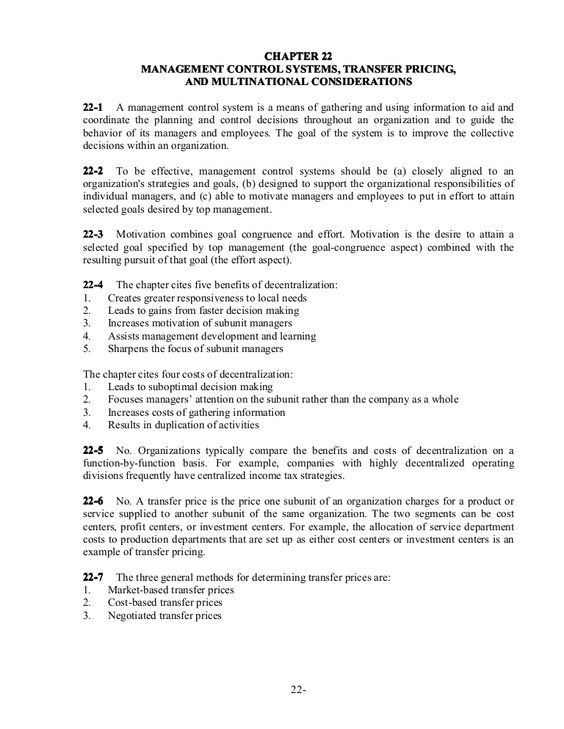

Transfer Pricing Between Related Companies

Transfer Price Meaning Importance Example And More In 2021 Transfer Pricing Website Development Process Financial Management

How Transfer Pricing Works The Business World Is Becoming Increasingly Global And Multinational Companies Are The Norm Today In Fact Large Multinational Cor

Transfer Pricing Determining The Price Charged For Goods And Services Exchanged Between Related Entities I Transfer Pricing Goods And Services Atlantic Ocean

What Will Your Country By Country Report Say About Your Transfer Pricing Policies Better To Know Now Transfer Pricing Country Report Business Practices

Pin By Ey Global On Ey Infographics Tax Guide Indirect Tax Tax

Tp Week Infographic Preparation Transfer Pricing

1292019 Transfer pricing refers to the prices of goods and services that are exchanged between companies under common control.

Transfer pricing between related companies. Entities under common control refer to those that are. In the year of the intercompany depreciable asset transfer the preceding consolidation entries TA and ED are applicable regardless of whether the transfer was upstream or. The divisionalised companies should first determine their goals and priorities before selecting a transfer pricing.

Transfer pricingarms-length charges between related parties such as a parent corporation and a controlled foreign corporationis an area of high-tax-compliance risk for multinational corporations and carries important implications for tax planning and financial reporting. The arms length principle should be adopted for transfer pricing between related parties. Transfer pricing is the pricing of goods services and intangibles between related parties.

IRBM TRANSFER PRICING GUIDELINES 2012 Page 1 of 98 PART I PRELIMINARY 1. When a multi-entity company has different branches one branch may provide products goods or services to another. For example if a subsidiary company sells goods or renders services to its holding company or a sister company the price charged is referred to as the transfer price.

Multinational enterprises often use Transfer Pricing as a method to allocate profits into territories where tax rates are more favourable. 992019 Transfer pricing is an accounting and taxation practice that allows for pricing transactions internally within businesses and between subsidiaries that operate under common control or ownership. Related-Party Transaction To which types of transactions do US.

Reduce depreciation for the year from 9000 to 6000 the appropriate expense based on historical cost. 10152016 Transfer pricing is the setting of the price for goods and services sold between controlled or related legal entities within an enterprise. INTRODUCTION Transfer pricing generally refers to intercompany pricing arrangements for the transfer of goods services and intangibles between associated persons.

Transfer pricing is the pricing of goods services and intangibles between related parties. Therefore the transfer pricing methods selected by a particular business enterprise must reflect the requirements and characteristics of that enterprise and must ultimately be judged by the decision making behaviour that it motivates. The UKs transfer pricing legislation also applies to transactions between any connected UK entities.

Transfer Pricing Transfer Pricing Transfer Quick News

Pricing Agreement Letter Fresh 10 Transfer Pricing Agreement Template Yetra Transfer Pricing Lettering List Of Jobs

Management Control Systems Transfer Pricing And Multinational Considerations By Virtual Pdf Resource Via Slideshare Transfer Pricing Control System Management

Companies Agree That Tax Risk And Controversy Will Become More Important In The Next Two Years Our Ey Tax Risk Survey Says Tax Surveys Insight

Does Entering Into Or Operating In An Emerging Market Significantly Increase A Company S Level Of Tax Risk And Controversy Risk Market Risk Tax Infographic

Pricing Agreement Letter Awesome Transfer Pricing Practical Manual For Developing Transfer Pricing Lettering Agreement

Pin De Ey Global En Ey Infographics

Employment Pass Holders Can Take Up Secondary Directorship When An Eligible Company Appoints From Another Singapore Business Singapore Private Limited Company

Pin By Ey Global On Ey Infographics Tax Guide Indirect Tax Transfer Pricing

Pin On Doing Business In Singapore

Tax Consultancy Domestic Transfer Pricing Firm In Delhi Ncr Transfer Pricing Anti Discrimination Certified Accountant

Pin On Corporate Solutions

Pin By Ey Global On Ey Infographics Tax Guide Tax Transfer Pricing