Transfer Pricing Documentation Requirements Us

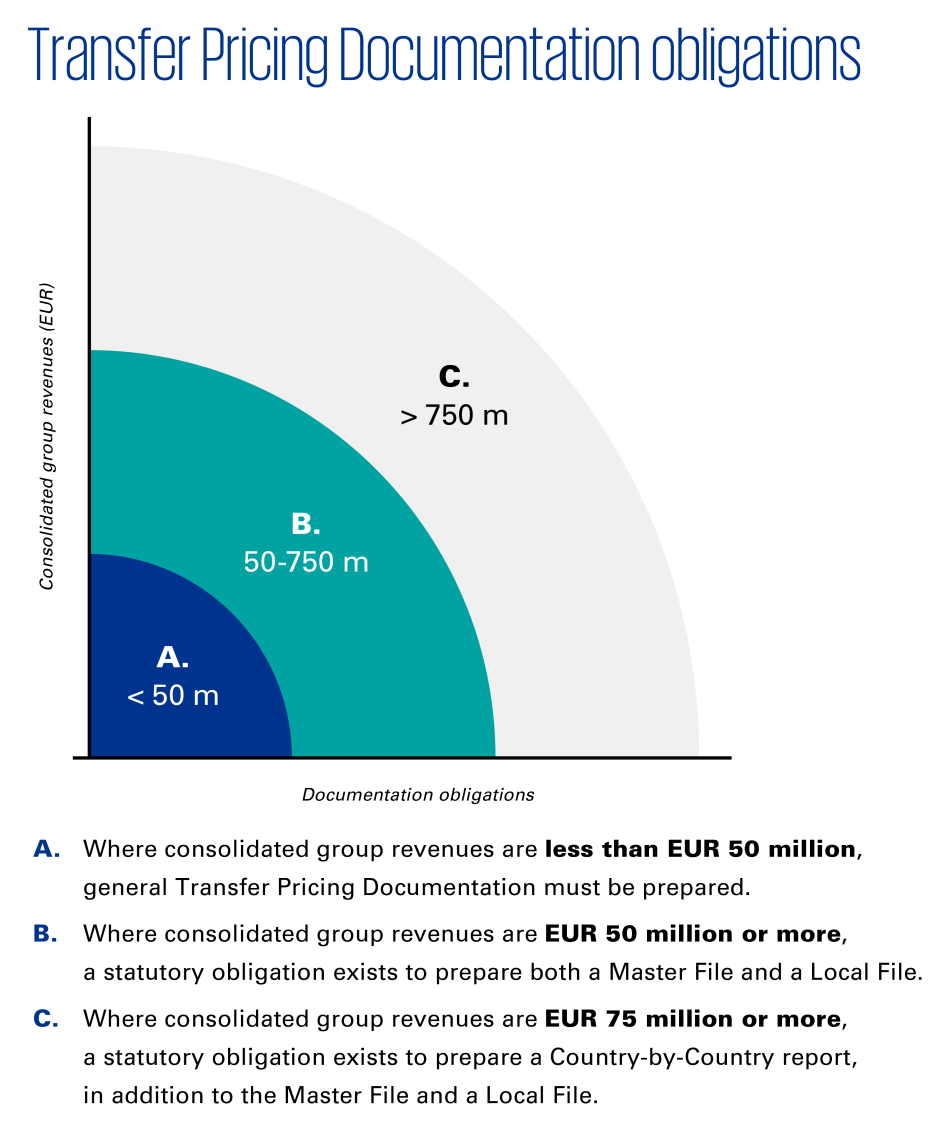

Transfer Pricing Documentation Obligatory Meijburg Co

Beps Royaltyrange

Transfer Pricing Methods Royaltyrange

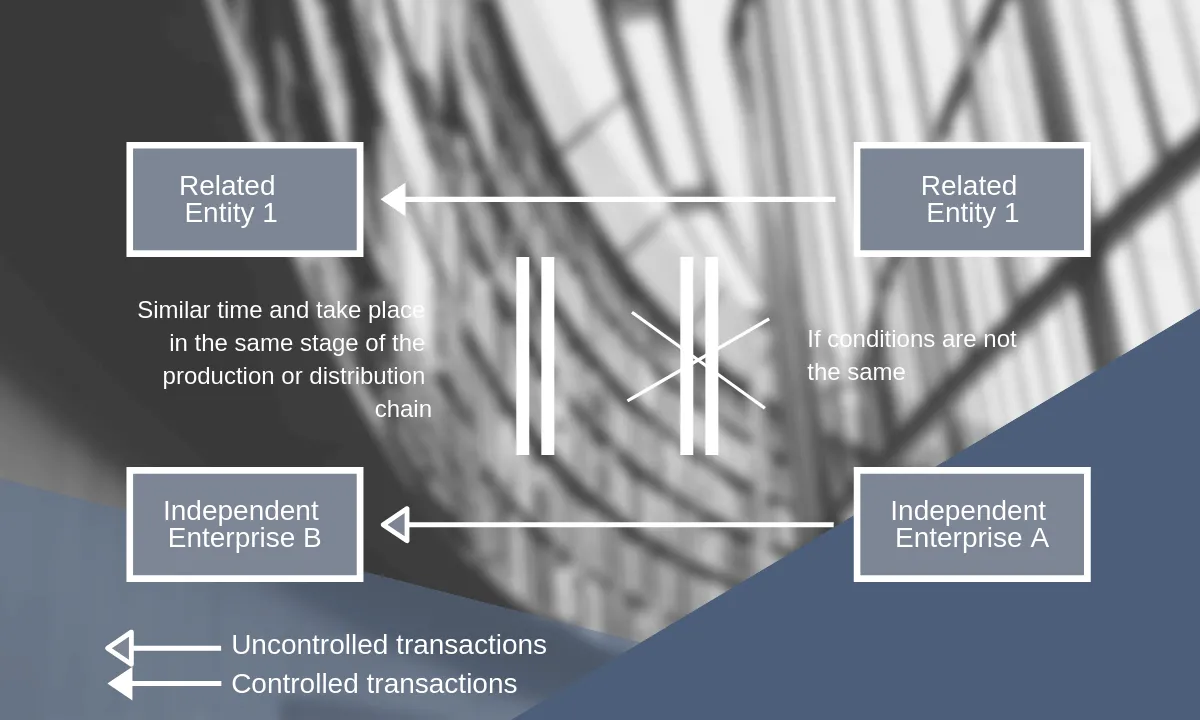

Transfer Pricing Comparable Uncontrolled Price Cup Method Royaltyrange

Pdf Transfer Pricing Application And Advance Pricing Agreements Turkish Application

Transfer Pricing Methods Royaltyrange

The EY Worldwide Transfer Pricing Reference Guide 201920 is a publication designed to help international tax executives identify transfer pricing rules practices and approaches.

Transfer pricing documentation requirements us. Additionally the transfer pricing penalty provisions are triggered when among other things a taxpayer fails to comply with requirements to contemporaneously document that its transfer pricing was on an arms-length basis and fails to timely provide the Internal Revenue Service with this documentation. Thereafter notification is required only if there are any changes in the notification content. Instead contemporaneous transfer pricing documentation is prepared to.

Taxpayers are required to keep records to prove that their related party transactions are always conducted at arms length. Transfer Pricing Documentation Multinationals of all sizes are required to be much more transparent about their allocation of global profits. 1052015 Deloittes Transfer Pricing practice has prepared the Global Tax Reset - Transfer Pricing Documentation Summary.

These must be understood for a company to carry out both transfer pricing compliance and planning activities in the base erosion and profit shifting BEPS1 era. Industry and company analysis sections of the report should be clear and provide context for related-party transactions. Taxpayers with controlled transactions are required to maintain transfer pricing documentation as covered in Section 6662 in order to avoid the imposition of penalties in the event of an adjustment to taxable income by the Internal Revenue Service.

