Transfer Pricing Formula

Transfer Pricing F5 Performance Management Acca Qualification Students Acca Global

The Cost Plus Method With Example Transfer Pricing Asia

The Five Transfer Pricing Methods Explained With Examples

Transfer Pricing Definition Optimal Price Determination Examples

Chapter 8 Pricing Study Objectives Ppt Video Online Download

Managerial Accounting The Importance Of Transfer Pricing Dummies

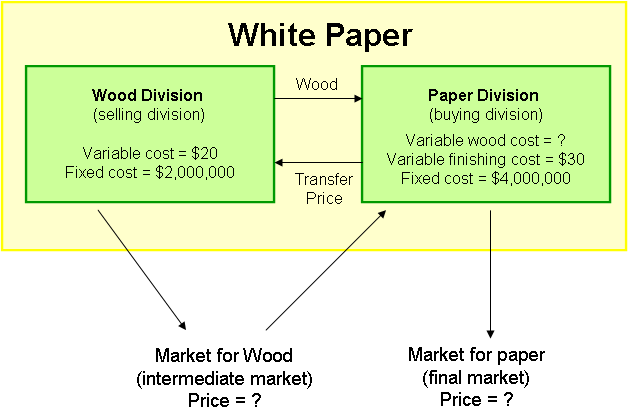

Maximum fixed by receiving division Transfer price the lower of net marginal revenue of transfer-in division and the external purchase price.

Transfer pricing formula. 1292019 Multinational corporations use transfer pricing as a method of allocating profits earnings before interest and taxes EBITDA EBITDA or Earnings Before Interest Tax Depreciation Amortization is a companys profits before any of these net deductions are made. Transfer Pricing introduced from AY 2002 -03 for international transactions Extended to Specified Domestic Transactions SDT from AY 2013- 14 Sections 92 to 92F amended to include reference to SDT However similar amendments to Rules 10 to 10E yet to be carried out Methodology to compute ALP is primarily provided in Rules. The total transfer price is 15 multiplied by 100 or 1500.

A transfer price set equal to the variable cost of the transferring division produces very good economic decisions. Anderson and Sollenberger have presented their evaluation of different transfer pricing approaches as displayed Exhibit 121. 992019 Transfer pricing is an accounting and taxation practice that allows for pricing transactions internally within businesses and between subsidiaries that operate under common control or ownership.

Xiii 105 halaman 1 tabel 9 gambar 2 grafik 34 referensi 1993-2011 9 lampiran. Transfer pricing methods are ways of establishing arms length prices or profits from transactions between associated enterprises. Length nature of prices or profits.

Therefore the transfer pricing methods selected by a particular business enterprise must reflect the requirements and characteristics of that enterprise and must ultimately be judged by the decision making behaviour that it motivates. Base a transfer pricing m ethod subject of course to the presence of other controlled transactions within operating expenses such as management service charges or royalties. 772020 A company may calculate the minimum acceptable transfer price as equal to the variable costs or equal to the variable costs plus a calculated opportunity cost.

How The Cost Plus Transfer Pricing Method Works. Kaplan and Atkinson have given the following recommendations in choosing a transfer. We saw that the total cost of the services is 125000 USD.

