Transfer Pricing Adjustment

Tahapan Pemeriksaan Transfer Pricing Accounting

Transfer Pricing F5 Performance Management Acca Qualification Students Acca Global

What Is Transfer Pricing A Clear And Simple Definition

Transfer Pricing Methods Royaltyrange

%20Application%20of%20three-step%20approach%20to%20apply%20arm's%20length%20principle.JPG)

Iras Introduction To Transfer Pricing

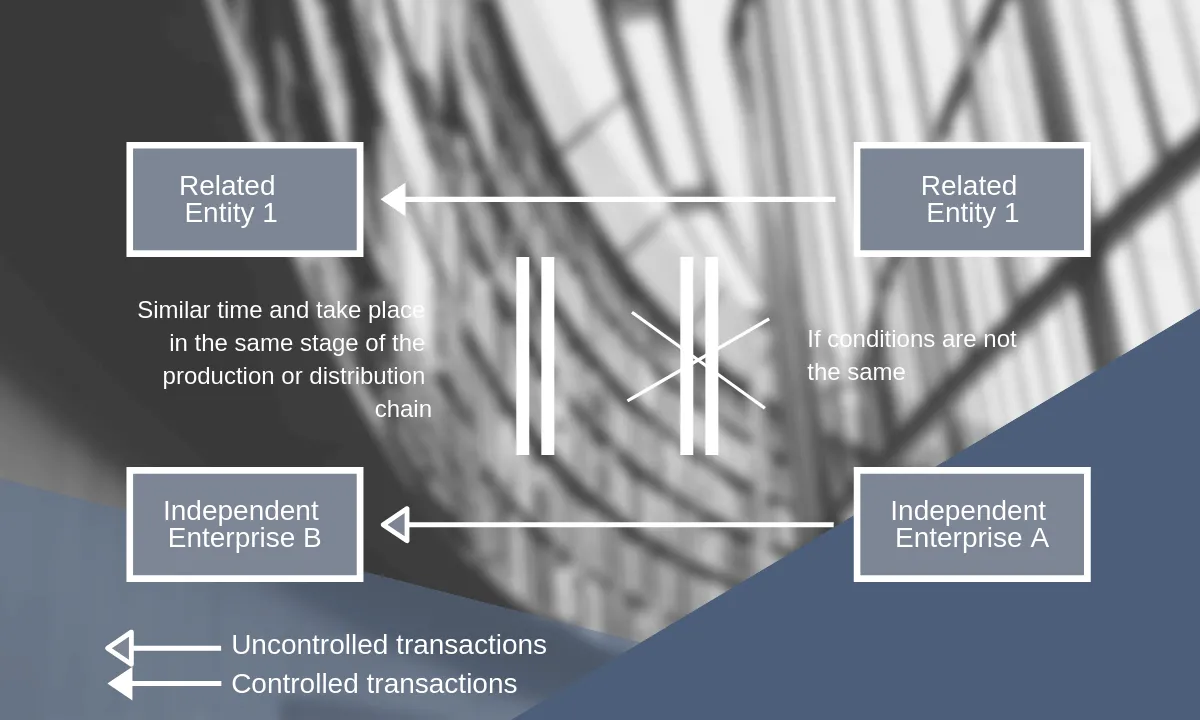

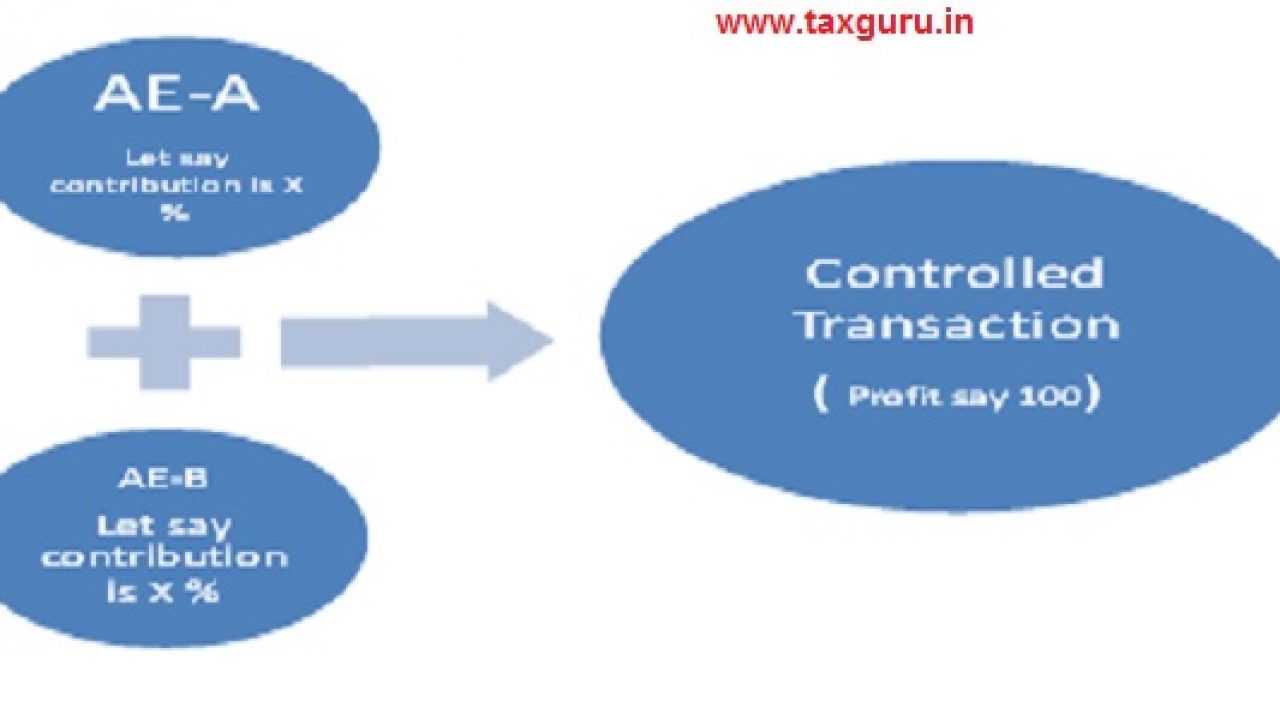

Transfer Pricing

482 transfer pricing adjustment exceeds the relevant dollar thresholds.

Transfer pricing adjustment. The taxpayer also needs to take care of the appropriate recognition of tax consequences of the transfer pricing adjustments from CIT and VAT perspective. Transfer pricing adjustments profitability adjustments are applied by multinationals and groups of companies to adjust the transfer prices in transactions between related entities so that they are at arms length level. Data and research on transfer pricing eg.

1262016 transfer pricing documentation for transaction with related entities for the year that the transfer pricing adjustment is conducted in. In the current high-tariff environmentie with tariffs as high as 25 on many imported goodsthe customs duty cost implications can be significant. As March 31 draws near entities closing their books must make Covid-19 related adjustments to determine transfer pricing margins.

The UK legislation allows only for a transfer pricing adjustment to increase taxable profits or reduce a tax loss. 992019 Transfer pricing is an accounting and taxation practice that allows for pricing transactions internally within businesses and between subsidiaries that operate under common control or ownership. Transfer pricing is in the cross hairs of tax policy as it relates to the competing objectives of three parties.

6662 e that may be imposed in the event of a substantial or gross valuation misstatement. 1282020 Transfer pricing adjustments Generally at the year-end closing of its accounts a company may make transfer pricing TP adjustments to arrive at the arms length outcome. This exercise may indicate that the company has understated or overstated the value of the supply or import of goods or services for GST purposes.

