Transfer On Death Stock Cost Basis

What Is A Step Up In Basis Cost Basis Of Inherited Assets

Avoiding Basis Step Down At Death By Gifting Capital Losses

Avoiding Basis Step Down At Death By Gifting Capital Losses

Guide To Calculating Cost Basis Novel Investor

Http Www Bairdfinancialadvisor Com Thelilesgroup Mediahandler Media 317117 Tax 20 205 20 20basis 20adjustments 20at 20death Pdf

Strategies To Preserve Step Up In Cost Basis Under New Tax Landscape Putnam Investments

Is it better to sell stock in trust and pay taxes or transfer in-kind to beneficiaries and have them pay taxes whenever they sell.

Transfer on death stock cost basis. If the assets dropped in value after you inherited them you may. If the shares were purchased after 1985 you inherit the cost base of the prior owner. The annual gifting limits of 15000 per person 30000 for a joint gift with your spouse apply and.

Find the Information Youve Been Searching For. 12182020 To receive the investments after the account holder passes away the beneficiaries of a TOD account will need to provide the investment company with an original death certificate for the owner. Ad Learn more About Finance and Take Control of Your Finances.

Stock held in irrevocable trust which needs to be terminated and sitributions made because of death. Any shares you inherit receive this step up which resets the cost basis of the shares to their fair market values as of the deceaseds date of death. 1252006 Stepped-up basis refers to the fact that the IRS allows you to use the closing stock price or fund at the date of the deceased owners death.

