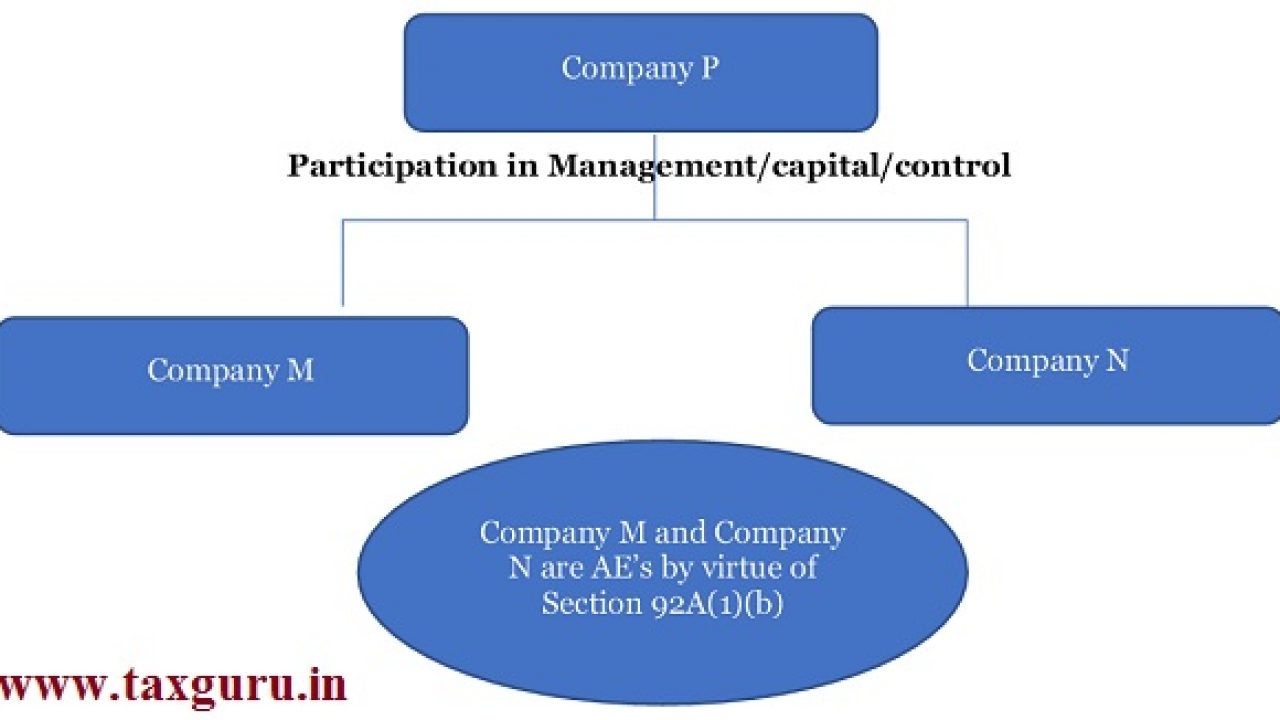

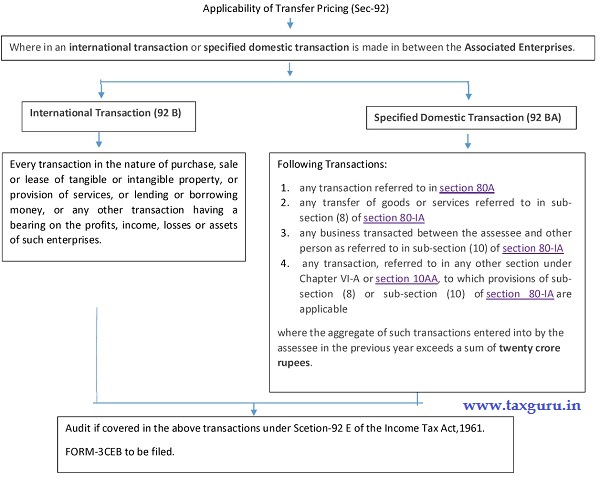

Transfer Pricing Audit Applicability In India

Concept Of Capital Gains In Case Of Joint Development Agreement

Income From Other Sources Casual Income Residual Dividend Income

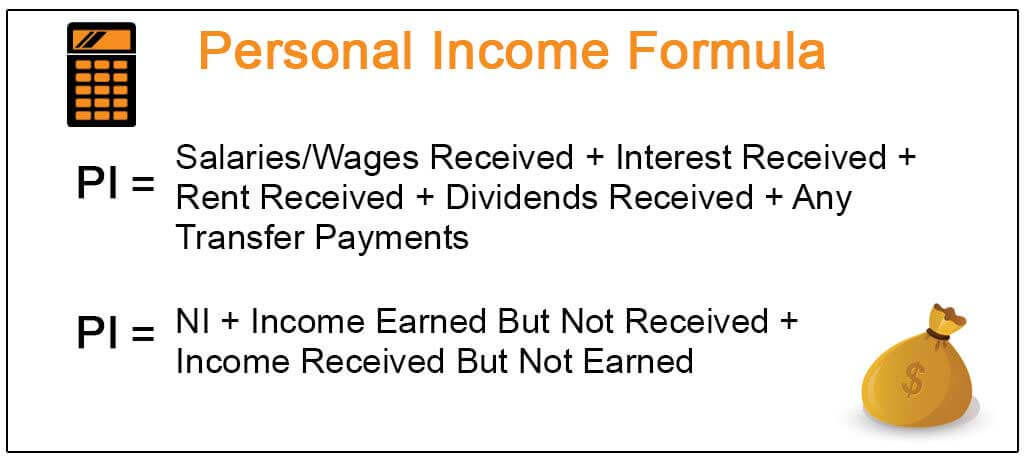

Personal Income Definition Formula How To Calculate

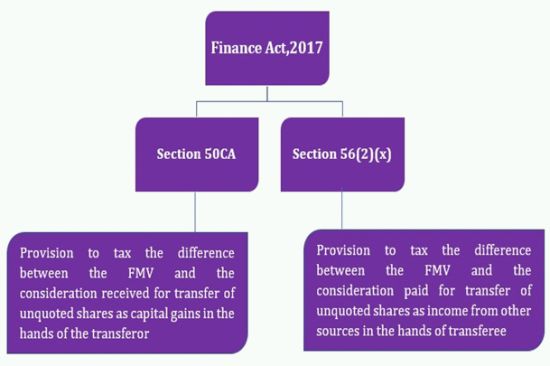