1212020 When transfer pricing adjustments are typically needed including certain regulatory and contractual requirements Practical considerations that MNCs should consider when making year-end adjustments including factors such as the timing and size of the adjustment. 3112021 There are three types of penalties described in Internal Revenue Code IRC. 4272018 Hence transfer pricing adjustments should not necessarily result in a price adjustment for VAT purposes even though the profit adjustment may be an indirect consequence of goods being bought or sold and other kinds of costs being incurred.

11202020 Transfer pricing refers to prices that a multinational company or group charges a second party operating in a different tax jurisdiction for. It is not possible to decrease profits or increase a tax loss. Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations transfer pricing country profiles business profit taxation intangibles This 2017 edition of the OECD Transfer Pricing Guidelines incorporates the substantial revisions made in 2016 to reflect the clarifications and revisions agreed in the 2015 BEPS Reports.

Https Www Longdom Org Articles Determination Of The Arms Length Profitability For Commissionaires Use Of Working Capital Adjustments Pdf

Transfer Pricing Methods Royaltyrange

Contents Introduction To Transfer Pricing Ppt Download

Https Www Longdom Org Articles Determination Of The Arms Length Profitability For Commissionaires Use Of Working Capital Adjustments Pdf

Https Www Un Org Development Desa Financing Sites Www Un Org Development Desa Financing Files 2020 10 Crp40 20transfer 20pricing 20manual 20combined 20compressed Pdf

Pdf Transfer Pricing Application And Advance Pricing Agreements Turkish Application

Best Practices For Year End Transfer Pricing Adjustments In China China Briefing News

Ini Dia Transfer Pricing Penghambat Kenaikan Rasio Pajak Direktorat Jenderal Pajak

Contents Introduction To Transfer Pricing Ppt Download

Contents Introduction To Transfer Pricing Ppt Download

Contents Introduction To Transfer Pricing Ppt Download

Transfer Pricing Study A Simplified Overview

Pdf Transfer Pricing And State Aid The Unintended Consequences Of Advance Pricing Agreements