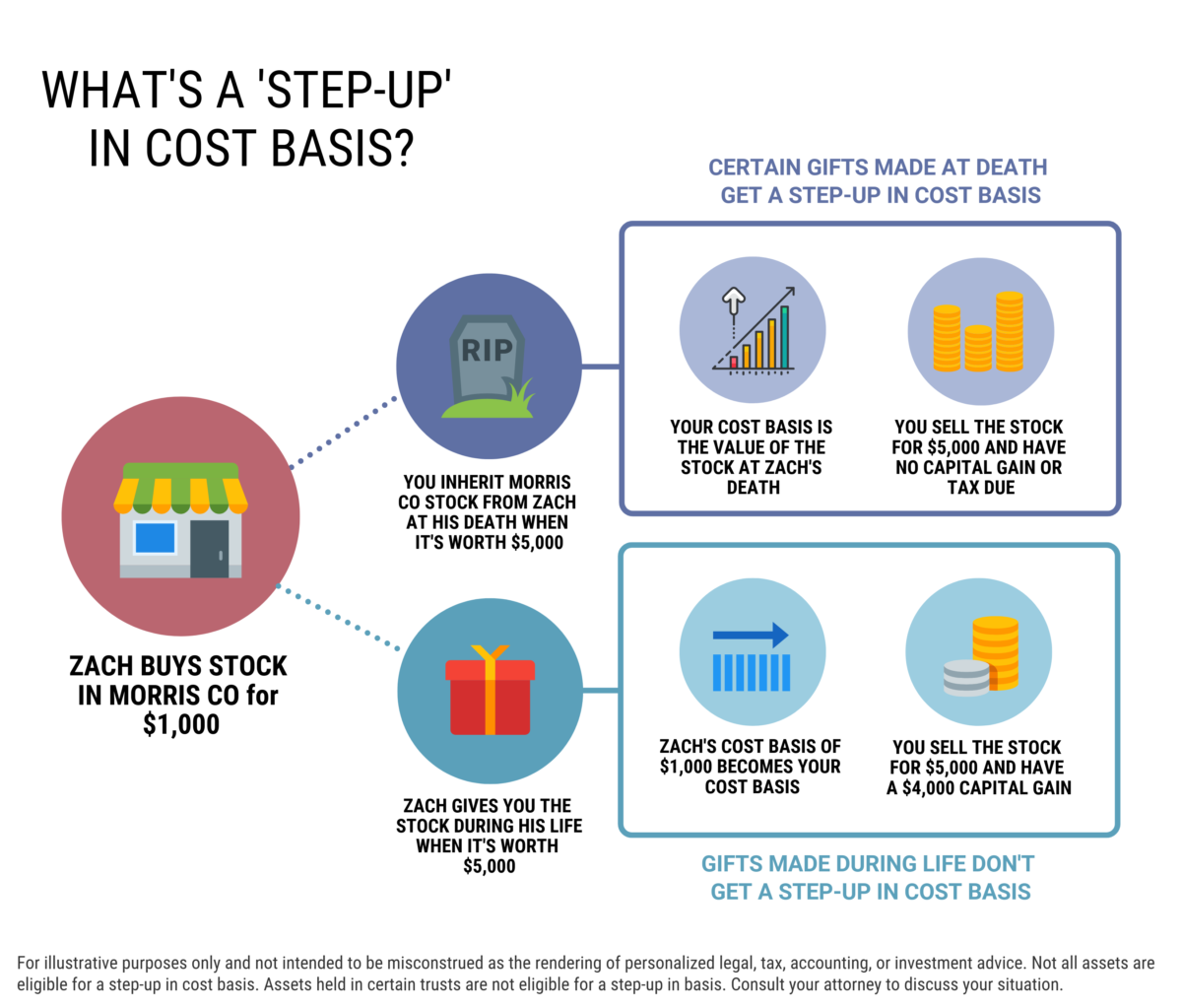

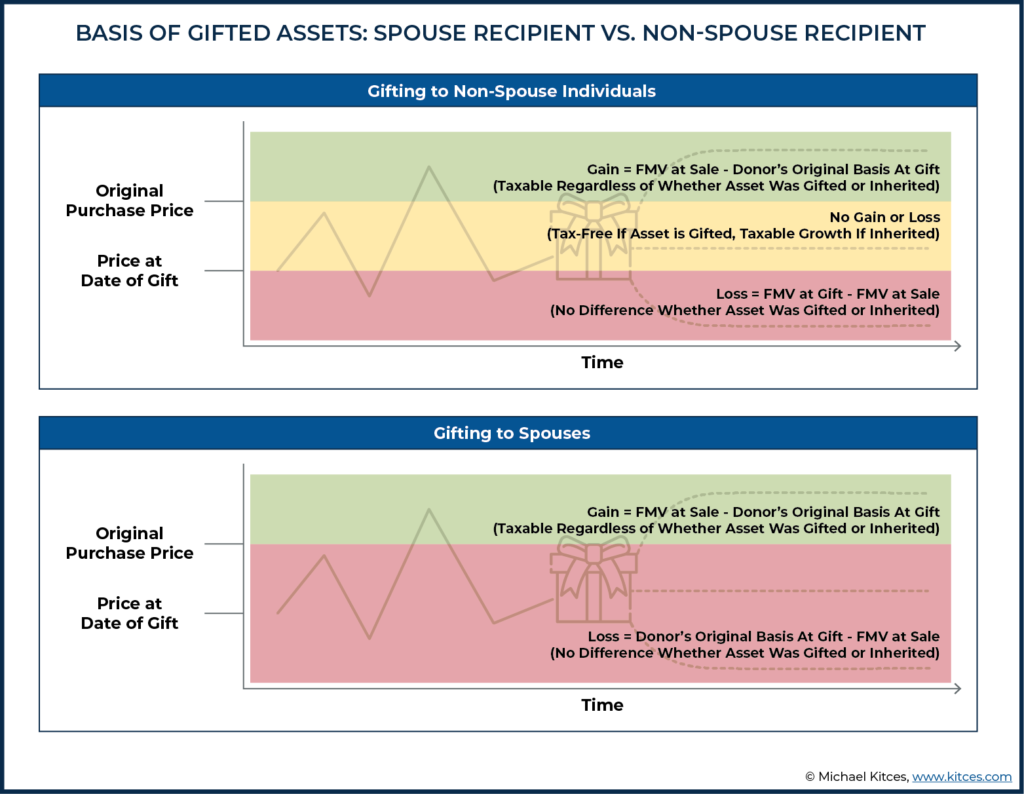

9102017 Mom had every intention of passing these assets to her children knowing that on her death the cost basis the original value for tax purposes would reset to. 152013 The cost basis for inherited stock is usually based on its value on the date of the original owners death -- whether it has increased or lost. Pankowski is correct - stepped-up basis is a result of the asset passing at death versus during life a lifetime gift.

