Transfer Pricing Valuation Methods

Business Valuation Methods Business Valuation Business Management Business

Transfer Pricing And Customs Valuation Book Ibfd

Pin On Epubnewbooks

Cv Design Template Cv Design Template Business Valuation Schools First

Webinar On Valuation Of Intangibles Business Valuation Webinar Marketing Data

Intellectual Property The Complete Guide For Transfer Pricing Valuation Licensing And Litigation Professionals Royaltyrange

The author considers the main features of intangibles in a transfer pricing context as well as the conceivable consequences from a company perspective.

Transfer pricing valuation methods. Transfer pricing methods are ways of establishing arms length prices or profits from transactions between associated enterprises. Economic modelling and the relevance or otherwise of bank opinions. The application of transfer pricing methods.

2192019 Transfer pricing practice generally requires a Functional Analysis often also referred to as a functional and risk analysis an Economic Analysis and a Financial Valuation Analysis. Topics covered include ownership concepts. However if a traditional transaction method and a transactional profit.

Intangibles in a Transfer Pricing Context. The cost of funds incurred by the lender in raising the funds to lend. 5 - WCO Guide to Customs Valuation and Transfer Pricing guidelines based on the arms length principle for the setting and testing of transfer prices for direct tax purposes.

114 TAX ADMINISTRATION REVIEW CIATlAEATlIEF N. 45 CUSTOMS VALUATION AND TRANSFER PRICING DOCUMENTATION the normal pricing practices of the industry in Resale price method RPM. Transaction value of identical or similar goods deductive value computed value and fall-back method.

For the methods of transfer pricing it may be required to take into account the companies market business strategies and the terms of payment which are not required for the methods of the determining of customs value Method of the resale price of transfer pricing and method of customs valuation based on deducted value. The use of credit default swap prices. Transfer Pricing and Customs Valuation A coordinated approach to related party pricing The days of boldly using transfer prices as a basis for customs values are gone.

A transfer price is based on market. These include the comparable uncontrolled price CUP method the resale price method the cost plus method the transactional net margin method and the transactional profit split method. Enforced by revenue authorities transfer pricing is grounded in.

Resurgent India Debt Equity Advisory Tev Training Wealth Debt Equity Business Valuation Equity

Financial Statement Analysis And Valuation 5th Edition的图片 1 Financial Statement Analysis Financial Statement Financial

Are You Interested In Buying Online Jobs Board With Huge Potential Business For Sale Ownersellers Sellingyourb Business Valuation Sell Your Business Business

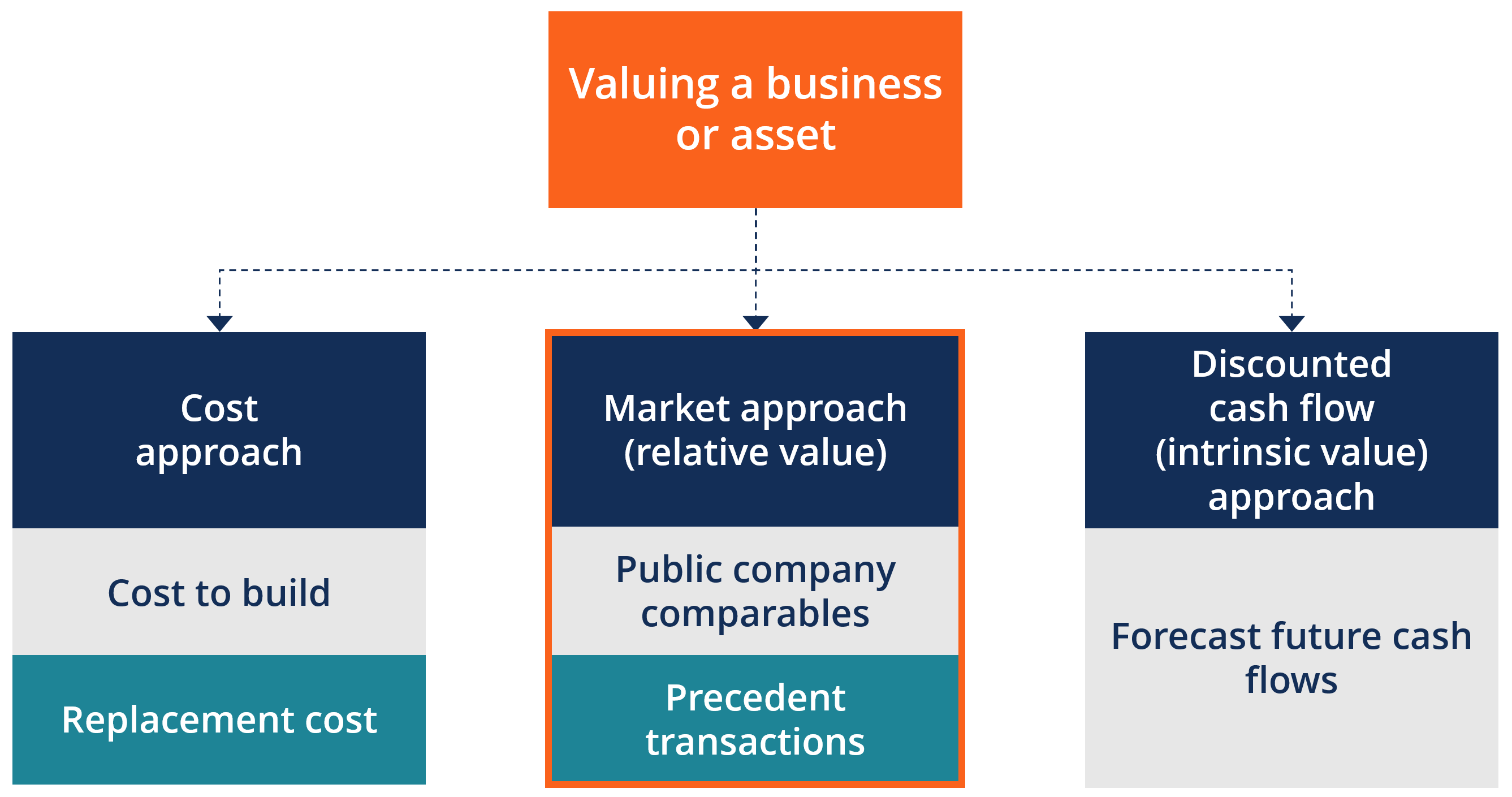

Market Approach Methods Uses Advantages And Disadvantages

Http Www Valerie Eu Images Themes Valuingess Jhassink Pdf

Corporate Logo Request Logo Design Contest Design Logo Contest Rveldhuizen Book Printing Companies Logo Design Contest Corporate Logo

Mbaa 523 Written Assignment 3 Airline Pricing Research Assignment This Or That Questions Case Study Homework

Pin On Business To Business

Download The Management Of Mutual Funds Pdf Free Mutuals Funds Fund Portfolio Management

Mineral Pricing Igf Mining

Lessons In Corporate Finance A Case Studies Approach To Financial Tools Financial Policies And Valuation Finance Finance Lessons Case Study

Real Estate Valuation Process And Its Benefits In Sydney Property Valuation Real Estate Services Audit Services

Pin On Test Bank Solution Manual 2020 2021