Transfer Pricing Nz

Transfer Pricing Methods Tpguidelines Com

Https Repository Theprakarsa Org Media 285237 G 20 Dan Transparansi Perpajakan Global D2f9e8ee Pdf

Http Www Taxand Com Wp Content Uploads 2019 07 Taxand Asia Junior School 2019 Tp Presentation Updated By Sarah Chew Elvi Final Pdf

Http Www Taxand Com Wp Content Uploads 2019 07 Taxand Asia Junior School 2019 Tp Presentation Updated By Sarah Chew Elvi Final Pdf

Transfer Pricing And The Arm S Length Principle Tpguidelines Com

Restricted Transfer Pricing And The Impact On Interest Deductibility In New Zealand Tax Deloitte New Zealand

KPMG New Zealands Global Transfer Pricing Services GTPS practice helps companies develop and implement economically supportable transfer prices document policies and outcomes and respond to tax authority challenges.

Transfer pricing nz. Transfer pricing is a critical tax issue for businesses operating across more than one jurisdiction. It has become one of the most important international tax issues facing multinational corporations whatever their size. Loveday Consulting is a firm specialising in providing transfer pricing as well as international and corporate tax advice.

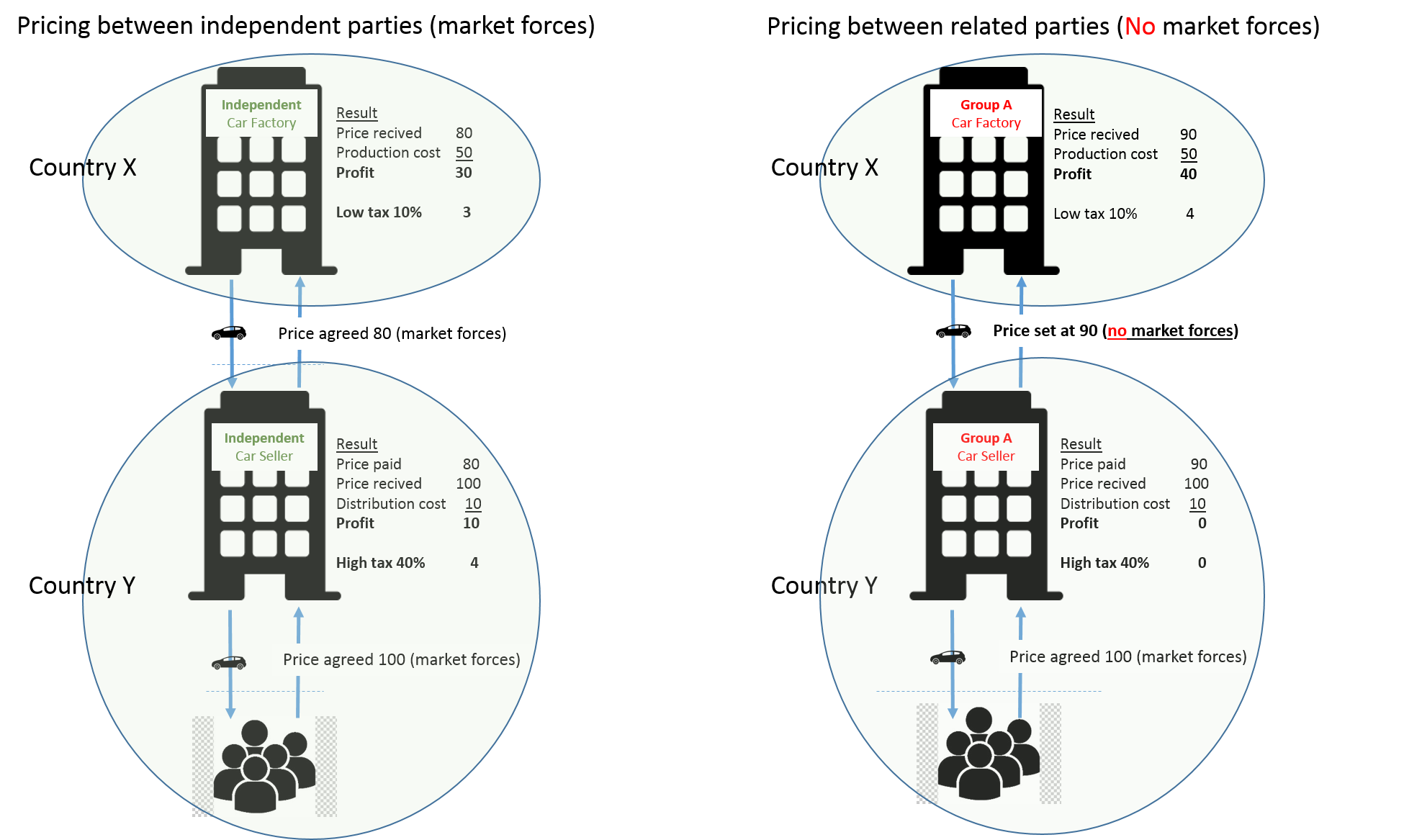

New Zealands transfer pricing rules apply to cross-border arrangements between associated persons based on 50 or greater common shareholding or effective control. In October 2000 the New Zealand Inland Revenue also released transfer pricing guidelines. No court cases have arisen directly under New Zealands current transfer pricing legislation or under the previous legislation which was section GD 13 of the Income Tax Act 1994.

MNEs are a significant force in New Zealands economic environment. Foreign trusts with New Zealand resident trustees Learn about the requirements for registering and de-registering a New Zealand foreign trust and the process for annual returns. Section GB 2 can extend the application of sections GC 7-10 to non-associated parties where there is a collateral arrangement such as a market-.