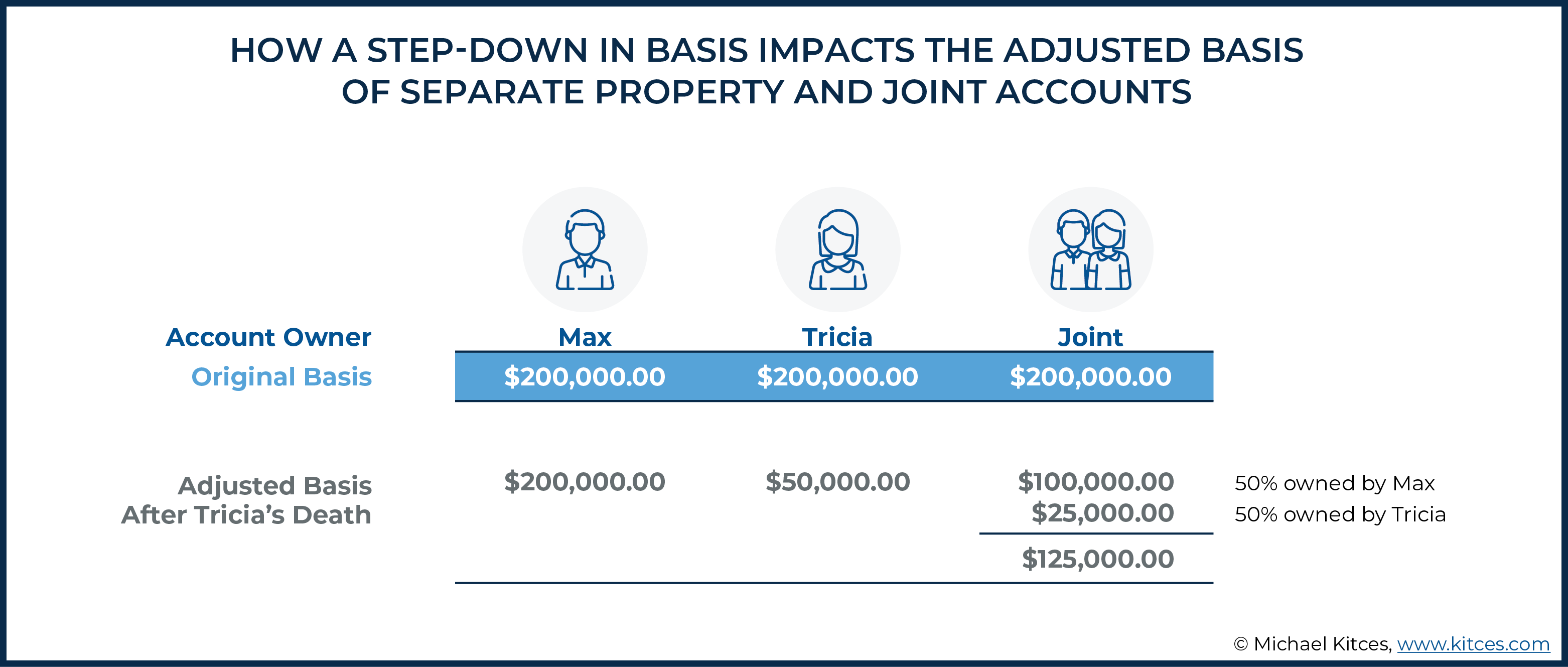

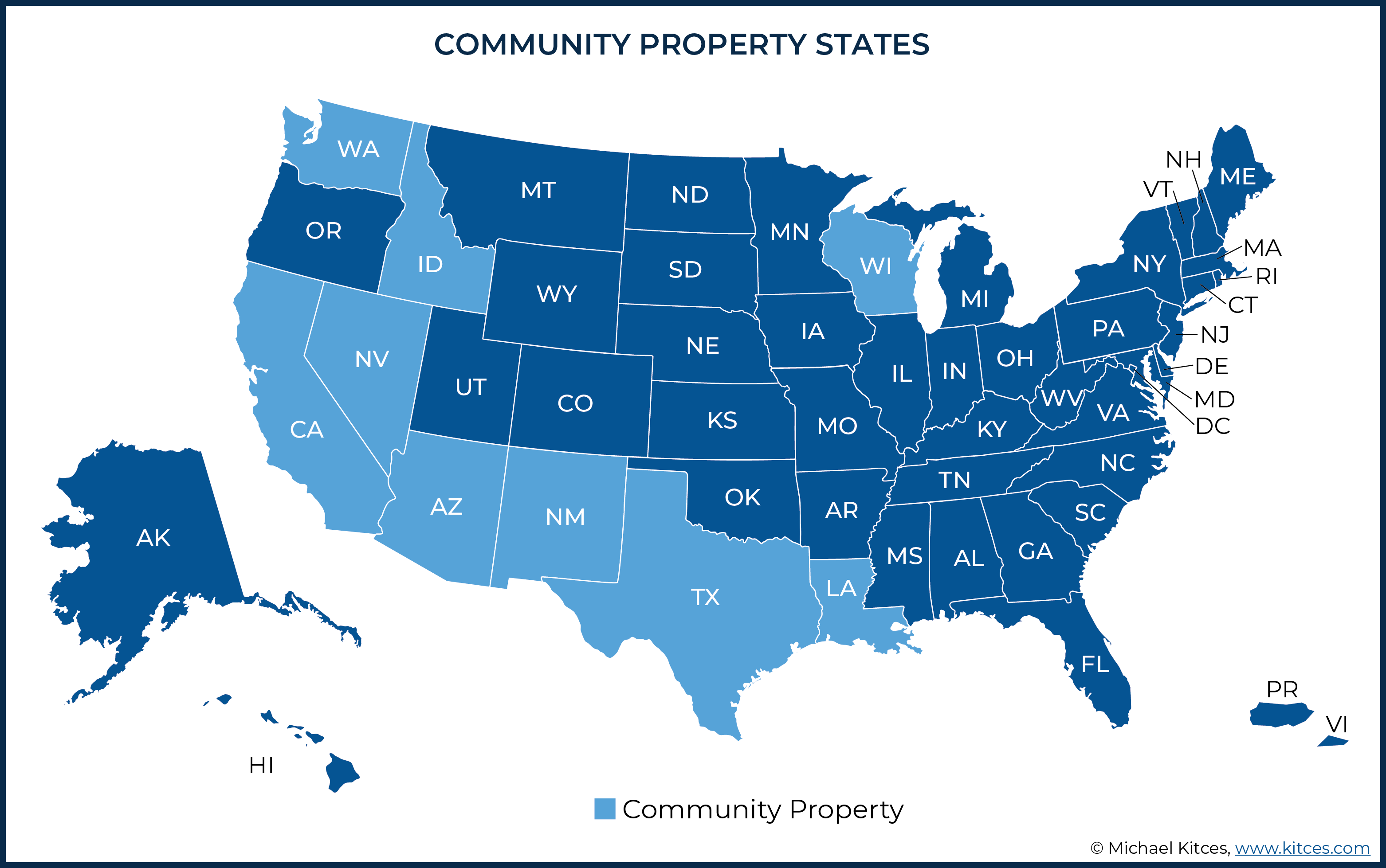

611999 In California and other community-property states the cost basis of all the stock held jointly in a husband-wife account is normally changed to the price on the date of the first spouses death. Stock A 52896 19861 shrs 23624 46921 Stock A 4197 047 shrs 30 141. 612019 It is worth 200 at the date of death of the decedent.

