Transfer Realty Tax Nj

Https Www Bracheichler Com Wp Content Uploads 2019 12 Gladstone Ecepc Presentation Pdf

Transfer Taxes Paradigm Tax Group

New Jersey Real Estate Transfer Tax Calculator

Real Estate Transfer Taxes Deeds Com

Current Median List Price Of Homes For Sale In Fairfield New Jersey 3 16 14 Via Altos Research Homesforsaleinfairfieldnj La Real Estate Nj Fairfield Timer

Realty Transfer Tax Information Kearny Nj Real Estate Listings And Homes For Sale Home Buying Home Selling Information Rosa Agency

The Fee is required to be paid upon the recording of deeds conveying title to.

Transfer realty tax nj. Class 2 Residential. 4615-5 et seq The Realty Transfer Fee is imposed upon the recording of deeds evidencing transfers of title to real property in the State of New Jersey. 4172020 An Affidavit of Consideration RTF-1 must be filed with any deed in which a full or partial exemption is claimed from the Realty Transfer Fee.

On June 27 2018 the New Jersey State Legislature attempted to double the realty transfer fee. The last big exemption is when a property transfer is exempt from the realty transfer fee. Imposes a realty transfer fee RTF on the seller of real property for recording a deed for the sale.

For example in Michigan state transfer taxes are levied at a rate of 375 for every 500 which translates to an effective tax rate of 075 375 500 075. The RTF is already a burdensome tax on homeowners selling their property and proposing to double this fee is just one more tax property owners should not be responsible for. In that case it is also exempt from the mansion tax.

The Declaration and payment must be submitted to the recording office at the time the deed is presented for recording. 5212018 If you have sold a home or other real estate within the State of New Jersey you have likely paid a fee known as the Realty Transfer Fee. 7242020 Note that transfer tax rates are often described in terms of the amount of tax charged per 500.

Upon the transfer of the deed to the buyers the seller pays the RTF which is based on their propertys sales price. New Jersey Transfer Tax. The fee is based on the sales price of the property and the seller is required to pay the fee at the time of closing.

It should be noted that if a deed is recorded and it is determined later that additional RTF fees are due the deed is still valid and the buyers status as Bona Fide Purchaser is not affected. 8272012 The New Jersey realty transfer tax applies to the sale of residential real estate and is assessed to the seller of the property said Michael Steiner a. The only exception occurs if the property is used as an investment or rental property in which case the seller could deduct them as a work expense.

Closingcosts Expenses Over And Above The Price Of The Property Incurred By Buyers Sellers Home Insurance Quotes Real Estate Buyers Real Estate Marketing

Real Estate Investment Trust Tokyo Realty Investment Management Inc Real Estate Investment Trust Investing Real Estate School

Did You Know A 203 K Loan Can Bundle The Costs Of Fixing Up A Home Into Your Mortgage Home Loans Home Mortgage Home Refinance

Real Estate 101 The Cost Of Transferring A Land Title In The Philippines Philrep Realty Corp

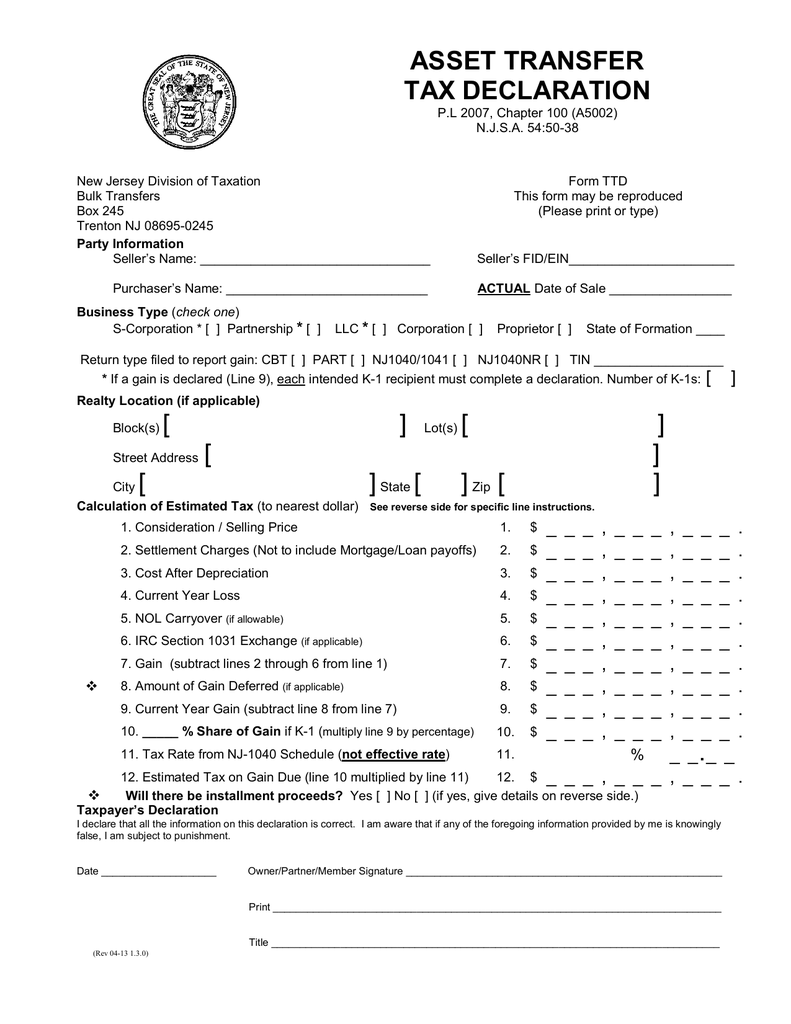

Asset Transfer Tax Declaration

Realty Transfer Fee House And Dollar Balancing Showing Investment Since 1968 Realty Transfer Fees Have Been An Unfortunate Reality In New Jersey Since 1968 The Original Purpose Was Meant To Defray The Cost Of Tracking The Transfer Of Real Properties

Jakarta Kompas Com Pemerintah Provinsi Dki Jakarta Mengusulkan Kenaikan Tarif Pajak Bea Balik Nama Bbn 1 Untuk Kendaraan Baru Menj Pemerintah Sari Tulisan

97 Real Estate Infographics How To Make Your Own Go Viral The Close Real Estate Infographic Real Estate Tips Real Estate Investing

Could You Deduct That Nj Realty Transfer Fee

Http Capemaycountynj Gov Documentcenter View 1939 Deeds Bidid

Https Www Greenbaumlaw Com Media Publication 483 Practical 20law 20ownership 20 20jan 20 20tjd 20ktb 20msk Pdf

Great Information For First Time Home Buyers First Time Home Buyers Real Estate Career First Time

Realestate Yahoo News Latest News Headlines Mortgage Loans Home Equity Loan Home Equity