Sale Transfer Of Unquoted Shares Get Your Valuation Right Tax India

Tax Audit Under Section 44ab

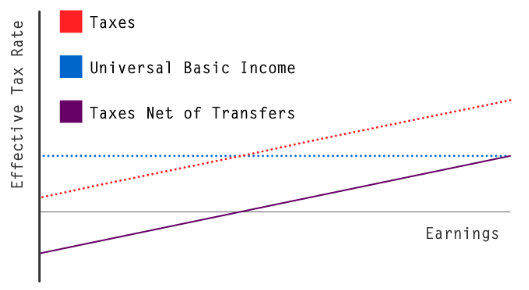

Universal Basic Income Is Just A Negative Income Tax With A Leaky Bucket Niskanen Center

Deemed Owner Of House Property Section 27

Taxation In South Africa Wikipedia

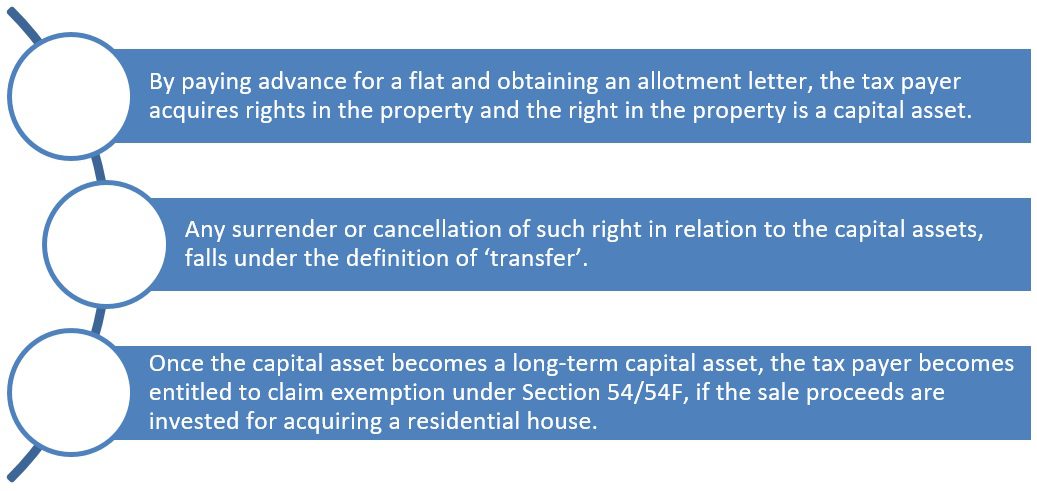

Are Profits On The Cancellation Of A Property Deal Taxable Housing News