Transfer Definition As Per Capital Gain

Slump Sale And Its Taxability

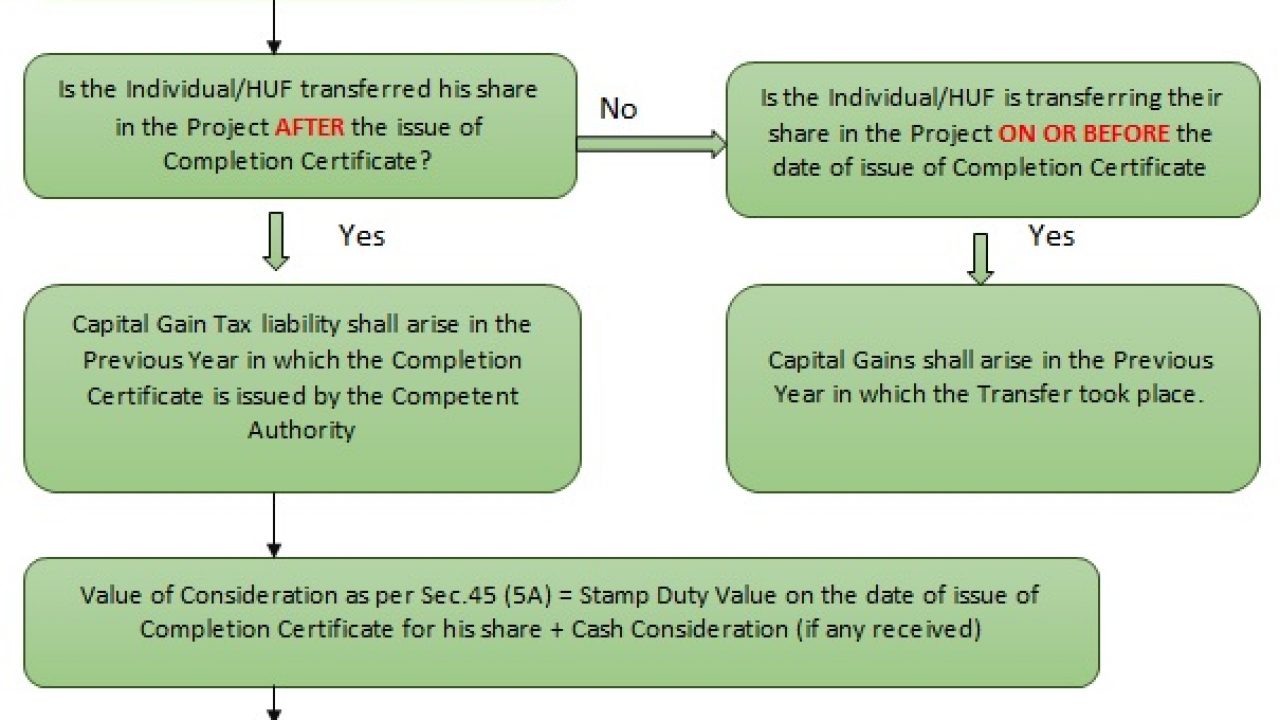

Concept Of Capital Gains In Case Of Joint Development Agreement

Capital Gains Ppt

Capital Gains Ppt

Determination Of Period Of Holding Of Capital Asset Short Term Or Long Term

Capital Gains Ppt

Hence urban agricultural lands constitute capital assets.

Transfer definition as per capital gain. The Transfer is of a Capital Asset us. The capital gains on transfer of capital. The most common capital gains are realized from the sale of stocks bonds precious metals real estate and property.

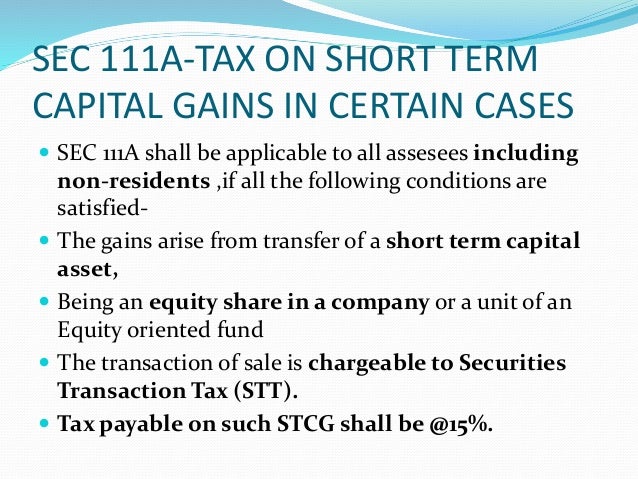

Capital gains treatment only applies to capital assets such as stocks bonds jewelry coin collections and. Short-term capital gains on transfer of listed equity sharesunits of an equity oriented fund and. It is not a Transaction in not regards as Transfer us.

Accordingly the AO determined the market value of the TDRFSI rights at Rs57423000- as per stamp authority valuation as against Rs50000000- declared by the receipt from sale of TDR and accordingly determined the capital gain in the hands of the. Capital gains tax is not applicable to the inherited property as there is an only transfer of ownership and no sale. An involuntary sale of a property of a debtor by a court at the instance of a decree holder is also transfer of a capital asset.

- Amount recorded in books on such transfer. Income from capital gains is classified as Short Term Capital Gains and Long Term Capital Gains. That transaction falls within the definition of Transfer us.

