Transfer Pricing Requirements

%20Application%20of%20three-step%20approach%20to%20apply%20arm's%20length%20principle.JPG)

Iras Introduction To Transfer Pricing

International Transfer Pricing Searching For Patterns Sciencedirect

Transfer Pricing Purpose Methodologies

What Is Domestic Transfer Pricing

Transfer Pricing Purpose Methodologies

Uae May Issue Transfer Pricing Regulations In 2020 Spectrum Accounts

Relevant guidance as well as fulfil all Transfer Pricing Documentation requirements in the Guidelines.

Transfer pricing requirements. Platform for Collaboration on Taxs new toolkit helps countries implement effective transfer pricing documentation requirements 19 January 2021 OECD publishes guidance on the transfer pricing implications of the COVID-19 pandemic 18 December 2020. High-quality transfer pricing documentation allows the. EY has developed TP Web a comprehensive transfer pricing documentation tool that can help you streamline your internal processes and generate reporting packages to support transfer pricing documentation requirements under BEPS Action 13.

6662 e help demonstrate low levels of compliance risk and in turn help support early deselection of the transfer pricing issue from further examination. Such language requirements are not considered in this summary when determining whether an OECD master file and local file can provide local documentation compliance. The annual corporate income tax return must be submitted within 12 months from the end of the relevant year of assessment.

Transfer pricing rules around the globe are quite similar. A 1 Transfer pricing reports that comprehensively document the reasonable selection and application of a transfer pricing method consistent with the requirements of. Taxpayers should prepare and keep contemporaneous transfer pricing documentation to show that their related party transactions are conducted at arms length.

On 23 November 2020 the Italian Tax Authorities issued new instructions New Instructions 1 regarding the content and validity of the elective transfer pricing TP documentation available to Italian resident enterprises and. Practice issues for transfer pricing Find out about common practice issues with transfer pricing. 6172020 With transfer pricing requirements having now been in place for over a year this second edition of transfer pricing guidelines have now been issued providing further clarifications in certain areas such as intangibles and documentation requirements.

Or alternatively may opt to comply with Transfer Pricing Documentation requirements under paragraph 254a d and e only. The new guidance makes it clear that the arms length principle applies in all cases. The UKs transfer pricing legislation details how transactions between connected parties are handled and in common with many other countries is.

Although transfer pricing is sometimes inaccurately presented by commentators as a tax avoidance practice or technique transfer mispricing the term refers to a set of substantive and administrative regulatory requirements imposed by governments on certain taxpayers. At the same time there are different focus areas in specific countries. Transfer pricing is the pricing of goods services and intangibles between related parties.

Transfer Pricing F5 Performance Management Acca Qualification Students Acca Global

Transfer Pricing Its Importance In Domestic And International Transaction

What Will Your Country By Country Report Say About Your Transfer Pricing Policies Better To Know Now Transfer Pricing Country Report Business Practices

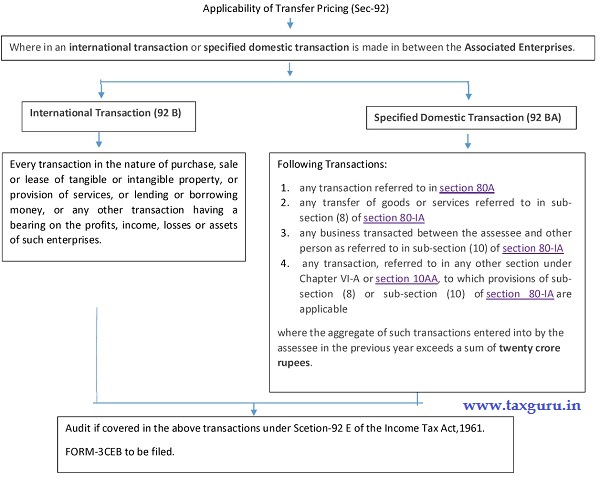

Transfer Pricing Audit Applicability In India

Transfer Pricing Deloitte Tax

Intangibles In The World Of Transfer Pricing Identifying Valuing Implementing Bjorn Heidecke Springer

Transfer Pricing Deloitte Tax

Https Www Pwc Com Sg En Tax Bulletin Assets Taxbulletin201803 Pdf

Https Www Irs Gov Pub Irs Pdf P5300 Pdf

Transfer Pricing Audit Applicability In India

Https Www Pwc Com Pk En Assets Document Flyer 20 20sro 20144 Pdf

Https Www Pwc Com Gx En Tax Newsletters Pricing Knowledge Network Assets Pwc Tp Ethiopia 20issues 20tp 20rules Pdf

Transfer Pricing Deloitte Tax