Transfer Pricing Cost Plus Method

The Cost Plus Method With Example Transfer Pricing Asia

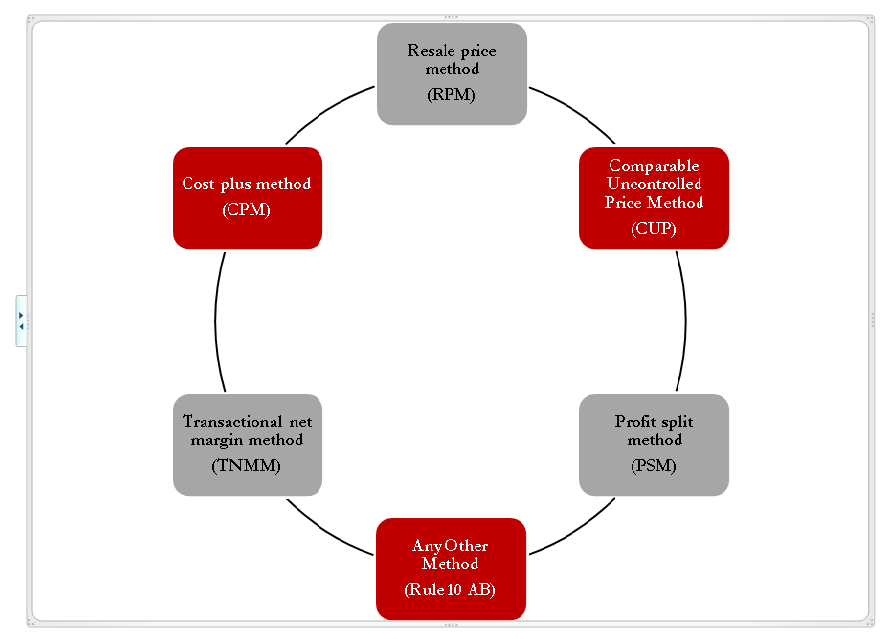

The Five Transfer Pricing Methods Explained With Examples

The Transactional Net Margin Method Explained With Example

Dasar Dasar Transfer Pricing Solusi Pajak

Transfer Pricing Methods

Transfer Pricing Meaning Examples Objectives Purpose

OECD Transfer Pricing Guidelines 2017 membagi metode transfer pricing ke dalam 2 metode yaitu.

Transfer pricing cost plus method. The full cost or cost plus is likely to be treated by the buying division as an input variable cost so that external selling price decisions if based on cost may not be set at levels which are optimal as far as the firm as a whole is concerned. 7312012 Full Cost Transfer Pricing In this method the transfers are made at full costs plus a profit markup. 1Metode Perbandingan Harga antara Pihak yang tidak.

