Transfer Tax Kentucky Statute

Https Apps Legislature Ky Gov Law Statutes Statute Aspx Id 43160

Who Inherits With No Will In Kentucky Inheritance Tax Inheritance Tax

Missouri Quit Claim Deed Form Quites Missouri Form

Kentucky Inheritance Tax Planning And Paying Blog Jenkins Fenstermaker Pllc

About Krs Kentucky Retirement Systems

Kentucky The Official Army Benefits Website

There is imposed a tax at the rate of 100 for the first 100000 or fractional part of 100000 and at the rate of 10 cents for each additional 10000 or fractional part of 10000 on each deed instrument or other writing by which any lands tenements or other realty sold is granted assigned transferred or otherwise conveyed to or vested in the purchaser or purchasers or any.

Transfer tax kentucky statute. 9252020 When ownership in Kentucky is transferred an excise tax of 50 for each 500 of value or fraction thereof is levied on the value of the property. A If any deed evidencing a transfer of title subject to the tax herein imposed is offered for recordation the county clerk shall ascertain and compute the amount of the tax due thereon and shall collect the amount as prerequisite to acceptance of the deed for recordation. Transfer tax is uniform across the state.

B The amount of tax shall be computed on the basis of the value of the transferred property as set forth in the deed. Transfer tax is imposed at fifty cents for each 500 of value as declared in the deed. For example the sale of a 200000 home would require a 200 transfer tax to be paid.

See KRS 142050 7 for exceptions. 11202018 Each state is allowed to determine its own taxes. This tax is also referred to as a deed stamp tax real estate conveyance tax or documentary stamp tax.

Cities in a county that charges the tax can also have a transfer tax at half of the countys rate. C The tax required to be levied by this section shall be collected only once on. 2 A tax upon the grantor named in the deed shall be imposed at the rate of fifty cents 050 for each 500 of value or fraction thereof which value is declared in the deed upon the privilege of transferring title to real property.

Transfer Tax Information These excerpts from Kentucky statutes list the exemptions from transfer tax in detail. KRS 142050 AKA Deed Transfer Tax. The city tax can be credited against the county tax.

If the document is exempt from transfer tax it must be stated on the document. Transfer taxes are imposed by state county and sometimes city governments. 5302018 either 1 a sworn notarized certificate signed by the grantor or his agent and the grantee or his agent that the consideration reflected in the deed is the full consideration paid for the property or 2 a sworn notarized certificate signed by the grantor or his agent and the grantee or his agent stating that the transfer is by gift and setting forth the estimated fair cash value of.