Find the Information Youve Been Searching For. 612019 Stock cost basis 10. So the inherited basis is 100 200 2.

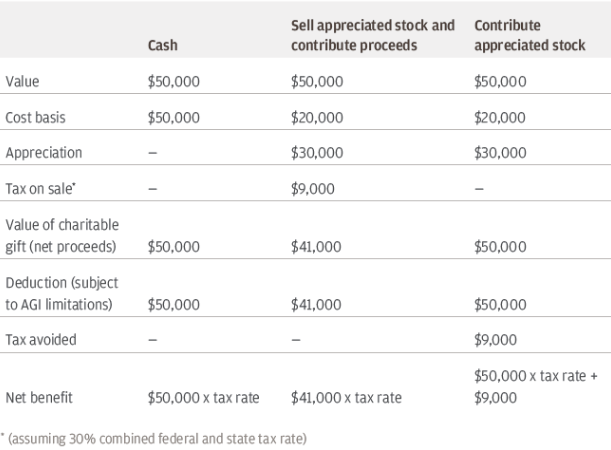

Selecting The Right Assets To Give To Charity

Https Www Raymondjames Com Soundwealthmanagement Pdfs Carryover Pdf

Avoiding Basis Step Down At Death By Gifting Capital Losses

Guide To Calculating Cost Basis Novel Investor

/dotdash_Final_Trust_Aug_2020-01-6b0686cb892a40589605baeeef79a183.jpg)