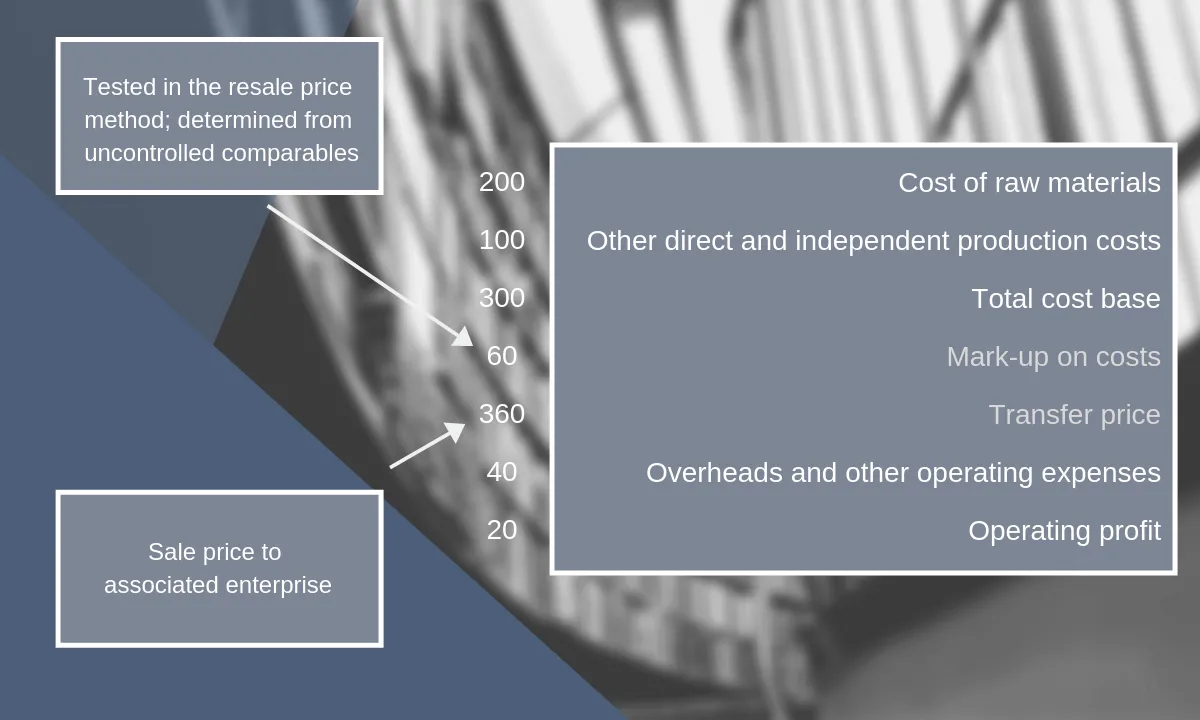

Thus TP COGSx 1 M. Transactional profit methode yaitu transactional net margin methode TNMM dan transactional profit split method PSM. Transfer pricing methods are ways of establishing arms length prices or profits from transactions between associated enterprises.

The Cost Plus Method is a traditional transaction methodThe Cost Plus Method compares gross profits to the cost of sales. 6242020 Thus if we formulate the transfer price under Cost Plus Method it would be equal to COGS Markupwhere Markup is arrived by COGS x Markup. Dalam metode ini penjual atau produsen menetapkan harga jual untuk satu unit barang yang besarnya sama dengan jumlah.

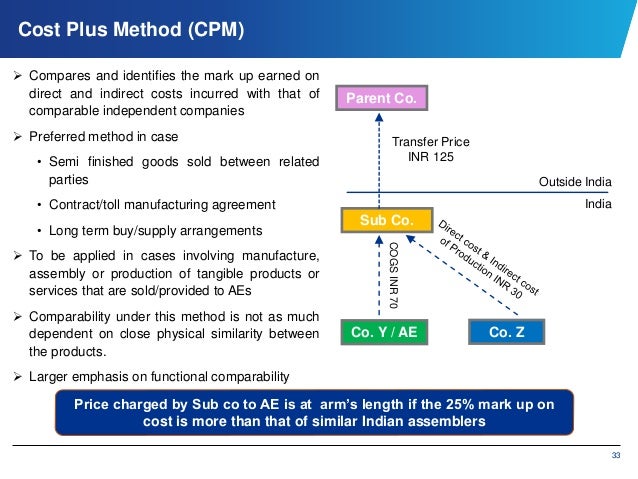

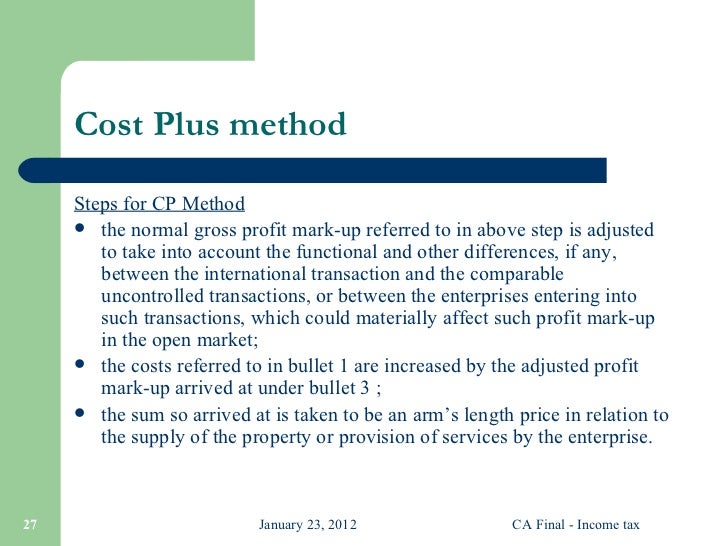

The application of transfer pricing methods. Cost plus method OECD Transfer Pricing Guidelines 2017 Part II Traditional transaction method Chapter II paragraph 256 The costs that may be considered in applying the cost plus method are. Firstly you determine the costs incurred by the supplier in a controlled transaction.

