Transfer Definition Under Capital Gain

How To Save Capital Gains Tax On Property Sale Capital Gain Capital Gains Tax Tax

A Brief Idea On Capital Gain Taxes On Mutualfunds Capital Gains Tax Capital Gain Finance Investing

Capital Gains Ppt

Slump Sale And Its Taxability

Capital Gains Ppt

The Beginner S Guide To Capital Gains Tax Infographic Transform Property Consulting Capital Gains Tax Capital Gain Tax

But Income Tax Act 1961 has given some relief in the form of exemptions.

Transfer definition under capital gain. Such transfer should take place during the previous year. Such profit or gain should not be exempted from tax under sections 54 54B 54D. The capital asset should be transferred by the assessee.

A capital gain arises only when a capital asset is transferred. 1142019 The transfer of such capital asset. The sale need not be voluntary.

152018 Conditions for Gains to be charged under Capital Gains There should be a capital asset. In this video I have explained when a transaction is said to be transfer as per Income Tax Act. From above definition we can understand that the term Transfer under the Income Tax is mainly important to work out tax liability arising under the head.

Capital gains tax only applies to profits from the sale of assets held for more than a year referred to as long term capital gainsThe rates. A profit earned as a result of this transfer. 7302019 Capital gain is an increase in a capital assets value.

I sale exchange or relinquishment of the asset or ii the extinguishment of any tight therein or iii the compulsory acquisition thereof under any law or. Capital Asset includes land building plant and machinery share and debenture etc. Where in Holder of TDR transfer the TDR generated from waving the right surrendering the eligible area to the requisite Developer for Construction.

11262020 Capital gain arises on transfer of a capital asset. When capital gain arises then it is chargeable to tax and you have to pay tax on gain on transfer of capital asset. Transfer of Capital Assets to arise Capital Gain Capital Gain should arise in the previous year in which Transfer took place.

Concept Of Capital Gains In Case Of Joint Development Agreement

Deduction Under Capital Gains

Irr Internal Rate Of Return Definition Example Financial Calculators Balance Transfer Credit Cards Credit Card Transfer

How Rich Save Taxes Finance Capital Gain Tax

Bill Of Exchange Notary Public Negotiable Instruments Bills

Ten Mistakes You Should Avoid To Save On Tax Under Income Tax Act Of India Investing Income Tax Capital Gains Tax

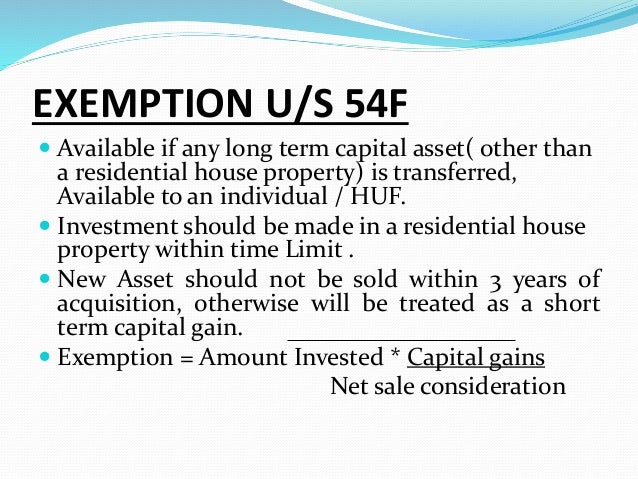

Section 54f Capital Gain Tax Exemption

Capital Gain On Conversion Of Capital Asset Into Stock In Trade

Ultimate Guide To Capital Gains Tax Exemption U S54 In A Video Watch It To Know About It Capital Gains Tax Capital Gain Gain

Cleartax 39 S Guide To Tax Implications On Capital Gains From Sale Of Shares House Property Capital Gain Capital Gains Tax Gain

Determination Of Period Of Holding Of Capital Asset Short Term Or Long Term

What Is The Meaning Of Legal Tender Used In Rule 6dd Http Taxworry Com Meaning Legal Tender Used Rule 6dd Legal Tender Capital Gains Tax Taxact

Taxation Of Capital Gains New Taxbuddy