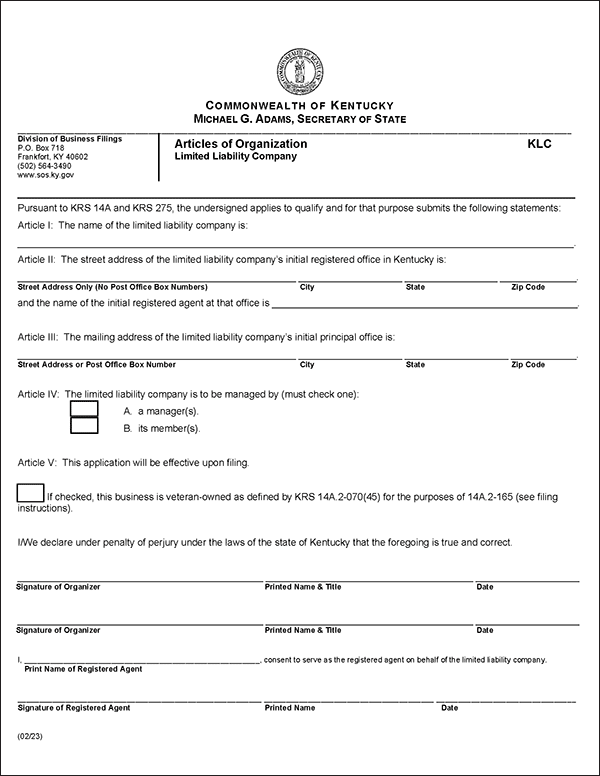

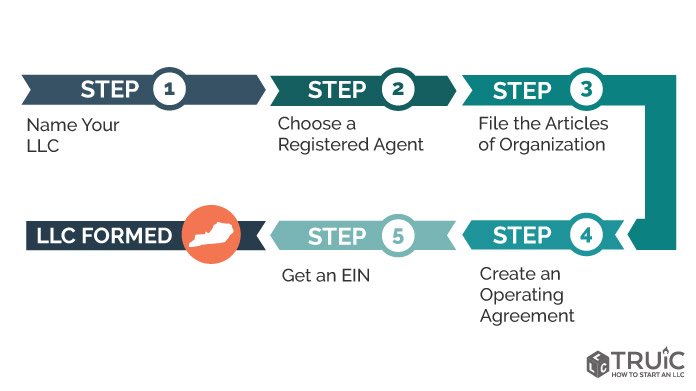

Kentucky Llc How To Start An Llc In Kentucky Truic Guides

Kentucky Releases Guidance On Inventory Tax Credit Bkd Llp

Https Personnel Ky Gov Dhra Employeehandbook Pdf

Kentucky Llc How To Start An Llc In Kentucky Truic Guides

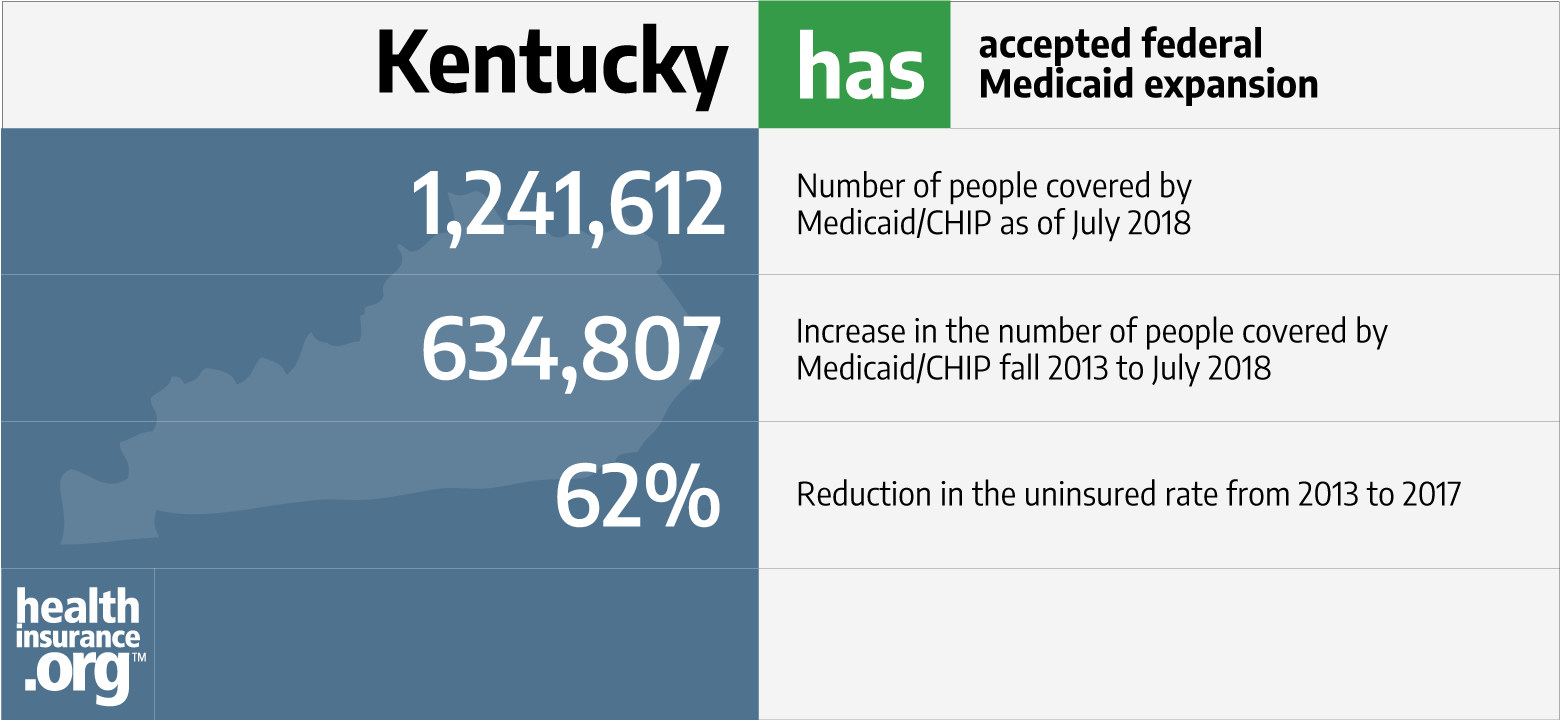

Kentucky And The Aca S Medicaid Expansion Healthinsurance Org

Free Kentucky Estate Planning Checklist Word Pdf Eforms

Guide To The Atv And Utv Laws Of Kentucky Atv Man

Kentucky Self Directed Ira Ira Financial Group

Shelbyville Ky Official Website

Property Tax Department Of Revenue

Kentucky Board Of Examiners Of Psychology

The Ultimate Guide To Getting Divorced In Kentucky Divorce Guide Survive Divorce

E Book Business Law Today The Essentials 8th Edition 8e In 2020 Business Law Paperbacks Goodreads Books