Under the US transfer pricing rules there. Non-US tax authorities and practitioners alike have tended to be critical of the level of. For reporting years up to 2019 Cyprus transfer pricing documentation requirements are limited to intercompany loans financed by debt.

Yes for certain transactions. Having contemporaneous transfer pricing documentation that satisfies the requirements under Section 6662 e in place at the time the tax return is filed can help provide protection against these. 172019 In the United States contemporaneous transfer pricing documentation is prepared to avoid the imposition of penalties after a transfer pricing adjustment proposed by the IRS is.

The guidance is designed to encourage and help taxpayers to prepare improved documentation with an aim to decrease the number of issues selected for examination. When a transfer pricing study is prepared should its content follow Chapter V of the Organisation for Economic Co-operation and Development OECD Guidelines. 6662 e help demonstrate low levels of compliance risk and in turn help support early deselection of the transfer pricing issue from further examination.

Https Wts Com Wts Com Insights Tp Documentation Country Sheets Wts Country Tp Guide Ecuador Pdf

Pdf Transfer Pricing Rules In Eu Member States

Dasar Dasar Transfer Pricing Solusi Pajak

Https Www Pwc Com Gx En Tax Newsletters Pricing Knowledge Network Assets Pwc Tp Puerto Rico Tp Study Relief Pdf

Dasar Dasar Transfer Pricing Solusi Pajak

Transfer Pricing Research Papers Academia Edu

Home Page Tp Tuned

%20Application%20of%20three-step%20approach%20to%20apply%20arm's%20length%20principle.JPG)

Iras Introduction To Transfer Pricing

Https Www Pwc Com Ge En Assets Pdf Transfer Pricing In Georgia Pdf

Dasar Dasar Transfer Pricing Solusi Pajak

International Taxation

The Comparable Uncontrolled Price Cup Method How It Works

Transfer Pricing Research Papers Academia Edu