Transfer pricing compliance and documentation Revenue authorities are focusing more widely and intensely on transfer pricing issues. Introduction to New Zealand transfer pricing. Construction and Real Estate BDO New Zealands specialist business advisory service will help you navigate the increasingly complex real estate and construction industries.

Global rules are constantly changing and tax authorities are not aligned as they implement changes over different timelines. Where an abusive tax position is perceived cases have been heard under the GAAR. Restricted transfer pricing requires taxpayers with NZD10 million or more in cross-border related borrowing to disregard certain loan features for the purpose of pricing the interest rate regardless of whether the threshold for the debt percentage or the 15 tax rate criteria have been breached.

He has considerable experience in transfer pricing matters including assisting establishing transfer pricing framework and policies negotiating APAs and making successful. To date transfer pricing disputes have been settled by negotiation or adjudication. It is the responsibility of local management to ensure a companys transfer prices are in accordance with the arms length standard.

Https Repository Theprakarsa Org Media 285237 G 20 Dan Transparansi Perpajakan Global D2f9e8ee Pdf

Https Www Un Org Development Desa Financing Sites Www Un Org Development Desa Financing Files 2020 05 Crp14 20 20transfer 20pricing 20manual 20combined Pdf

Https Www Un Org Development Desa Financing Sites Www Un Org Development Desa Financing Files 2020 05 Crp14 20 20transfer 20pricing 20manual 20combined Pdf

Microsoft Taxes And Transfer Pricing Tpcases Com

Restricted Transfer Pricing And The Impact On Interest Deductibility In New Zealand Tax Deloitte New Zealand

Transfer Pricing Deloitte Sea Tax

Transfer Pricing Deloitte Tax

Pdf Multinational Transfer Pricing Of Intangible Assets Indonesian Tax Auditors Perspectives

Global Transfer Pricing Principles And Practice Deloitte Uk

What Is Transfer Pricing A Clear And Simple Definition

Join Our Leading Practice As A Transfer Pricing Specialist Deloitte

Transfer Pricing Developments In Debt Pricing Tax Alert September 2018 Deloitte New Zealand

Transfer Pricing Energy And Resources 5th Edition