Transfer Pricing No Excess Capacity

Transfer Pricing No Excess Capacity Youtube

Excess Capacity An Overview Sciencedirect Topics

Managerial Accounting Ppt Download

8 Pricing Learning Objectives Ppt Video Online Download

Chapter 8 Pricing Study Objectives Ppt Video Online Download

Chapter 8 Pricing Study Objectives Ppt Video Online Download

If excess capacity exists market price is a good transfer price.

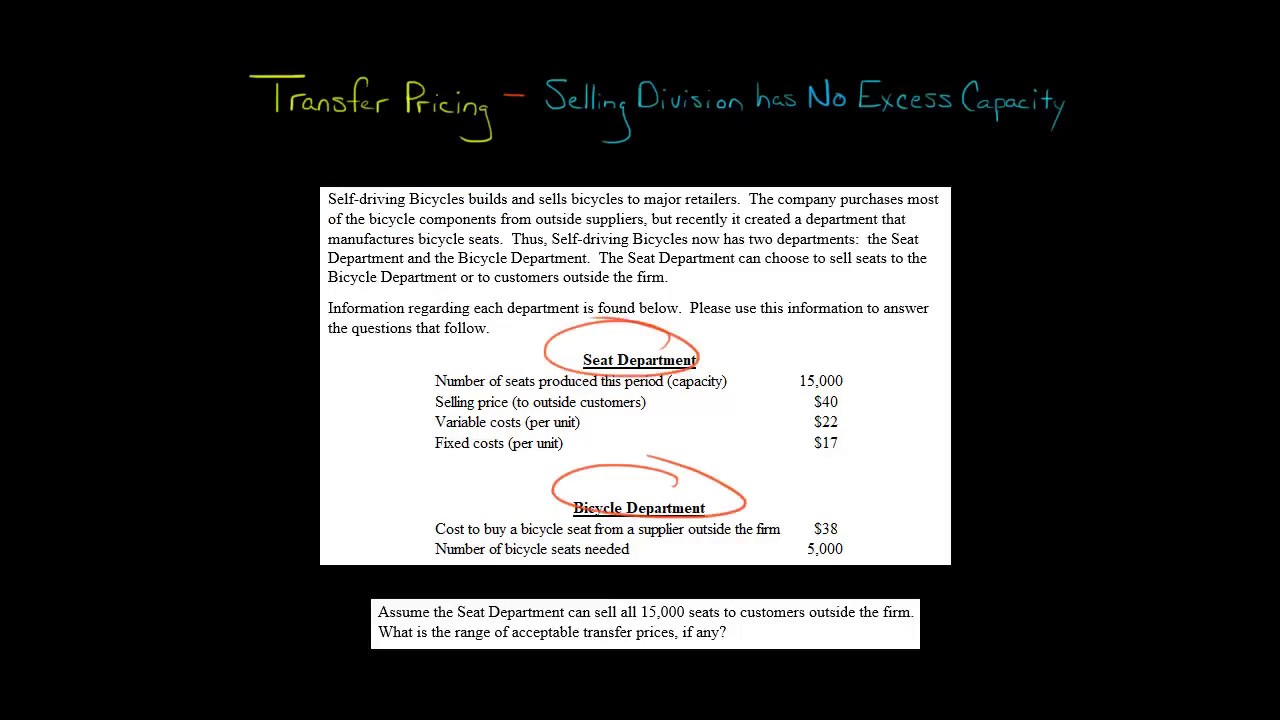

Transfer pricing no excess capacity. So the transfer price will be no lower than variable cost and no. Briefly define the term opportunity cost. 11192020 A company with a lot of excess capacity can lose sizable amounts of money if the business cannot pay for the high fixed costs that are associated with production.

However in Scenario 2 where spare capacity exists it is clear that the full cost transfer price of 83 per ton would lead to optimal decision-making in these circumstances and in fact would split the incremental profit reasonably equitably. When the selling division does not have excess capacity this. Transfer price incremental outlay costsunit to point of transfer opportunity costunit to the supply division.

1252018 This video discusses transfer pricing when the selling division does not have excess capacity. If excess capacity transfer price standard variable costs. On the other hand excess.

Usually no cash actually changes hands between the segments. One element of the general transfer-pricing rule is opportunity cost. A common approach is to set the transfer price equal to the price in the external market and when there is no excess production capacity and perfect competition prevail the general transfer pricing rule and the external price yield the same transfer price.

Transfer price Scenario 4 there is no external market and there is excess capacity in the supplying division - As there is no opportunity cost with the transfer the transfer is based on cost-plus mark-up Scenario 5 there is no external market and no excess capacity in the supplying division - The transfer price will need to account for the opportunity cost on lost sales. 1152012 If we consider Scenario 1 it is clear that the full cost transfer price 83 per ton would be too low where no spare capacity exists. A transfer price is an artificial price used when goods or services are transferred from one segment to another segment within the same company.

Liululliwhen the production division has no excess capacity and perfect competition prevails the general transfer price rule and external market price will yield the same transfer price. 272009 ullia common approach is to set the transfer price equal to the price in the external market. Liululliif the producting division has excess capacity and perfect competition does not prevail then the two methods will given different transfer.

Chapter 8 Pricing Study Objectives Ppt Video Online Download

Transfer Pricing

Chapter 10 Decentralization Responsibility Accounting Ppt Video Online Download

Excess Capacity An Overview Sciencedirect Topics

According To The Shanghai Metals Market The A00 Aluminium Ingot Price Has Extended Its Decline By Rmb 30 Per Tonne To Stan Ingot Chinese New Year Holiday Price

How To Negotiate A Transfer Price Dummies

Pin On Business

Chapter 8 Pricing Study Objectives Ppt Video Online Download

Incremental Analysis For Short Term Decision Making Ppt Download

Monopolistic Competition Short Run Profits And Losses And Long Run Equilibrium

Excess Capacity An Overview Sciencedirect Topics

China S Excess Capacity Problem

When A Particular Lift With An Overhead Crane Requires Substantial Planning Due To Special Circumstances A Critical Lift Plan May Crane Lift How To Plan Crane