Traditional profit methode yaitu metode Comparable Uncontrolled Price CUP resale price method RPM dan cost plus methode CPM. Final and temporary transfer pricing services. An appropriate cost plus mark up is added to this cost to make an appropriate profit in light of the functions performed taking into account assets used and risks assumed and the market conditions.

8272020 The cost plus method is a transfer pricing method using the costs incurred by the supplier of property or services in a controlled transaction. To ensure a smooth tax audit use of the cost plus method by multinationals and group companies to determine the sales price of a product or service between associated parties needs regular review writes Marie-Lise Swinne of Tax Consult. In such cases the price charged to unrelated parties for those services can be used to value the same services when they are provided to related parties.

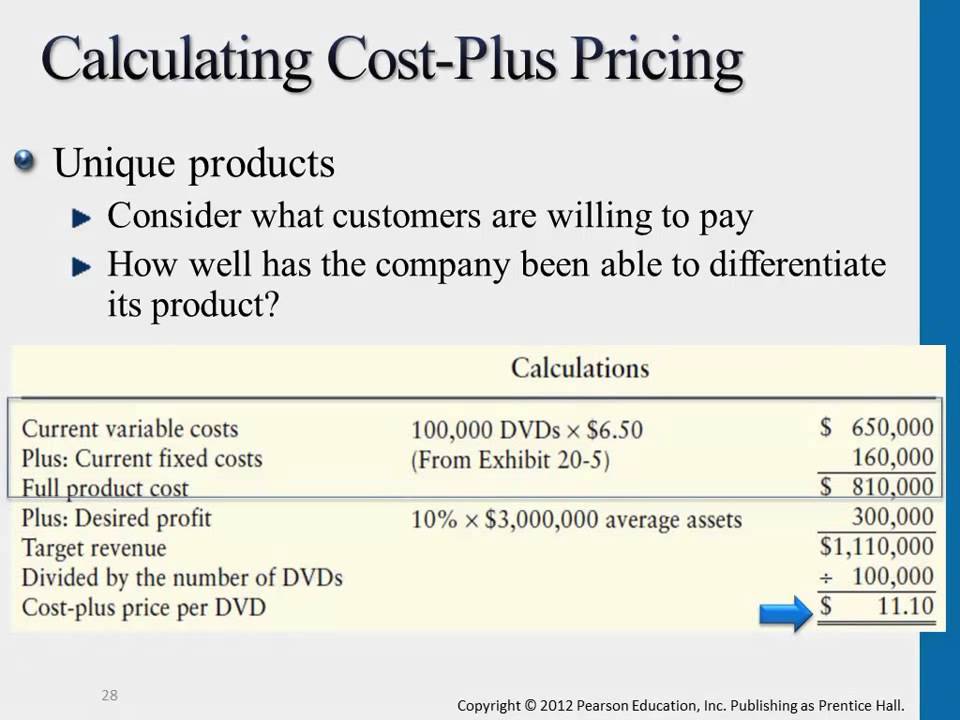

Calculating Cost Plus Pricing Youtube

International And Domestic Transfer Pricing Final

Dasar Dasar Transfer Pricing Solusi Pajak

Transfer Pricing

Transfer Pricing Basics

The Transactional Net Margin Method Explained With Example

Cost Plus Pricing Definition Method Formula Examples Video Lesson Transcript Study Com

Transfer Pricing F5 Performance Management Acca Qualification Students Acca Global

Concept Of Transfer Pricing Transfer Pricing Documentation Ppt Video Online Download

Dasar Dasar Transfer Pricing Solusi Pajak

Concept Of Transfer Pricing Transfer Pricing Documentation Ppt Video Online Download

Dasar Dasar Transfer Pricing Solusi Pajak

Dasar Dasar Transfer Pricing Solusi Pajak