Transfer Pricing Best Method Rule

The Five Transfer Pricing Methods Explained With Examples

The Cost Plus Method With Example Transfer Pricing Asia

Transfer Pricing Meaning Examples Objectives Purpose

The Transactional Net Margin Method Explained With Example

Transfer Pricing Methods Royaltyrange

What Is Transfer Pricing A Clear And Simple Definition

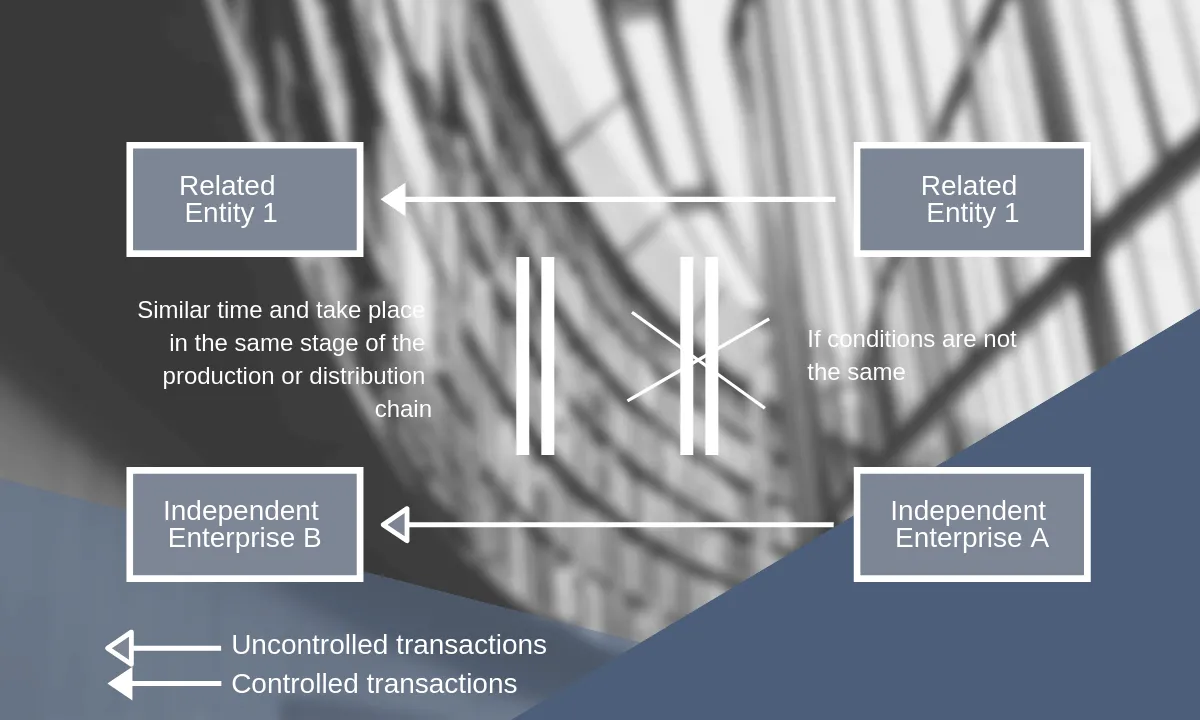

Transfer pricing methods this does not mean that its pricing should automatically be regarded as not being at arms length and there may be no reason to impose adjustments.

Transfer pricing best method rule. In accordance with the best method rule of. The selection of a transfer pricing method serves to find the most appropriate method for a. The FAQs examine the transfer pricing documentation and related penalty rules and offer insights about documentation best practices.

The Guidance is significant because it is the first time that the OECDs Transfer Pricing Guidelines have been updated to include guidance on the transfer pricing aspects of financial transactions. Differences can be made. The best method rule.

Of transfer pricing requires that the methodology used to determine the transfer price be the one that offers the greatest precising in matching the price of an arms-length transaction between unrelated parties. 3112021 A 1 Transfer pricing reports that comprehensively document the reasonable selection and application of a transfer pricing method consistent with the requirements of. More than minor differences.

In February 2020 the Organization for Economic Cooperation and Development OECD released Transfer Pricing Guidance on Financial Transactions Guidance. 1 the quality of the data and assumptions used in the analysis and 2 the degree of comparability between the controlled transaction or under the CPM the tested. Accordingly the CUP method may not be the best method.

The general rule specifies the transfer price as the sum of two cost components. 1482-1c a method may be applied in a particular case only if the comparability quality of data and reliability of assumptions under that method make it more reliable than any other available measure of the arms length result. Comparable profits method CPM.

Transfer pricing refers to the pricing of contributions assets tangible. Best Method Rule Law and Legal Definition. The official definition of the arms length standard as it applies in the United States can be found in Section 482-1 b of the transfer pricing regulations.

Transfer Pricing Comparable Uncontrolled Price Cup Method Royaltyrange

Transfer Pricing Methods Royaltyrange

What Will Your Country By Country Report Say About Your Transfer Pricing Policies Better To Know Now Transfer Pricing Country Report Business Practices

Methods Of Determining Alp Ppt Video Online Download

Transfer Pricing F5 Performance Management Acca Qualification Students Acca Global

Transfer Pricing

Franchises And Transfer Pricing Regulation Franchise Business Business Model Template Relationship Management

Transfer Pricing Regulations In Saudi Arabia Transfer Pricing Country Report Regulators

Gst Invoice Format Meteorio Pins Invoice Format Invoice Inside Sample Tax Invoice Template Australia 10 Invoice Template Word Invoice Template Invoice Format

International Transfer Pricing Ppt Download

How Transfer Pricing Works The Business World Is Becoming Increasingly Global And Multinational Companies Are The Norm Today In Fact Large Multinational Cor

Transfer Pricing