Trust Definition

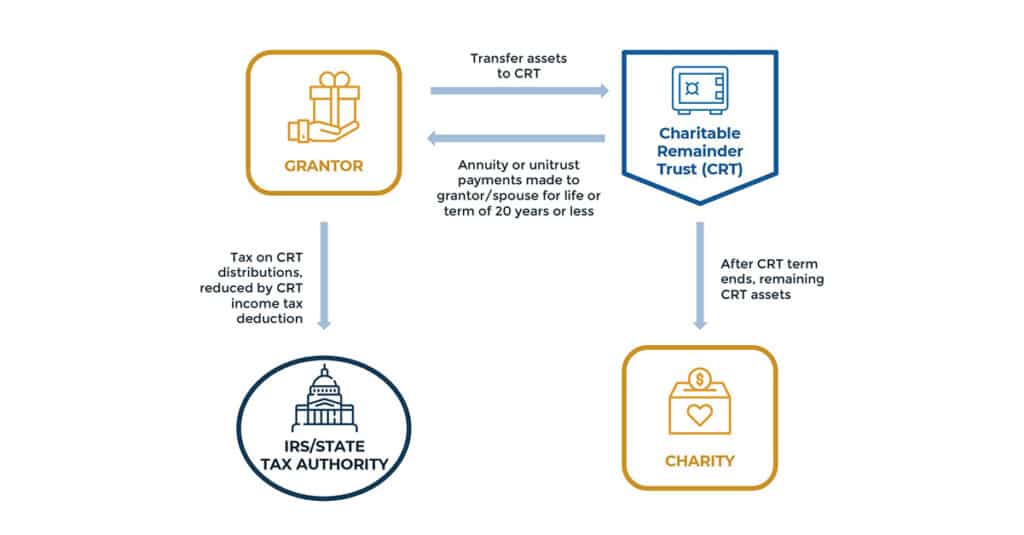

Charitable Remainder Trusts Crts Wealthspire

Texas Tod Deed Form Create A Transfer On Death Deed Online

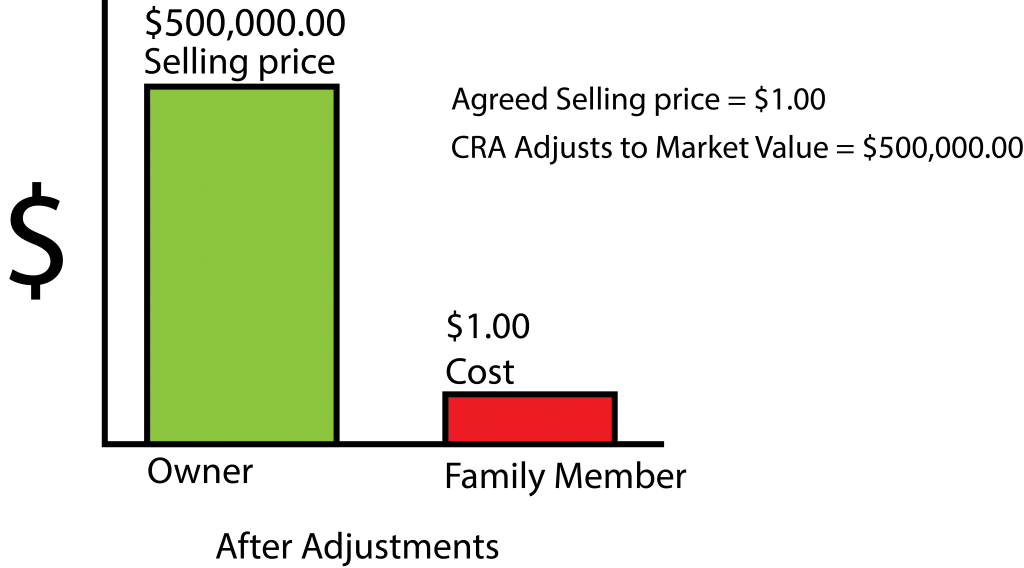

Transferring Business To Family Member In Canada Madan Ca

/ScreenShot2020-02-03at1.41.37PM-322605a2b23a49598d9cdf9faee0a97a.png)

Form 706 United States Estate And Generation Skipping Transfer Tax Return Definition

Cost Basis 101 How To Correctly Understand It

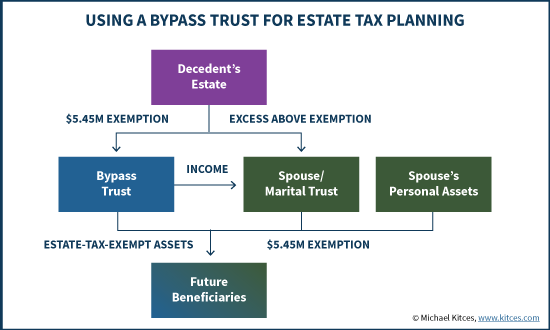

Distributable Net Income Tax Rules For Bypass Trusts

/182667184-56a636213df78cf7728bd987.jpg)

How Is Cost Basis Calculated On An Inherited Asset

The Estate Tax On Stocks And Dividends Intelligent Income By Simply Safe Dividends

/dotdash_Final_Trust_Aug_2020-01-6b0686cb892a40589605baeeef79a183.jpg)