From above definition we can understand that the term Transfer under the Income Tax is mainly important to work out tax liability arising under the head. 772020 In the country considered realized capital gains are gains obtained related to fixed assets by onerous transfer under whatever title and those deriving from accident claims or those resulting from the permanent allocation of said elements to purposes not related to. Its the gain you make thats taxed not the amount of.

This resulted in a net capital gain of approximately INR 29 crore arising from the Transaction as against the net capital. 122016 Now would the date of registeration be the date of transfer for income tax purposes like computing Capital Gains or investing in RECL or NHAI bonds or would the initial date of consideration be considered as date of transfer as cited in CIT v CF. 182021 Transfer is defined as the sale of the asset giving up of rights on the asset forceful takeover by law or maturity of the asset.

Capital Gains Ppt

Taxation Of Capital Gains New Taxbuddy

Concept Of Capital Gains In Case Of Joint Development Agreement

What Are Capital Gains What Is Stcg Tax 5paisa 5pschool

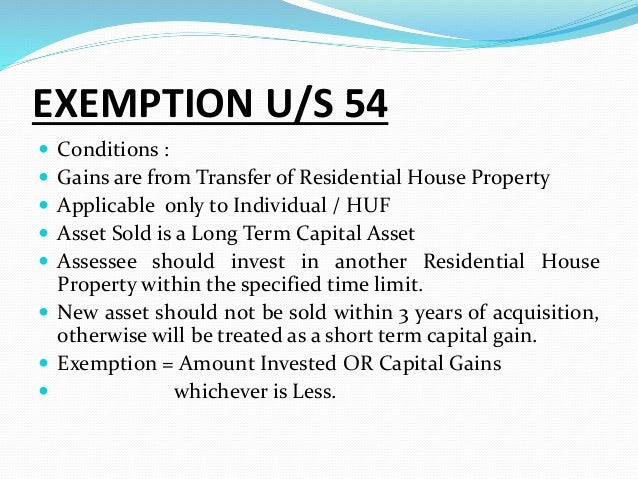

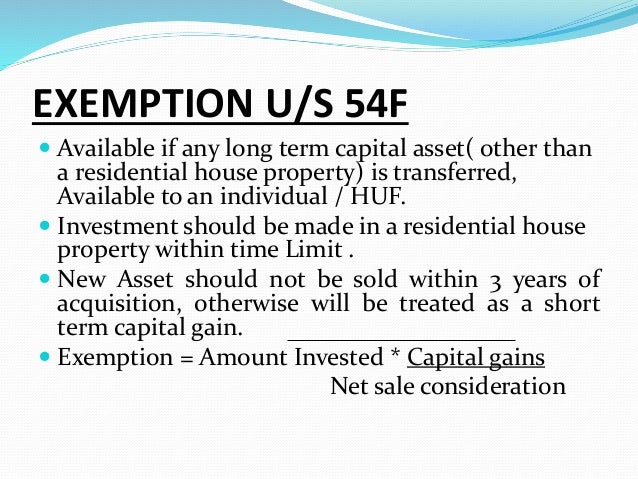

Deduction Under Capital Gains

Capital Gain All You Want To Know

How To Calculate Capital Gains On Sale Of Gifted Property Examples

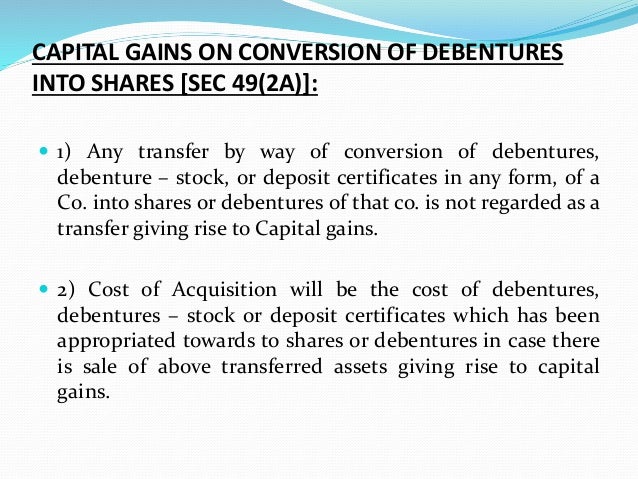

Capital Gain On Conversion Of Capital Asset Into Stock In Trade

Capital Gains Ppt

How To Calculate Capital Gains On Sale Of Gifted Property Examples

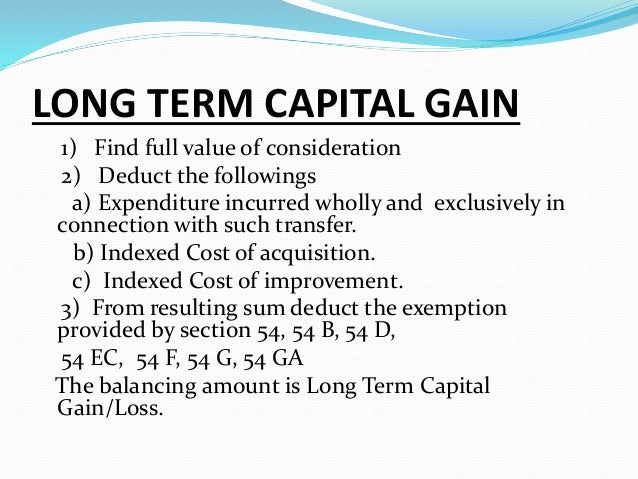

Capital Gains How Computed U S 48

What Is Long Term Capital Gains Tax The Financial Express

Capital Gains Ppt