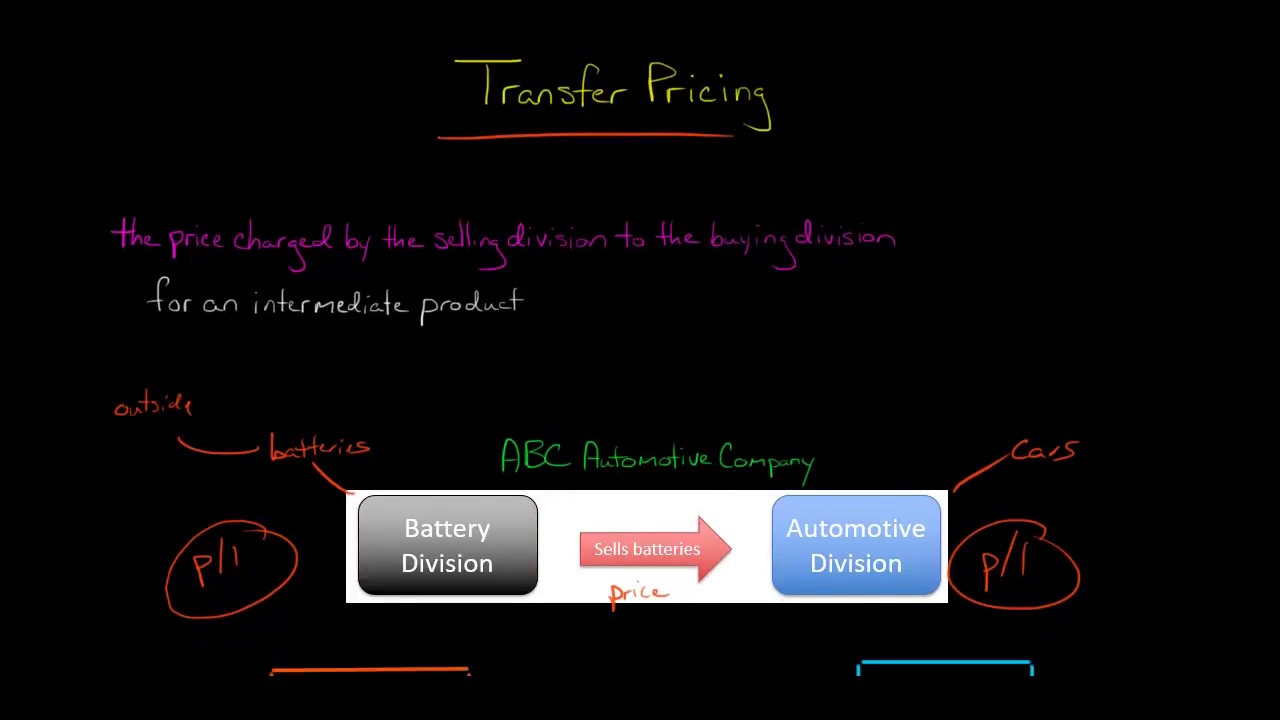

The Berry ratio can also be useful when applied to limited risk distribution of high volume low margin. 2232017 Transfer pricing is how companies specify the value of goods moved between departments or divisions. Transfer price marginal cost of transfer-out division any lost contribution.

Transfer Pricing Acca Advanced Performance Management Apm Youtube

Transfer Pricing

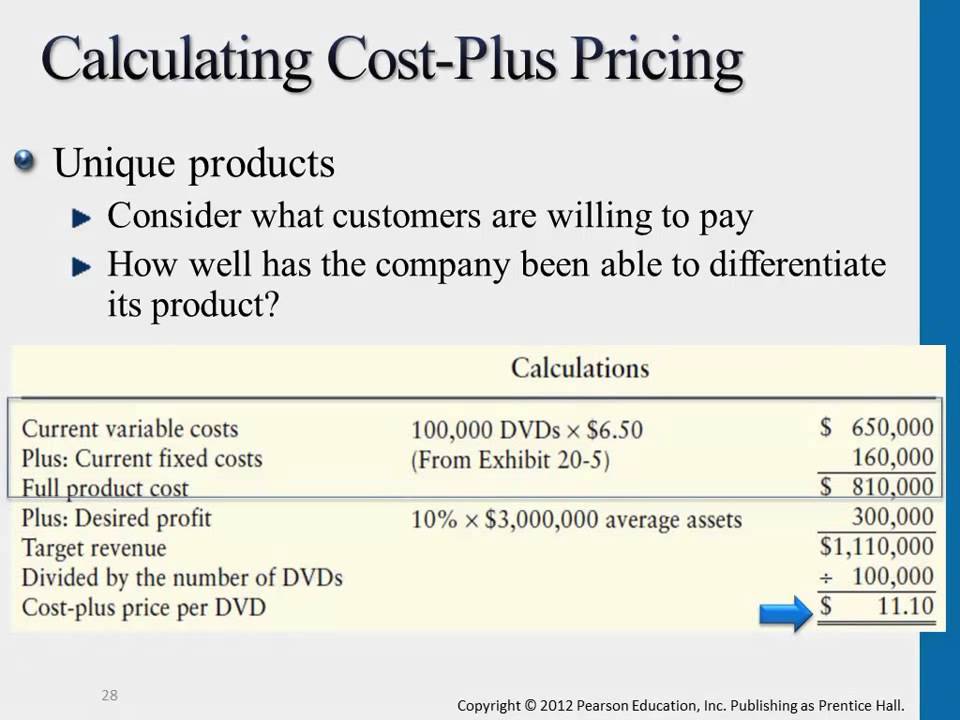

Calculating Cost Plus Pricing Youtube

The Five Transfer Pricing Methods Explained With Examples

Managerial Accounting Ppt Download

How To Negotiate A Transfer Price Dummies

Transfer Pricing Methods Allowed In The Netherlands

Transfer Pricing Youtube

8 Pricing Learning Objectives Ppt Video Online Download

Ch08

J 1 J 2 J Pricing Accounting Fifth Edition J 3 After Studying This Chapter You Should Be Able To 1 1 Compute A Target Cost When The Market Determines Ppt Download

The Five Transfer Pricing Methods Explained With Examples

Transfer Pricing Purpose Methodologies